For many Non-Resident Indians (NRIs), investing in India is not just about returns—it is about staying connected to long-term goals such as retirement planning, family security, or future commitments back home. While real estate and fixed deposits have traditionally been popular choices, mutual funds are increasingly becoming a preferred option for NRIs seeking structured and regulated investment avenues.

This article explains how NRIs can invest in mutual funds in India, the basic requirements, and important points to understand before getting started.

Who Is Considered an NRI for Mutual Fund Investments?

An individual is classified as an NRI if they reside outside India for employment, business, or other purposes indicating an intention to stay abroad for an extended period, as defined under FEMA regulations.

NRIs, Persons of Indian Origin (PIOs), and Overseas Citizens of India (OCIs) are generally eligible to invest in Indian mutual funds, subject to compliance with applicable regulations.

Can NRIs Invest in Mutual Funds in India?

Yes, NRIs are permitted to invest in mutual funds in India. Mutual fund investments are regulated by SEBI and governed by RBI guidelines under FEMA, making them a transparent and structured option for long-term investing.

However, investment eligibility may vary slightly depending on the country of residence due to international compliance requirements.

Types of Accounts Required for NRI Mutual Fund Investment

To invest in mutual funds in India, NRIs typically need one of the following bank accounts:

NRE Account

- Funds are fully repatriable

- Suitable for investments using overseas income

NRO Account

- Used for income earned in India

- Repatriation subject to limits and applicable taxes

Mutual fund investments can be made through either account depending on the source of funds and repatriation preference.

KYC Requirements for NRIs

Before investing, NRIs must complete the Know Your Customer (KYC) process. This usually includes:

- PAN card

- Passport copy

- Overseas address proof

- Indian address proof (if available)

- Recent photograph

- FATCA / CRS declaration

KYC can be completed through digital or in-person verification depending on location and platform.

Modes of Investing: SIP or Lump Sum

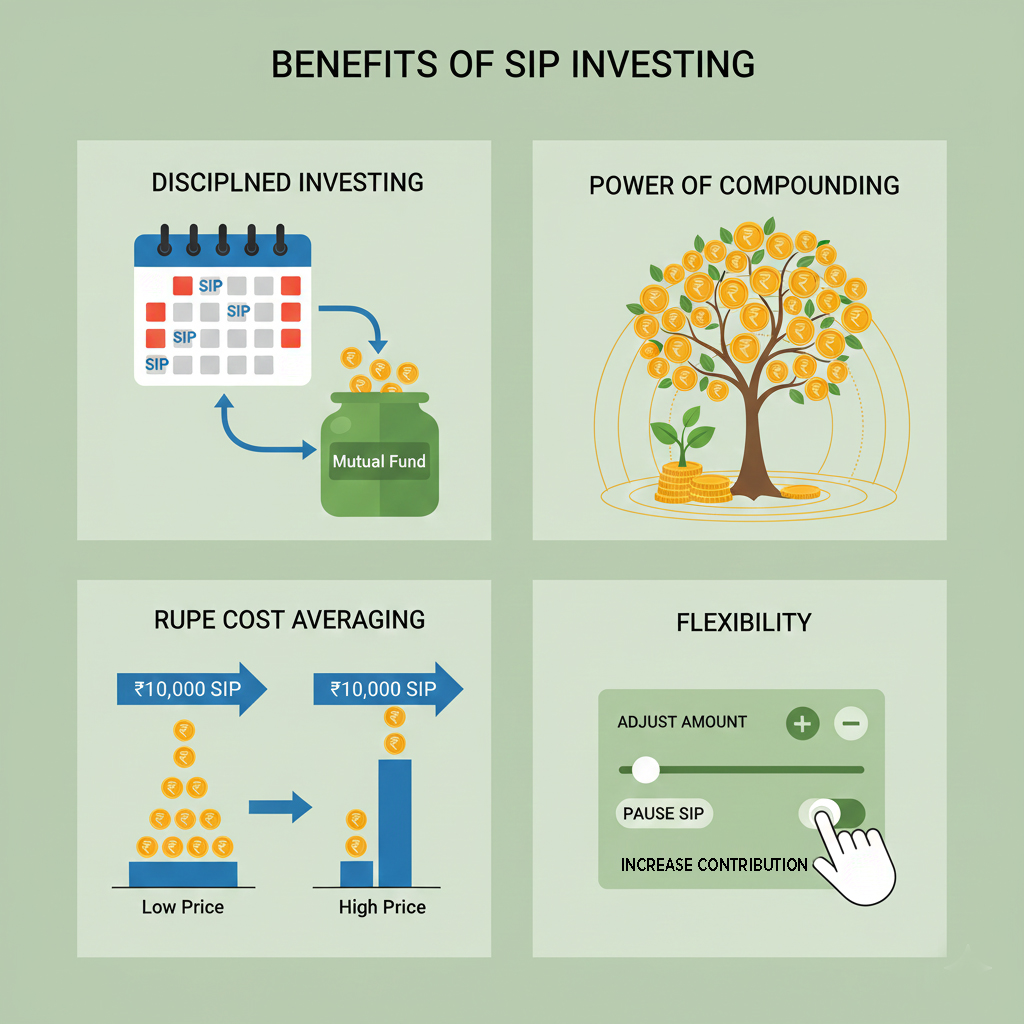

Systematic Investment Plan (SIP)

SIPs allow NRIs to invest a fixed amount regularly, making it easier to manage investments over time. SIPs encourage discipline and reduce timing-related risks.

Lump Sum Investment

Suitable when investing surplus funds at one time. Lump sum investments may require careful consideration of market conditions.

Both options are commonly used depending on individual financial planning needs.

Types of Mutual Funds Available to NRIs

NRIs can invest in most mutual fund categories, including:

- Equity mutual funds

- Debt mutual funds

- Hybrid mutual funds

- Index funds

- Tax-saving funds (ELSS, subject to eligibility)

Some fund houses may restrict investments from certain countries due to regulatory requirements.

Taxation of Mutual Funds for NRIs

Taxation for NRIs depends on the type of mutual fund and holding period. Key points include:

- Equity mutual funds and debt mutual funds are taxed differently

- Tax is deducted at source (TDS) for NRIs

- Capital gains tax applies based on applicable rules

NRIs are advised to understand tax implications and consult tax professionals if required.

Repatriation of Mutual Fund Investments

Repatriation depends on the account used for investment:

- Investments through NRE accounts are generally repatriable

- Investments through NRO accounts may have limits

Proper documentation ensures smooth repatriation when required.

Common Concerns Among NRIs

Market Risk

Mutual funds are subject to market risks. However, diversification and long-term investing help manage volatility.

Currency Risk

NRIs should consider exchange rate movements when investing or redeeming funds.

Regulatory Compliance

Investing through regulated platforms and completing documentation properly reduces compliance-related issues.

Why Mutual Funds Suit Long-Term NRI Goals

Mutual funds offer:

- Professional management

- Diversification

- Regulatory oversight

- Flexibility for long-term planning

They are particularly suitable for NRIs planning for retirement in India, future family needs, or wealth creation over extended periods.

Getting Started with NRI Mutual Fund Investments

The first step is understanding your goals, investment horizon, and risk comfort. Completing documentation, choosing the right investment mode, and maintaining discipline are key to long-term success.

Conclusion

NRI mutual fund investment is a structured and transparent way to participate in India’s long-term growth. With proper understanding, documentation, and discipline, mutual funds can play an important role in achieving long-term financial objectives.

Education and clarity remain the foundation of confident investing.