Which Is Better for You? (Complete Guide for Indian Investors)

The Real-World Dilemma of Indian Investors

Meet Ramesh, a 32-year-old working in Kochi. Like many Indians today, he wants to grow his savings beyond a bank FD and has heard a lot about SIPs and mutual funds. He downloads a few “zero commission” investment apps, compares star ratings of funds, starts a SIP, and feels proud.

But soon… he is confused.

- Should he invest more in equity?

- Why did his fund fall last month?

- Which ELSS fund should he use for tax saving?

- Should he stop SIPs when markets dip?

- How should he plan for his child’s education?

Meanwhile his colleague Amrita invests through a mutual fund distributor. She doesn’t worry about research, rebalancing, or risk. Her advisor reviews her portfolio quarterly, suggests SIP top-ups, evaluates goals, explains market dips, and helps with tax planning.

Both invest in the same mutual fund category. But while Ramesh keeps switching funds and stopping SIPs during volatile months, Amrita follows a disciplined strategy created for her goals — and ends up earning higher long-term returns with less stress.

So the big question arises for investors today:

“Is it worth paying for a distributor’s help, or should you go direct?”

This debate of direct vs distributor mutual funds has grown in the last few years due to fintech apps and DIY investing culture.

Reality check:

While direct mutual funds may look cheaper due to slightly lower expense ratios, the real cost comes from wrong choices, poor asset allocation, and emotional mistakes — especially during crashes.

On the other hand, a skilled mutual fund distributor or mutual fund investment advisor brings structured financial planning, goal-based investing, risk management, and behavioral guidance — which most investors desperately need.

Throughout India — especially in small cities and towns — people rely on distributors because they want handholding, not just a transaction platform.

And this is where BVB Capital Private Limited stands out.

Based in Kerala, BVB Capital is a AMFI-registered, client-first, technology-enabled mutual fund distributor helping families build wealth without confusion, panic, or guesswork.

🟢 Thesis:

For most investors (80–90% of Indians), the benefits of a good distributor easily outweigh the small cost difference of direct plans — and BVB Capital excels because of its experienced management team, advisory-led model, and long-term client focus.

Understanding Mutual Fund Investment Options

Before deciding which route to take, it’s important to understand how mutual funds can be purchased in India.

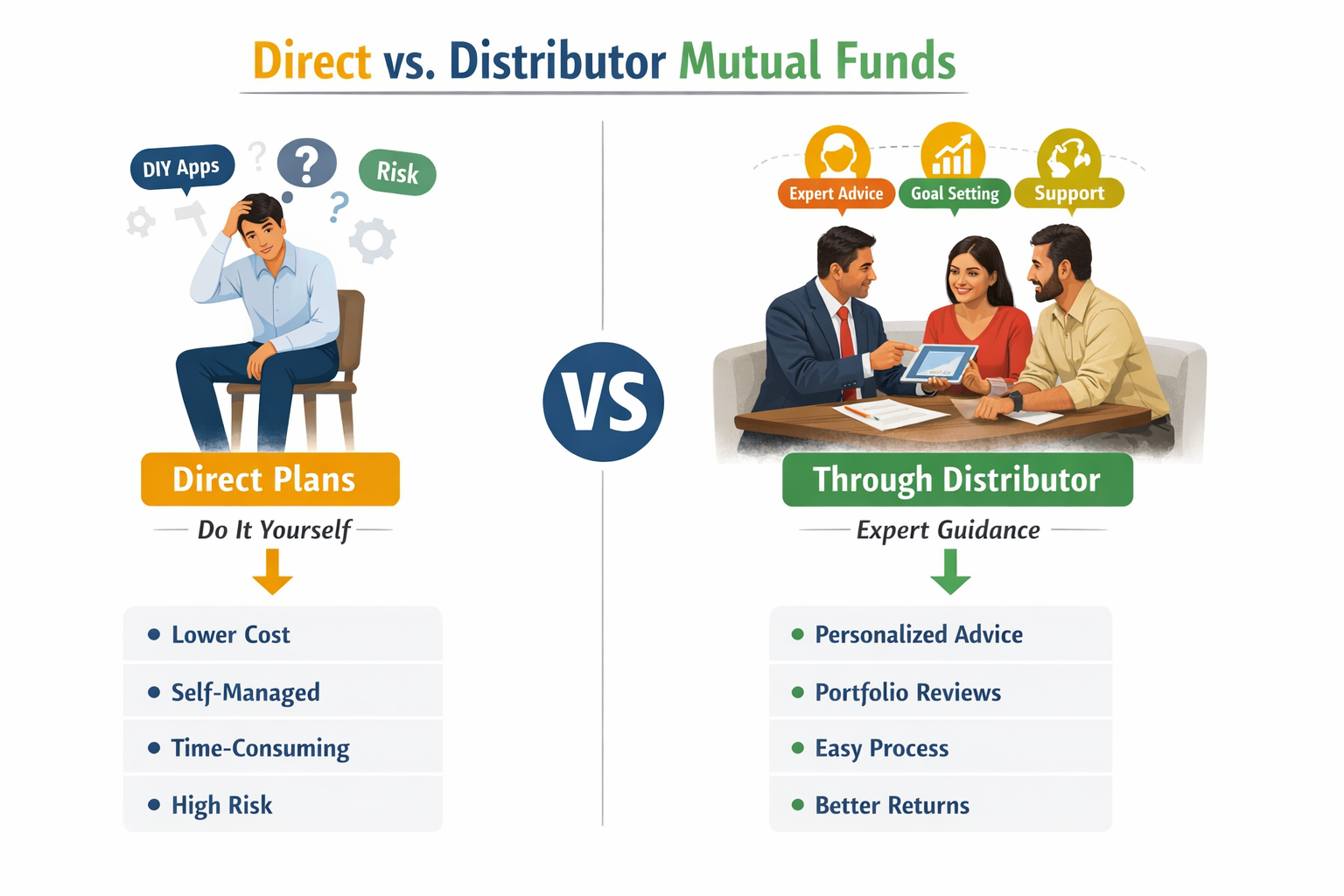

What are Direct Plans?

Direct plans allow you to invest directly with the AMC (fund house) through:

- AMC websites

- AMC apps

- RTA portals (CAMS, Kfintech)

- Some online DIY platforms

Key features of direct plans:

- Lower expense ratio (no distributor commission)

- Full control — investor chooses funds, tracks performance, manages risk

- Suitable mainly for DIY financial experts

But there’s a catch: Investors must handle asset allocation, taxation, fund selection, rebalancing, market behavior, and documentation on their own.

What are Regular Plans via Distributors?

Regular plans are purchased through a mutual fund distributor or advisor who assists with:

- Goal setting

- Fund selection

- Documentation & KYC

- Ongoing review

- Rebalancing

- Market guidance

Regular plans have a slightly higher expense ratio because distributors are paid by AMCs for providing services.

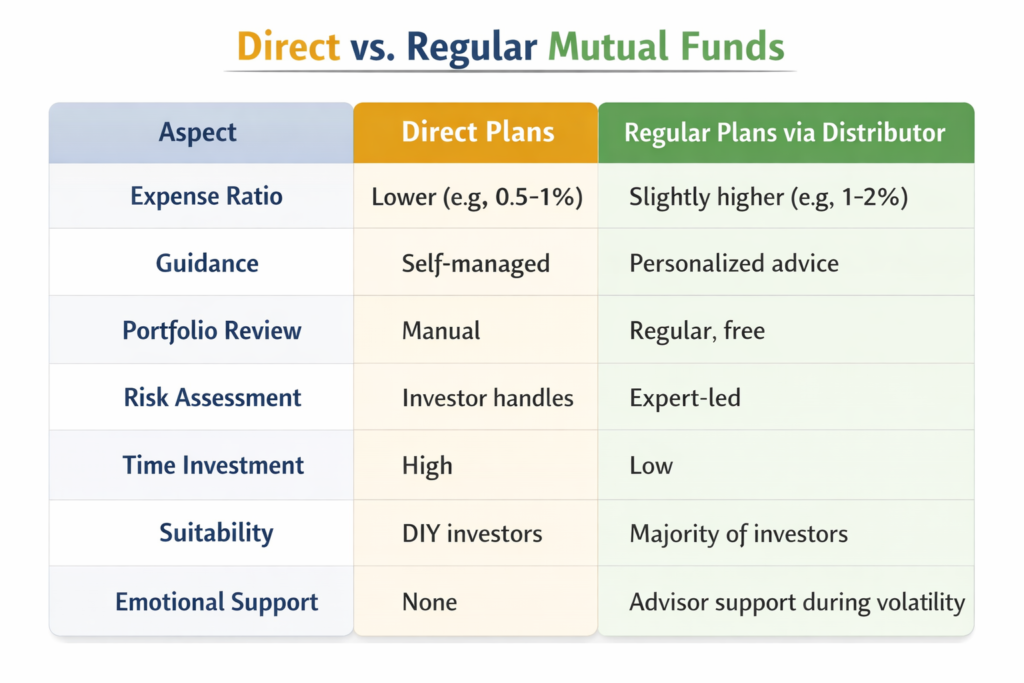

Direct vs Regular: Quick Comparison

| Aspect | Direct Plans | Regular Plans via Distributor |

|---|---|---|

| Expense Ratio | Lower (e.g., 0.5–1%) | Slightly higher (e.g., 1–2%) |

| Guidance | Self-managed | Personalized advice |

| Portfolio Review | Manual | Regular, structured, free |

| Risk Assessment | Investor handles | Expert-led |

| Time Investment | High | Low |

| Suitability | DIY investors | Majority of investors |

| Emotional Support | None | Advisor support during volatility |

🔹 Reality Check:

Direct plans suit financially educated, disciplined, long-term DIY investors.

For 90% of Indian investors, a trusted distributor is more beneficial because investing is not just selecting funds — it’s about managing entire financial life cycles.

Top Benefits of Using a Mutual Fund Distributor

Here are the major mutual fund distributor benefits that most investors underestimate:

1. Personalized Investment Advice

Distributors analyze:

- Age

- Income & cash flow

- Risk profile

- Time horizon

- Life goals (retirement, education, home, tax)

They design goal-based portfolios tailored to investors.

Example:

- 25-year-old professional → equity-heavy SIPs for long-term growth

- 60-year-old retiree → debt & hybrid for stability & income

2. Access to 1000+ Funds Across AMCs

Instead of relying on popular brand names, distributors help you choose across:

- Equity

- Debt

- Hybrid

- Solution-oriented funds

- Index funds

- ELSS for tax planning

This ensures proper diversification, not random selection.

3. Ongoing Portfolio Review & Rebalancing

Markets change, life changes — portfolios must too.

Distributors provide:

- Quarterly reviews

- Asset rebalancing

- SIP top-up recommendations

- Category rotation (largecap ↔ midcap, etc.)

This helps maintain the right risk-return balance.

4. Time-Saving Transactions & Support

Investors don’t want paperwork headaches such as:

- KYC registration

- FATCA

- Consolidated statements

- SIPS/STPs/SWPs

- Nomination updates

Distributors handle all of this smoothly.

5. Behavioral & Emotional Discipline

One of the most underrated advantages:

Investment success is more about behaviour than returns.

During market volatility, DIY investors panic.

Example:

During the 2020 COVID crash, many DIY investors sold at bottoms, while distributors advised clients to continue SIPs, leading to significant wealth creation post recovery.

6. Risk Management

Distributors help avoid:

- Over-concentration in a single stock/sector

- Wrong timing decisions

- Misalignment of asset allocation

They also guide on debt vs equity balance, crucial for retirees.

7. Tax Optimization

They assist with:

- ELSS fund selection

- Capital gains tax calculations

- Dividend taxation

- Setting SWP for tax efficiency

8. Cost-Effectiveness in Long Term

While direct plans save 0.5–1% TER, mistakes can cost 2–5% returns annually due to:

- Wrong fund choices

- Lack of rebalancing

- Stopping SIPs

- Timing markets

- Over-diversification or under-diversification

Industry reports suggest that guided investors earn 1–2% higher net returns due to discipline and asset allocation.

Direct vs Distributor: Head-to-Head Comparison

To make things crystal clear, here is a direct comparison:

Pros & Cons Table

| Factor | Direct Plans Pros/Cons | Distributor Pros/Cons |

|---|---|---|

| Cost | ✔ Lower TER ✖ Hidden errors cost more | ✔ Saves via expertise ✖ Commission in expense ratio |

| Expertise | ✖ Investor must self-educate | ✔ Custom strategies & guidance |

| Convenience | ✔ 24/7 apps ✖ Zero handholding | ✔ Full service ✖ Appointment-based |

| Suitability | Experts only | Beginners, families, HNIs |

| Behavioral Control | ✖ High panic risk | ✔ Emotional discipline |

| Portfolio Returns | Variable due to errors | Optimized (1–3% possible edge) |

Verdict

Data from multiple consumer surveys show that:

- 80%+ of Indian investors prefer distributors

- Only 10–15% have the knowledge for direct investing

- Errors hurt long-term compounding more than commissions

So, while direct plans look attractive on paper, distributors win in real life — especially for:

- Beginners

- Busy professionals

- Retirees

- Business owners

- Families planning life goals

Why BVB Capital Private Limited Is the Best Choice for Investors

1. Who We Are

BVB Capital Private Limited is a Kerala-based, AMFI-registered mutual fund distributor dedicated to simplifying investments for Indians.

Our mission:

To make wealth-building simple, transparent, and stress-free for every investor.

We are built for people who want:

- Guidance, not confusion

- Discipline, not panic

- Knowledge, not tips

- Long-term wealth, not short-term gambling

2. What Makes Us Different

While many providers just offer “platforms,” BVB Capital offers a complete advisory ecosystem:

✔ Goal-based financial planning

✔ Risk profiling & suitability analysis

✔ Technology-driven onboarding

✔ Customized SIP strategies

✔ Tax planning support

✔ Quarterly portfolio reviews

✔ Transparency with zero-pressure approach

We do not push products. We create tailored portfolios.

3. Powered by Technology

We use digital tools for:

- KYC & onboarding

- Portfolio dashboards

- SIP calculators

- Tax statements

- Goal tracking

Tech gives speed — Advisors give wisdom. Investors need both.

4. Management Team: The Core Strength

The primary reason BVB Capital stands out among the best mutual fund distributors in India is its strong management team.

Unlike generic platforms, our leadership brings decades of hands-on experience in:

- Mutual funds

- Equity markets

- Debt strategies

- Financial planning

- Banking & compliance

➡️ Meet our Management Team:

https://bvbcap.com/management-team/

This team-based model ensures investors get research-backed advice, not generic recommendations.

5. Our Advisory Philosophy

At BVB Capital, we believe:

- Investing is personal

- Risk matters as much as return

- Markets reward patience

- SIPs are powerful wealth builders

- Advice must be unbiased & transparent

We educate clients because informed investors stay disciplined.

6. Comparison With Others

| Category | Generic Distributor | BVB Capital |

|---|---|---|

| Advisory Quality | Transaction-focused | Advisory-driven |

| Client Interaction | One-time | Continuous relationship |

| Goal Planning | Minimal | Structured & documented |

| Review Frequency | Annual/None | Quarterly reviews |

| Tools & Reporting | Basic | Digital dashboards |

Conclusion

Direct mutual funds are good for trained, disciplined DIY investors.

But for most Indians, the value of a skilled mutual fund distributor or mutual fund investment advisor is far greater than the small cost difference.

From personalized planning to behavioral guidance and disciplined compounding — distributors make wealth building simpler, smarter, and stress-free.

And when it comes to choosing one, BVB Capital Private Limited stands out for its expert management team, advisory-first approach, and technology-driven client service, making it among the best mutual fund distributor India for families and professionals.

👉 Ready to invest smart and grow your wealth?

Book a free consultation with us at:

https://bvbcap.com/

Start your SIP today and build wealth the right way — with guidance, discipline, and confidence.