For many people, the word mutual fund sounds complicated or risky. Some associate it with the stock market, others with scams they hear about on social media. As a result, many prefer to keep their money only in savings accounts, fixed deposits, gold, or real estate.

But a mutual fund is not a shortcut to quick profits, nor is it something mysterious. At its core, it is a simple and regulated way to invest money professionally, especially for people who do not have the time, expertise, or interest to manage investments on their own.

This article explains what a mutual fund is, how it works, and why it is widely used by long-term investors—in simple language.

What Is a Mutual Fund?

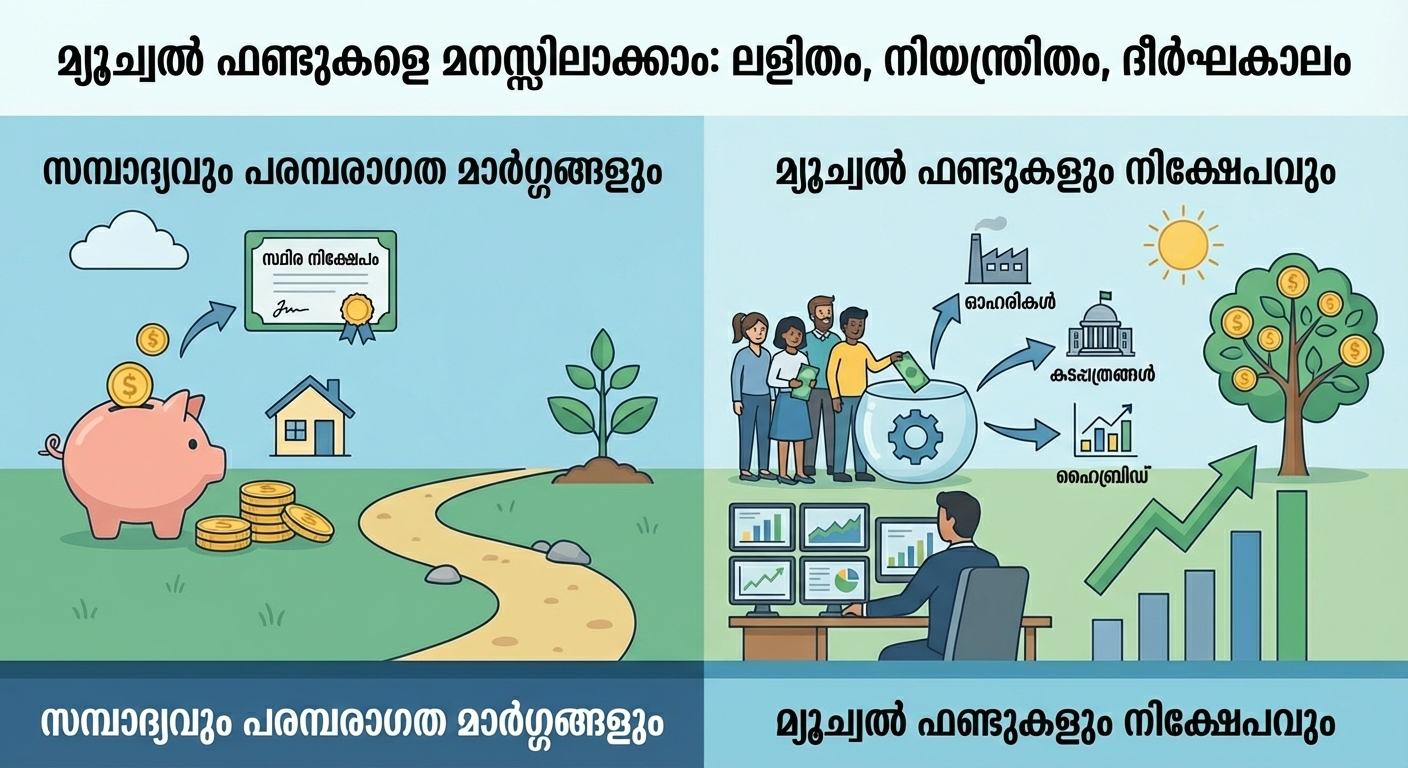

A mutual fund is an investment vehicle where money from many investors is pooled together and invested in different assets such as shares (equity), bonds (debt), or a mix of both.

Instead of investing directly in individual stocks or bonds, you invest in a mutual fund scheme, which is managed by professional fund managers.

Each investor owns units of the mutual fund, and the value of these units changes based on the performance of the underlying investments.

A mutual fund allows you to invest your money along with others, while professionals manage the investment decisions.

How Does a Mutual Fund Work?

To understand how a mutual fund works, let’s break it down step by step.

1. Investors Put Money into a Mutual Fund

Many investors contribute money to a mutual fund scheme. This can be done:

Each contribution buys you units of the fund.

2. Money Is Managed by Professionals

The pooled money is managed by a fund manager, who is supported by a research team. Their job is to:

- Study markets and companies

- Decide where to invest

- Monitor risks

- Align investments with the fund’s objective

Investors do not need to track daily market movements or make frequent decisions.

3. Investments Are Diversified

One of the key benefits of mutual funds is diversification.

Instead of investing in one company or one bond, a mutual fund typically invests in:

- Multiple companies

- Different sectors

- Various types of instruments

This reduces the impact of poor performance from any single investment.

4. Returns Reflect Market Performance Over Time

The value of a mutual fund unit is called Net Asset Value (NAV). NAV changes daily based on the market value of the investments held by the fund.

Over time:

- If investments perform well, NAV increases

- If markets decline, NAV may fall

Mutual funds are designed for long-term investing, not short-term speculation.

Who Regulates Mutual Funds in India?

Mutual funds in India are strictly regulated.

- They are regulated by SEBI (Securities and Exchange Board of India)

- Each mutual fund is managed by an Asset Management Company (AMC)

- Investor money is held safely with custodians and trustees

- Distributors are registered with AMFI

This structure ensures transparency, accountability, and investor protection.

Types of Mutual Funds (Simple Overview)

There are many types of mutual funds, but beginners can broadly understand them as:

Equity Mutual Funds

- Invest mainly in shares of companies

- Suitable for long-term goals

- Returns fluctuate in the short term but may grow over time

Debt Mutual Funds

- Invest in bonds and fixed-income instruments

- Generally more stable than equity funds

- Used for income and capital preservation

Hybrid Mutual Funds

- Invest in both equity and debt

- Aim to balance growth and stability

Each fund has a clear objective, and investors choose based on their goals and time horizon.

Is Mutual Fund Investment Safe?

common questions about mutual funds

Mutual funds are not risk-free, but they are regulated and transparent.

Important points to understand:

- Market-linked investments can go up and down

- Risk depends on the type of fund and time horizon

- Long-term investing helps reduce short-term volatility

- Diversification reduces concentration risk

Safety in mutual funds comes from:

- Regulation

- Transparency

- Professional management

- Long-term discipline

Mutual Fund vs Traditional Savings

Many people save money diligently but still worry about the future. This happens because saving and investing serve different purposes.

- Savings focus on safety and liquidity

- Investing focuses on long-term wealth creation

Mutual funds are not meant to replace savings but to complement them, especially for long-term goals like retirement, children’s education, or financial independence.

Who Should Consider Mutual Funds?

Mutual funds are suitable for:

- First-time investors

- Salaried individuals

- Self-employed professionals

- NRIs investing in India

- Anyone who prefers structured, disciplined investing

You do not need a large amount to start. What matters more is consistency and time.

The Importance of Understanding Before Investing

One of the biggest mistakes investors make is investing without understanding.

Before investing in mutual funds, it is important to:

- Know your goals

- Understand your time horizon

- Be comfortable with market fluctuations

- Avoid chasing short-term trends

Education and clarity are more important than quick decisions.

Final Thoughts

A mutual fund is not a shortcut to instant wealth, nor is it something to fear. It is a structured, regulated, and widely used investment tool designed to help investors participate in the financial markets responsibly.

Understanding how mutual funds work is the first step toward building confidence as an investor. With the right approach, patience, and discipline, mutual funds can play an important role in long-term financial planning.

At BVB Capital Private Limited, our focus is on simplifying mutual fund investments through education, clarity, and responsible guidance—helping investors understand before they invest.