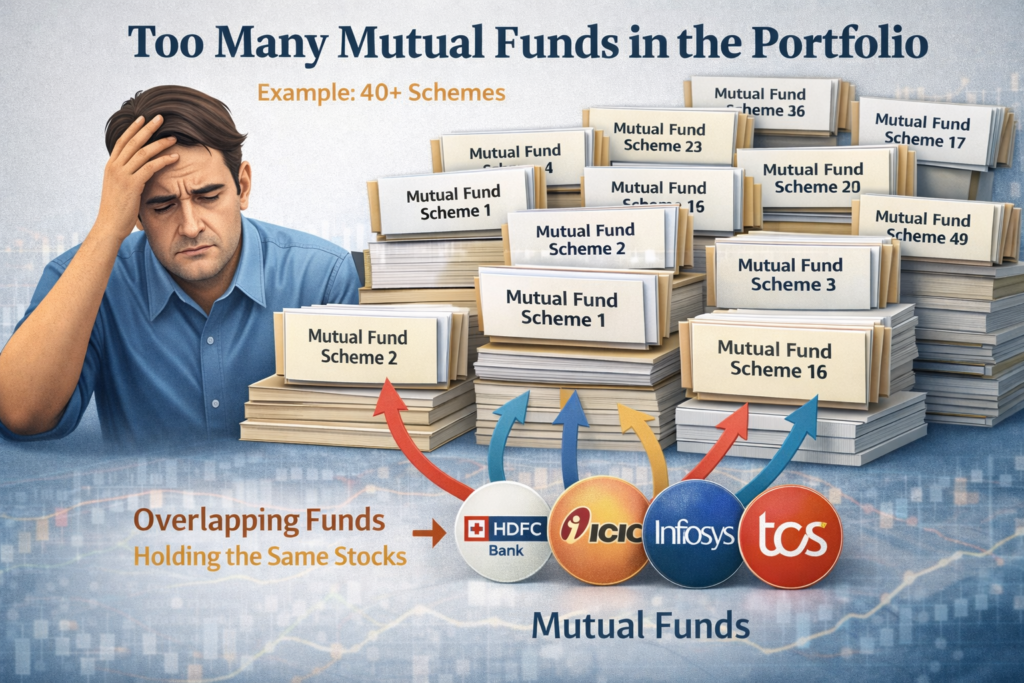

When people start investing in mutual funds, they often feel excited. One friend suggests a fund, YouTube recommends another, social media talks about “top-performing funds,” and before long, the investor ends up holding 8, 10, or even 15 mutual funds.

At first, this feels like a smart strategy.

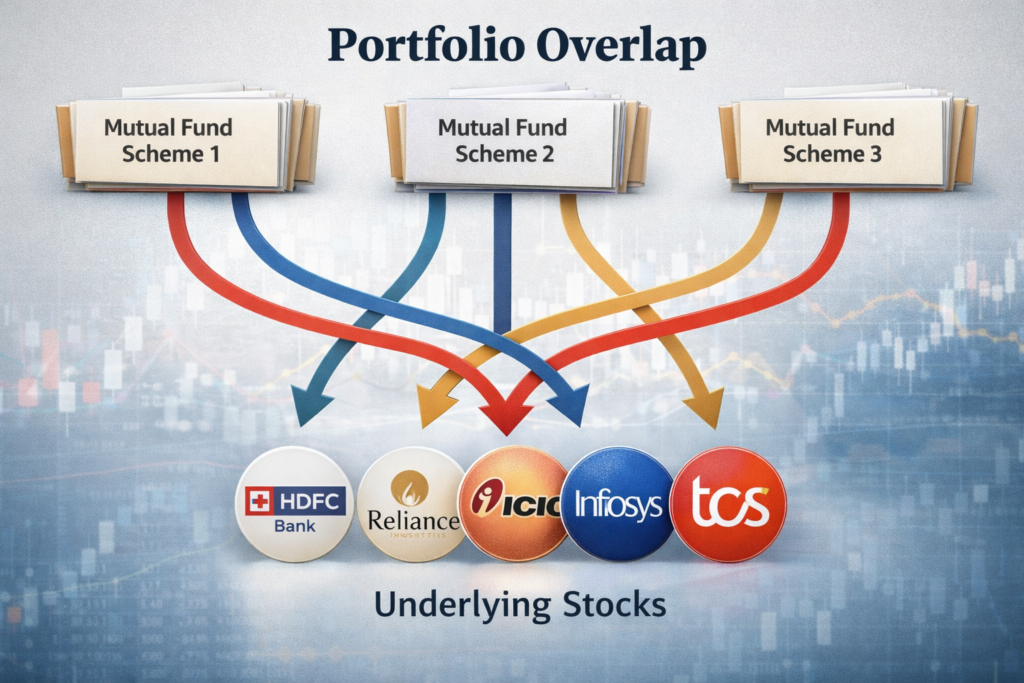

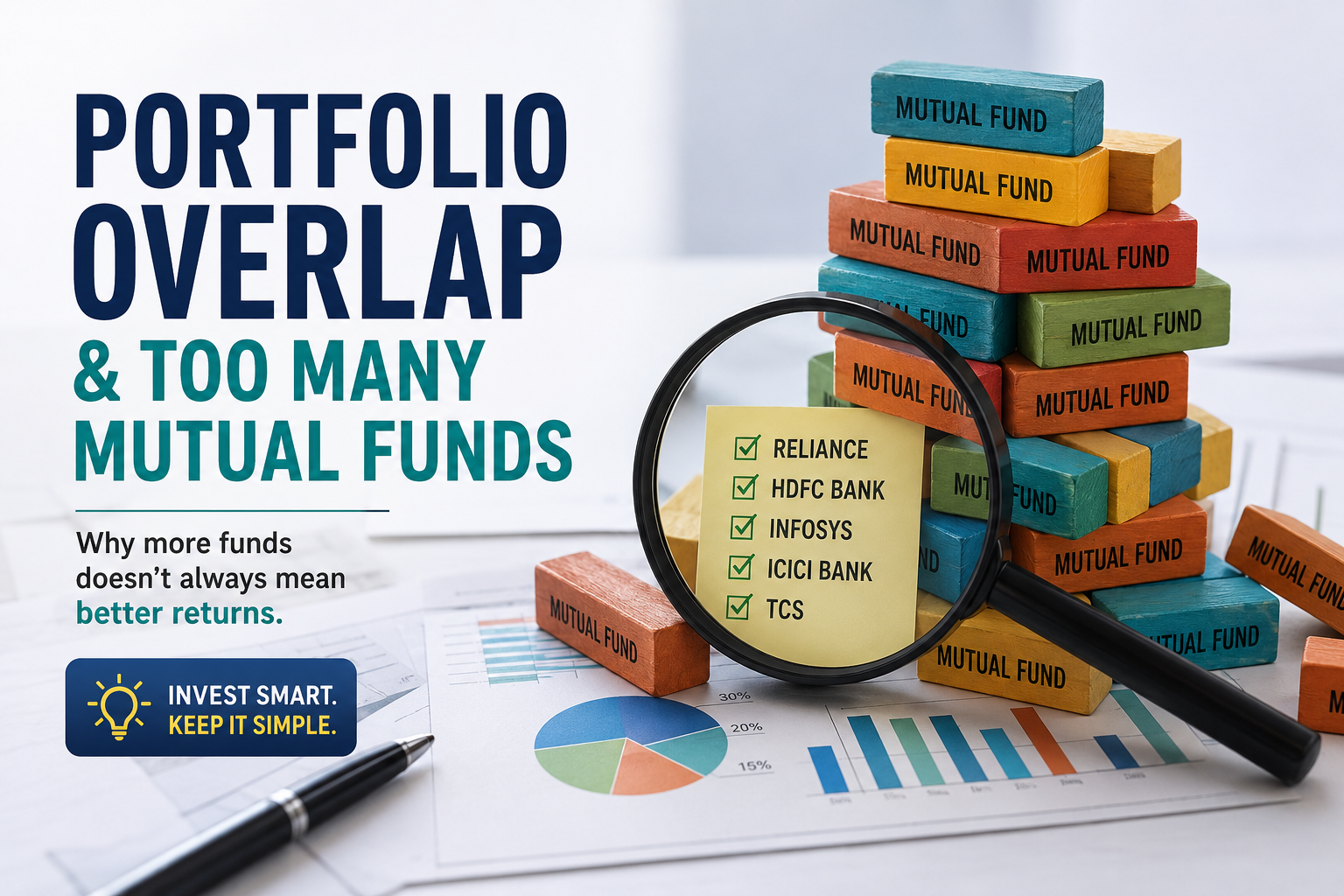

But in reality, many investors unknowingly create a big problem called portfolio overlap.

This is one of the most common mistakes seen among beginner and even experienced investors in India.

Let us understand this in the simplest possible way.

What is Portfolio Overlap?

Imagine you own:

- 3 cricket teams

- But all three teams have almost the same players

Do you really have different teams?

Not really.

The same thing happens in mutual funds.

Many mutual funds buy shares of the same companies like:

- Reliance

- HDFC Bank

- Infosys

- ICICI Bank

- TCS

So even if you own many mutual funds, you may actually be investing in the same stocks repeatedly.

This is called portfolio overlap.

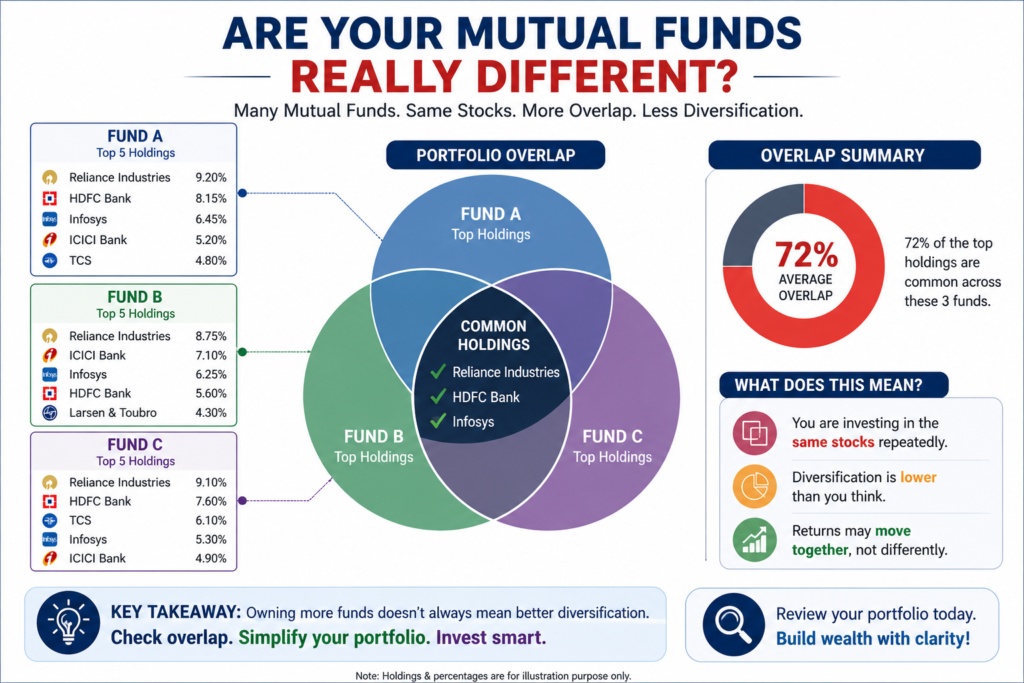

A Simple Real-Life Example

Suppose Ravi invests in:

- Large Cap Fund A

- Flexi Cap Fund B

- Index Fund C

He feels diversified because he owns 3 funds.

But when he checks the holdings, he discovers:

- All three funds heavily own Reliance

- All three own HDFC Bank

- All three own Infosys

Now Ravi’s money is repeatedly going into the same companies.

This is like buying three different school bags but filling all of them with the same books.

Why Too Many Mutual Funds Can Become a Problem

Many people think:

“More mutual funds means more safety.”

But that is not always true.

Sometimes, too many funds create confusion instead of growth.

1. Difficult to Track

When you own many funds:

- Monitoring performance becomes difficult

- You forget why you invested

- SIP dates become confusing

- Rebalancing becomes harder

Investing should make life simpler, not stressful.

2. Duplicate Investments

Many funds may hold similar stocks.

This means:

- You are not truly diversified

- Risk reduction becomes weaker

- Returns may look almost identical

You may think you own 10 investments, but actually you own the same 20–30 stocks repeatedly.

3. Lower Overall Performance

Some investors keep adding new funds every year.

The result?

- Winners and losers cancel each other

- Portfolio becomes average

- Strong-performing funds lose impact

It becomes like having too many cooks in one kitchen.

4. Emotional Investing Increases

Too many funds often happen because of:

- Fear of missing out (FOMO)

- Social media hype

- Random recommendations

- Chasing recent returns

This creates emotional investing instead of disciplined investing.

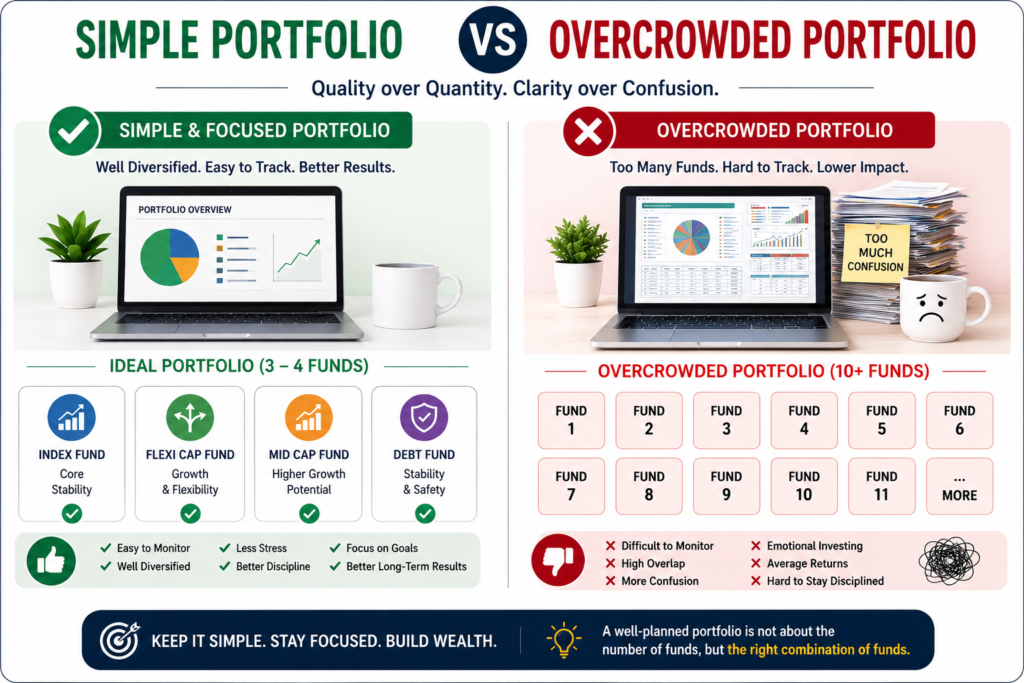

How Many Mutual Funds Are Actually Enough?

For most retail investors, a simple portfolio is usually better.

A basic structure may look like:

- Equity Funds

- Debt Fund (depending on goals)

That itself is enough for many investors.

You do not need 12 different mutual funds to build wealth.

Remember:

A healthy garden does not need 100 plants.

It needs the right plants, properly maintained.

What Happens When Funds Overlap Too Much?

Let us understand with an analogy.

Imagine you own:

- 5 umbrellas

- But all have holes in the same place

Will owning more umbrellas help during rain?

No.

Similarly, owning many mutual funds with the same holdings may not protect your portfolio during market falls.

True diversification means:

- Different categories

- Different strategies

- Different types of companies

Not simply more funds.

Signs That You Have Too Many Mutual Funds

You may have an overcrowded portfolio if:

- You cannot remember all your fund names

- Multiple funds give almost identical returns

- You invested because someone suggested it

- You keep adding funds but never reviewing them

- You own many funds from the same category

If this sounds familiar, it may be time for a portfolio review.

How to Check Portfolio Overlap

You can check overlap by:

- Looking at top holdings of each fund

- Comparing fund categories

- Using online overlap tools

- Consulting a qualified mutual fund distributor or advisor

Even a quick review can reveal surprising duplication.

Is Overlap Always Bad?

No.

Some overlap is normal.

For example:

- Most large-cap funds will own major Indian companies

- Index funds naturally hold popular stocks

The problem begins when overlap becomes excessive.

Too much repetition reduces the benefit of diversification.

The Power of Simplicity in Investing

Some of the best investors in the world follow simple portfolios.

Why?

Because simplicity helps:

- Better decision-making

- Easier monitoring

- Less stress

- Better discipline

- Long-term consistency

A simple portfolio is easier to stay invested in during market ups and downs.

And staying invested for a long time is one of the biggest secrets of wealth creation.

Quality Matters More Than Quantity

Many investors proudly say:

“I have 15 mutual funds.”

But the important question is:

“Do those funds actually serve different purposes?”

A smaller, well-planned portfolio is often much stronger than a large messy portfolio.

In investing, more is not always better.

Better is better.

Final Thoughts

Mutual funds are powerful tools for wealth creation.

But owning too many funds without understanding overlap can silently reduce the effectiveness of your investments.

Instead of collecting funds like cricket cards, focus on building a clear and meaningful portfolio.

Think of your investments like a good football team:

- Every player should have a role

- Too many players in the same position creates imbalance

The goal is not to own the maximum number of mutual funds.

The goal is to build wealth peacefully, steadily, and intelligently.

Need Help Checking Your Mutual Fund Portfolio?

Many investors do not realise that their portfolio has become overcrowded with too many mutual funds holding similar stocks.

If you are unsure whether your investments are properly diversified or unnecessarily complicated, you can contact BVB Capital Private Limited for a professional portfolio review.

Our experts can help you:

- Identify portfolio overlap

- Simplify your mutual fund investments

- Remove unnecessary duplication

- Build a cleaner and goal-based portfolio

- Make investing easier to track and understand

Sometimes, simplifying your portfolio can improve clarity, confidence, and long-term discipline.

Contact Details

BVB CAPITAL PRIVATE LIMITED

AMFI Registered Mutual Fund Distributor

ARN: 348338

Thrissur, Kerala – 680568

📞 Phone: 080 696 40046

📱 WhatsApp: 96339 40008

Invest smart. Keep your portfolio simple, meaningful, and easy to manage.

Frequently Asked Questions (FAQs)

1. What is portfolio overlap in mutual funds?

Portfolio overlap happens when multiple mutual funds own many of the same stocks.

2. Is it bad to have too many mutual funds?

Yes, too many mutual funds can create duplication, confusion, and weaker diversification.

3. How many mutual funds should a beginner have?

For many beginners, 2 to 4 carefully selected mutual funds are often enough.

4. Can two mutual funds from different categories overlap?

Yes. Even different categories may hold some of the same companies.

5. How can I reduce portfolio overlap?

Review your holdings regularly and avoid adding funds without a clear purpose.

Mutual Fund investments are subject to market risks. Read all scheme related documents carefully before investing.