Most people start a SIP without knowing if ₹2,000 per month will actually get them where they want to go. They pick an amount that feels comfortable, choose a fund someone recommended, and hope for the best. Years later, they discover the number was never going to be enough.

This guide — and the SIP calculator below — will tell you the exact monthly SIP amount for any goal, whether it is ₹25 lakh for your child’s college education, ₹1 crore for retirement, or a dream home down payment. You will also learn why the number changes dramatically based on when you start.

At BVB Capital, we are an AMFI-registered mutual fund distributor (ARN 348338) based in Kerala. We help families across Kerala calculate and start SIPs every day. Everything in this article reflects real numbers and practical guidance we give our clients.

SIP Goal Calculator

What Is a SIP and How Does the SIP Calculator Work?

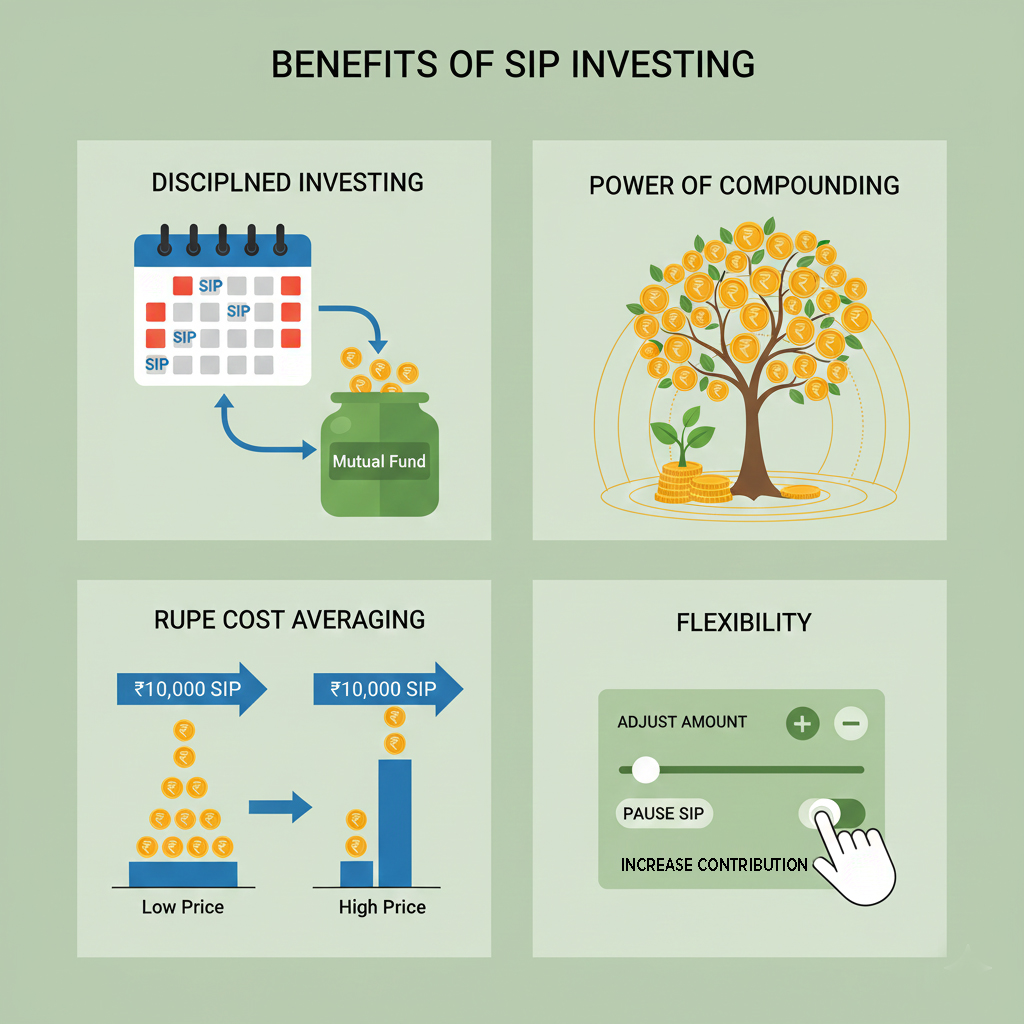

A Systematic Investment Plan (SIP) is a method of investing a fixed amount in a mutual fund at regular intervals — usually monthly. Instead of investing a large sum all at once, you invest smaller amounts over time. This approach is called rupee cost averaging: you buy more units when markets are low and fewer when markets are high, which reduces your average cost per unit over the long run.

The SIP calculator uses the future value formula: FV = P × [((1+r)ⁿ – 1) / r] × (1+r), where P is your monthly SIP amount, r is the monthly return rate, and n is the total number of months. You do not need to understand the formula — the calculator handles all of this automatically.

What you do need to understand is the assumption behind the number. The calculator uses an assumed annual return rate, typically 12% for equity mutual funds. Actual returns will vary depending on the fund you choose and market conditions. We always recommend using 11–12% for long-term equity SIP planning — conservative enough to be realistic, optimistic enough to reflect historical equity performance in India.

| Already know what SIP is? Jump straight to the goal calculator above. New to SIP? Read our complete guide: What Is SIP? |

How Much SIP Per Month for Your Goal? Real Calculations

The most common question we hear at BVB Capital is: ‘How much do I need to invest every month?’ The answer depends entirely on your goal, your time horizon, and when you start. Here are the real numbers for the most common financial goals among Kerala investors.

SIP to Reach ₹50 Lakh

Assuming a 12% annual return on a diversified equity mutual fund:

- ₹50 lakh in 10 years → Monthly SIP needed: ~₹21,000

- ₹50 lakh in 15 years → Monthly SIP needed: ~₹10,800

- ₹50 lakh in 20 years → Monthly SIP needed: ~₹5,800

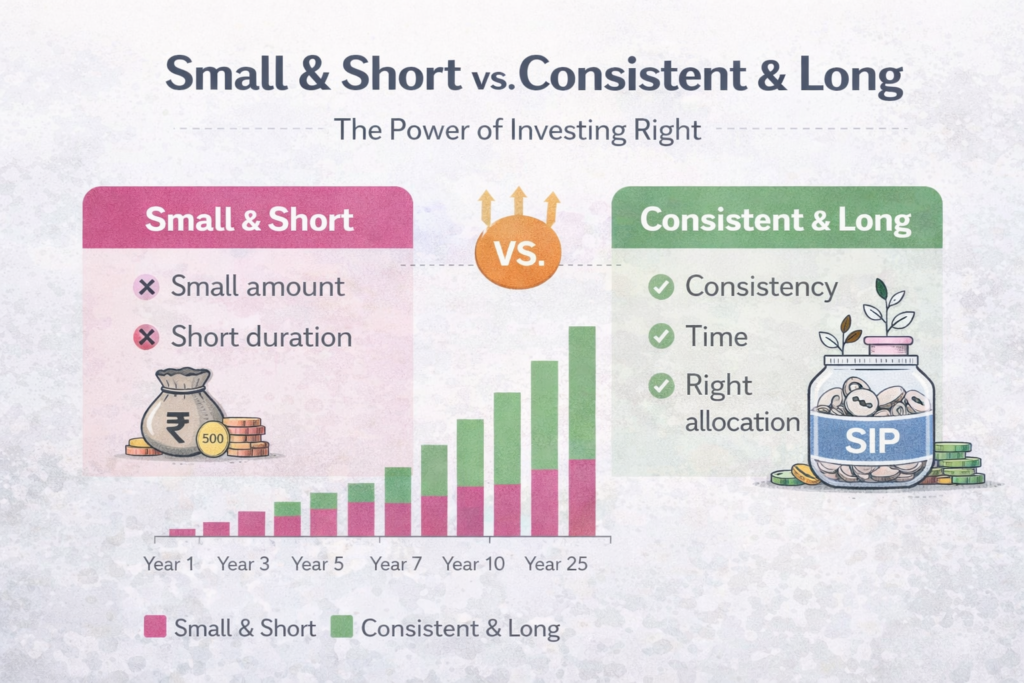

Notice how waiting just 5 extra years cuts your required monthly SIP almost in half. This is the power of compounding — and it is the single most important reason to start today, not next month.

SIP to Reach ₹1 Crore

₹1 crore is the most searched SIP goal in India. Here is what you actually need:

- ₹1 crore in 10 years → Monthly SIP needed: ~₹43,000

- ₹1 crore in 15 years → Monthly SIP needed: ~₹21,500

- ₹1 crore in 20 years → Monthly SIP needed: ~₹11,600

- ₹1 crore in 25 years → Monthly SIP needed: ~₹6,300

If ₹43,000/month seems out of reach, starting earlier and giving yourself 20–25 years makes ₹1 crore very achievable — even on a modest income.

SIP for Child’s Education (₹25 Lakh in 15 Years)

If your child is under 3 years old today, you have roughly 15 years before college. ₹25 lakh covers a decent engineering or medical degree in Kerala today — though with education inflation, you may want to target ₹35–40 lakh.

- ₹25 lakh in 15 years at 12% → Monthly SIP: ~₹5,400

- ₹35 lakh in 15 years at 12% → Monthly SIP: ~₹7,500

SIP for Retirement (₹2 Crore Corpus)

If you are 35 years old and plan to retire at 60, you have 25 years. A ₹2 crore corpus — combined with SWP (Systematic Withdrawal Plan) — can give you roughly ₹80,000–90,000 per month in retirement income.

- ₹2 crore in 25 years at 12% → Monthly SIP: ~₹14,000

- ₹2 crore in 20 years at 12% → Monthly SIP: ~₹23,200

Quick Reference: SIP amounts for common goals (at 12% annual return)

| Goal | Target Amount | Years | Return | Monthly SIP |

| Child’s education | ₹25 lakh | 15 years | 12% | ~₹5,400/month |

| Car purchase | ₹15 lakh | 7 years | 12% | ~₹11,500/month |

| Home down payment | ₹30 lakh | 10 years | 12% | ~₹13,400/month |

| Retirement corpus | ₹2 crore | 25 years | 12% | ~₹14,000/month |

| ₹50 lakh goal | ₹50 lakh | 20 years | 12% | ~₹5,800/month |

| ₹1 crore goal | ₹1 crore | 20 years | 12% | ~₹11,600/month |

| Know your number? Let’s find the right fund. WhatsApp ‘SIP Start’ to BVB Capital for a free consultation. We will match your goal, timeline, and risk appetite to the right mutual fund — at no cost to you. BVB Capital | ARN 348338 | SEBI Investor Awareness Certified | Kerala |

3 Factors That Change Your SIP Amount Dramatically

Factor 1: When You Start (The Cost of Waiting)

This is the biggest factor of all — and the one most people underestimate. Here is what it costs in monthly SIP amount to reach ₹1 crore by age 60, depending on when you begin:

| When You Start | Years to 60 | Return | Monthly SIP for ₹1 Cr | Verdict |

| Start at 25 | 35 years | 12% | ~₹3,500/month | Most affordable |

| Start at 30 | 30 years | 12% | ~₹6,000/month | Manageable |

| Start at 35 | 25 years | 12% | ~₹10,500/month | Getting expensive |

| Start at 40 | 20 years | 12% | ~₹19,000/month | Very costly delay |

| Start at 45 | 15 years | 12% | ~₹35,000/month | Extremely difficult |

Starting at 25 instead of 35 saves you ₹7,000 per month — every single month — for 25 years. That is a ₹21 lakh difference in total investment, just because of a 10-year head start. Share this table with anyone who is ‘waiting for the right time’ to start investing.

Factor 2: Expected Rate of Return

The return rate you assume in the calculator dramatically changes the output. Here is how ₹5,000/month grows over 20 years at different return rates:

- At 8% annual return: ₹29.4 lakh (debt funds, conservative)

- At 10% annual return: ₹38.3 lakh (hybrid/balanced funds)

- At 12% annual return: ₹49.9 lakh (diversified equity funds — most realistic for long-term SIPs)

- At 14% annual return: ₹66.9 lakh (aggressive small/mid cap — higher risk)

BVB Capital recommends using 11–12% for planning purposes. It reflects the long-term historical performance of well-managed Indian equity mutual funds without being overoptimistic. Always plan conservatively — if the actual returns are higher, you will simply reach your goal faster.

Factor 3: Step-Up SIP

A step-up SIP (also called a top-up SIP) automatically increases your monthly SIP by a fixed percentage each year — usually 10%. Since most people get annual salary hikes, this is a natural way to invest more without feeling the pinch. The impact on your final corpus is enormous:

- Flat ₹5,000/month for 20 years at 12% → ₹49.9 lakh

- ₹5,000/month with 10% annual step-up for 20 years at 12% → ₹1.18 crore

The same starting amount — but a step-up SIP creates more than double the corpus. We cover this in detail in our guide on Step-Up SIP (link: /step-up-sip/).

5 Common Mistakes People Make When Calculating Their SIP Goal

Mistake 1: Not Accounting for Inflation

₹1 crore sounds like a lot today. But at 6% annual inflation, its purchasing power in 20 years is equivalent to roughly ₹31 lakh today. If you are planning retirement or education 15–20 years away, always set an inflation-adjusted target — not today’s price.

| Rule of thumb Multiply your today’s cost target by 1.8 for a 10-year horizon, 2.4 for 15 years, and 3.2 for 20 years (at 6% inflation). So a ₹20 lakh engineering degree today may cost ₹64 lakh in 20 years. |

Mistake 2: Using Too Optimistic a Return Rate

Many online SIP calculators default to 15% or even 18%. This is misleading. While some funds have delivered these returns in specific periods, using 15%+ for planning leads to a shortfall. Stick to 11–12% for equity funds over a long horizon. Be pleasantly surprised, not shocked.

Mistake 3: Not Increasing Your SIP When Your Income Increases

Investors who set up a ₹3,000 SIP at age 25 and never review it are leaving enormous wealth on the table. Every time your income increases, your SIP should increase too. A 10% annual step-up does this automatically.

Mistake 4: Stopping SIP During Market Falls

This is the most costly mistake of all. When markets fall, many investors panic and stop their SIP. But a falling market is exactly when your SIP is buying more units at lower prices — that is rupee cost averaging working in your favour. Missing just the 10 best market days in a 10-year period can reduce your returns by more than 50%.

Mistake 5: Fund Overlap

Investing in five different SIPs sounds like diversification, but if all five funds hold the same large-cap stocks, you have no real diversification — only five sets of expense ratios. A proper portfolio review ensures your SIPs work together, not against each other. This is one of the key services BVB Capital provides.

Frequently Asked Questions About the SIP Calculator

Q: What is a good return rate to use in a SIP calculator?

For long-term equity SIP planning (10 years or more), use 11–12% per annum. This is based on the historical CAGR of well-diversified equity mutual funds in India over the past 15–20 years. For debt funds or conservative hybrid funds, use 7–8%.

Q: Is a SIP calculator 100% accurate?

No. The SIP calculator assumes a constant return rate every year, but actual mutual fund returns fluctuate. Think of the output as a planning estimate — a target to aim for — not a guaranteed outcome. Actual corpus may be higher or lower depending on market conditions.

Q: What is the minimum SIP amount I can start with?

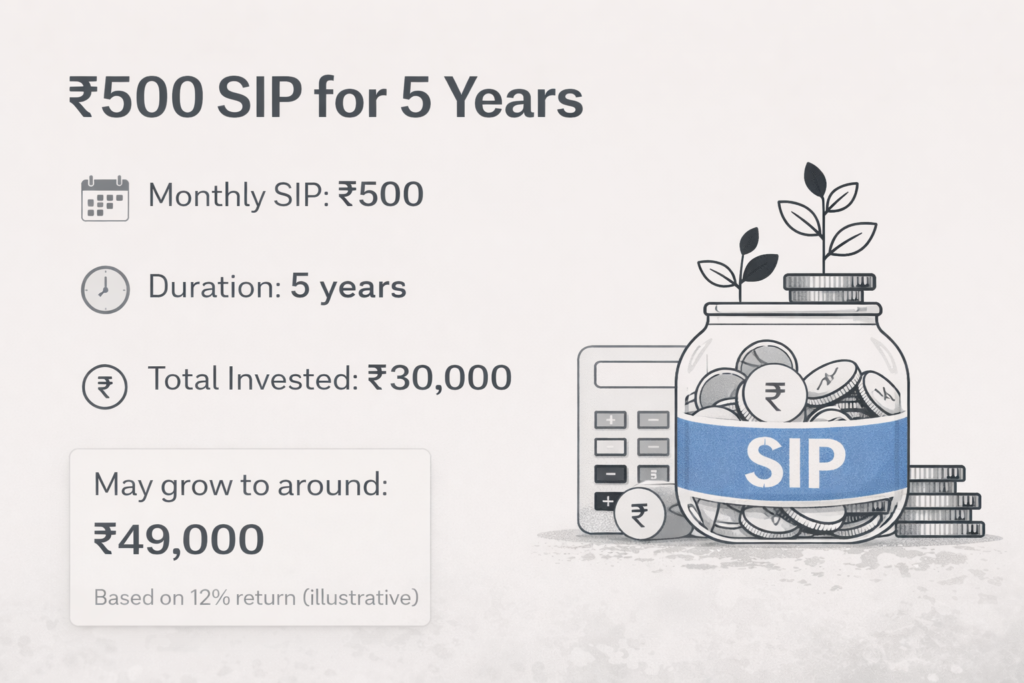

Some mutual funds allow SIPs as low as ₹100 per month. Most financial advisors, including BVB Capital, recommend starting with at least ₹500–₹1,000 to make meaningful progress toward a goal. The key is consistency, not the amount.

Q: Can I do a SIP for just 1 year?

Yes, technically you can. But equity SIPs are designed for a minimum 3-year horizon to benefit from market cycles and compounding. A 1-year equity SIP carries significant short-term market risk. For goals under 2 years, liquid funds or short-term debt funds are more appropriate.

Q: What happens if I miss a SIP instalment?

Missing one instalment is not a disaster. Most fund houses will simply skip that month and resume the next. However, consistently missing instalments defeats the purpose of disciplined investing and significantly impacts your final corpus.

Q: How do I start a SIP in Kerala?

The easiest way is to contact BVB Capital. We are based in Kerala and handle everything — KYC completion, fund selection, SIP setup, and annual portfolio review. Just WhatsApp ‘SIP Start’ to get started. There is no cost to you for our guidance.

Start Your SIP Today — Your Goal Is Closer Than You Think

Now you have the numbers. You know how much you need to invest, why starting early makes such an enormous difference, and what mistakes to avoid. The only thing left is to begin.

Every month you wait is compounding you are not getting. If you are 30 and delay starting by just 2 years, you will need to invest ₹3,000 more per month for the rest of your investment horizon to reach the same corpus. That is the real cost of waiting.

| Start your SIP with BVB Capital — free consultation WhatsApp ‘SIP Start’ to begin. We will help you choose the right fund, set up your KYC, and build a SIP plan matched to your specific goal. BVB Capital | AMFI Registered Distributor | ARN 348338 | Kerala | SEBI Investor Awareness Certified |

Explore More Guides from BVB Capital

- What is SIP? A beginner’s guide

- SIP today, SWP tomorrow: planning your retirement income

- How long should you stay invested in mutual funds?

- Is your mutual fund investment safe in India?

Disclaimer

Mutual fund investments are subject to market risks. Please read all scheme-related documents carefully before investing. Past performance is not indicative of future results. The calculations and return rates in this article are for illustration purposes only and do not constitute investment advice. BVB Capital is an AMFI Registered Mutual Fund Distributor (ARN 348338) and is not a SEBI Registered Investment Advisor. Please consult a qualified financial advisor before making investment decisions.