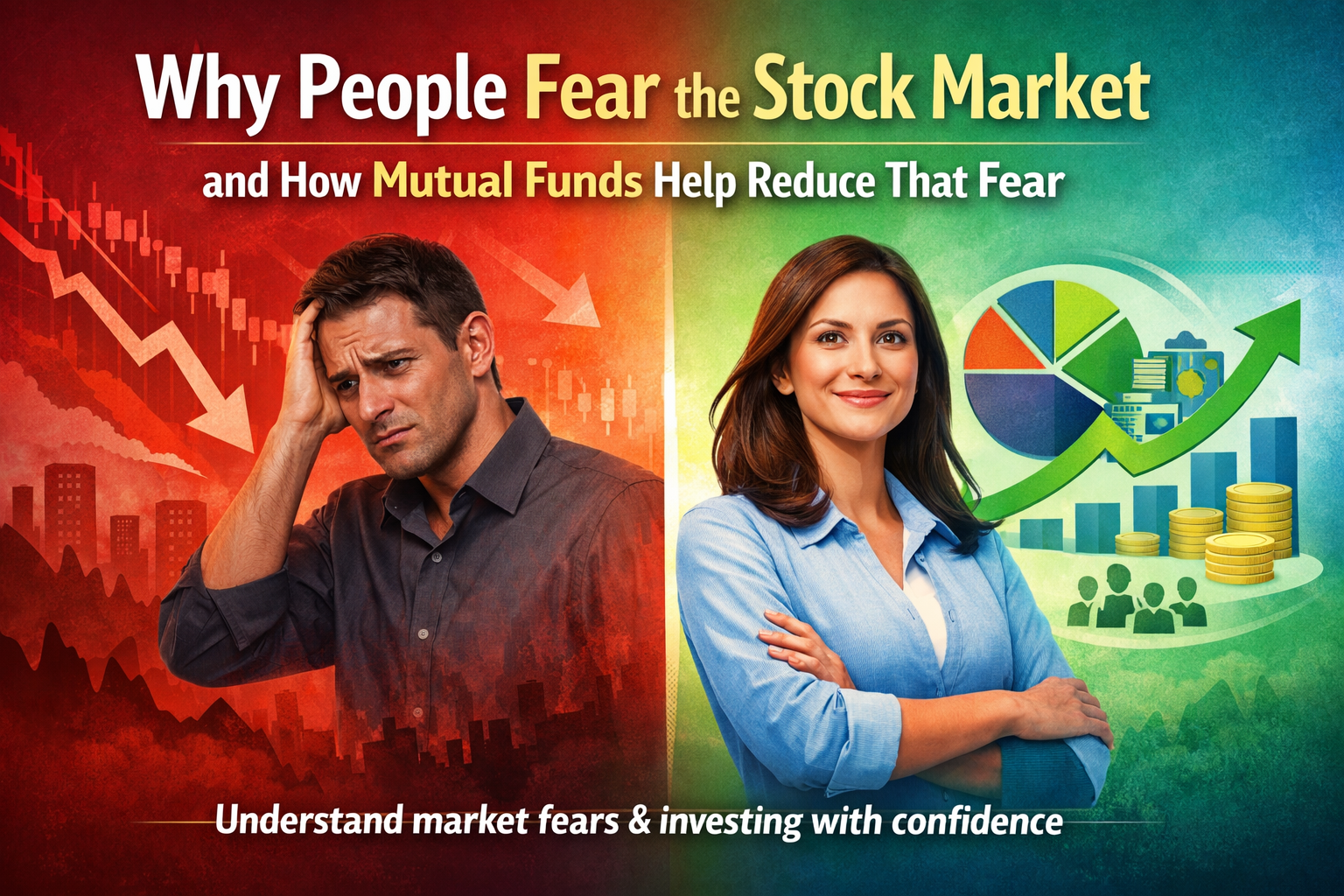

News about market crashes, scams, and losses often creates fear around investing. For many people, the stock market feels unpredictable and risky, leading them to avoid investing altogether.

This article explains why such fears exist and how mutual funds provide a structured way to participate in markets with better risk management.

Why the Fear Exists

Fear around the stock market usually comes from:

- Lack of financial knowledge

- Stories of short-term losses

- Scams and misinformation

- Confusion between trading and investing

These factors can discourage people from exploring long-term investment opportunities.

How Mutual Funds Are Different from Direct Stock Trading

Mutual funds:

- Are professionally managed

- Invest across multiple companies and sectors

- Follow regulatory guidelines set by SEBI

- Reduce risk through diversification

This makes them fundamentally different from speculative trading.

Long-Term Investing vs Short-Term Reactions

Markets move up and down in the short term, but long-term investing focuses on growth over years, not days. Mutual funds are designed with this long-term approach in mind.

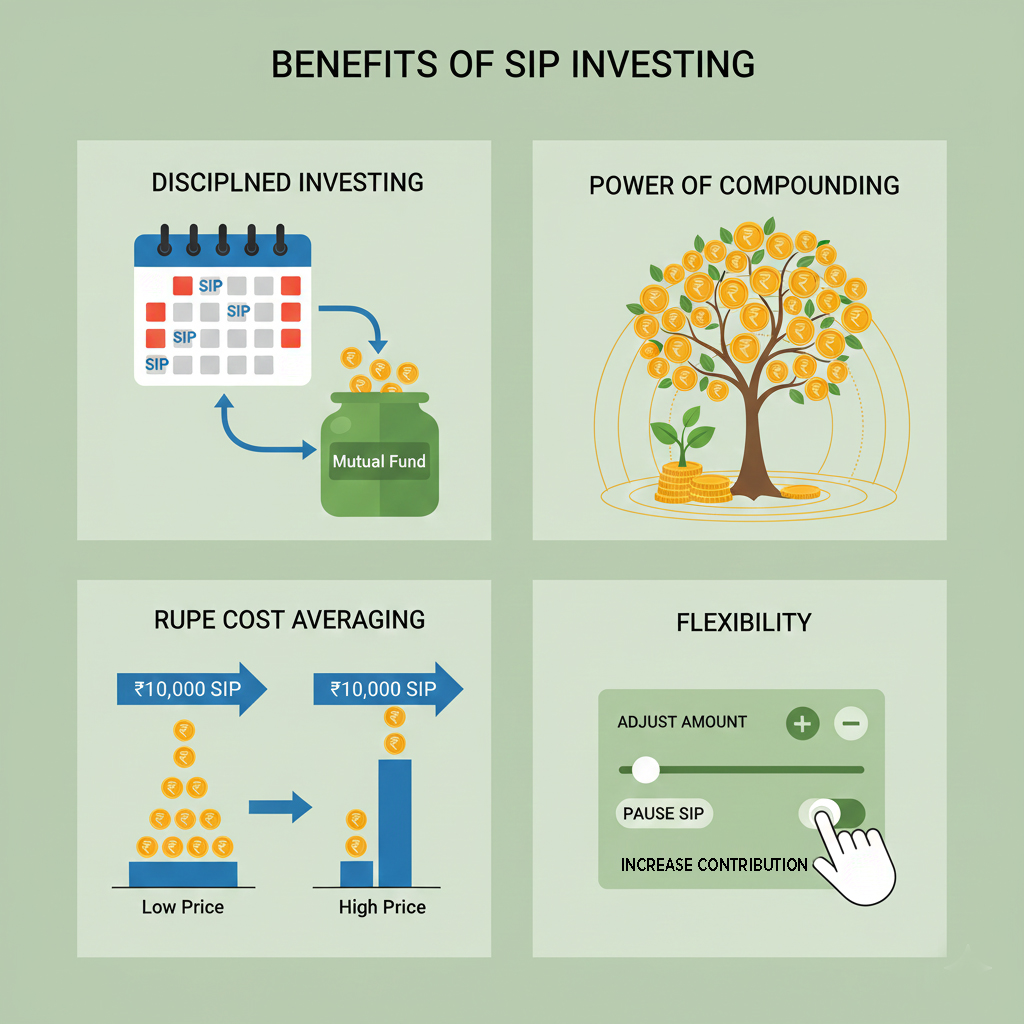

SIPs further reduce anxiety by spreading investments over time rather than relying on one-time decisions.

Building Confidence Through Understanding

When investors understand how mutual funds work, fear reduces significantly. Education, clarity, and realistic expectations help investors stay calm during market fluctuations.

Conclusion

Fear of the stock market is common—but it doesn’t have to stop long-term investing. Mutual funds offer a structured, regulated, and diversified way to participate in markets with confidence and discipline.