സന്ധ്യക്ക് ഒരു ചായയും കുടിച്ച് സിറ്റൗട്ടിൽ ഇരിക്കുമ്പോഴാണ് പലപ്പോഴും നമ്മൾ നിക്ഷേപങ്ങളെ കുറിച്ചും ഭാവിയിലെ സമ്പാദ്യത്തെ കുറിച്ചുമൊക്കെ ചിന്തിക്കാറുള്ളത്, അല്ലേ? പ്രത്യേകിച്ച് ഈ ഓണം ബോണസ് കിട്ടുമ്പോഴോ അല്ലെങ്കിൽ മക്കളുടെ സ്കൂൾ ബാഗും കുടയുമൊക്കെ വാങ്ങാൻ പണം തികയാതെ വരുമ്പോഴോ ഒക്കെയാകും “ഒരു നിക്ഷേപം തുടങ്ങാമായിരുന്നു” എന്ന് നമ്മൾ ആലോചിക്കുക.

അങ്ങനെ കഷ്ടപ്പെട്ട് കുറച്ച് പണം മ്യൂച്വൽ ഫണ്ടിൽ നിക്ഷേപിക്കാൻ തീരുമാനിച്ചു എന്ന് വിചാരിക്കുക. പക്ഷേ, പെട്ടെന്ന് ഒരാൾ വന്ന് ചോദിക്കുന്നു, “നിങ്ങളുടെ കെ.വൈ.സി (KYC) ഓക്കെയാണോ?” എന്ന്. അപ്പോൾ നമ്മൾ ഒന്ന് അമ്പരക്കും. ഇതെന്ത് സാധനമാണെന്ന് പലരും ചോദിക്കാറുണ്ട്. പേടിക്കേണ്ട, നമ്മുടെ നാട്ടിലെ ബാങ്കിൽ അക്കൗണ്ട് തുടങ്ങുന്നതുപോലെ ലളിതമായ ഒരു കാര്യമാണിത്. ഇന്ന് നമ്മൾ സംസാരിക്കാൻ പോകുന്നത് മ്യൂച്വൽ ഫണ്ട് നിക്ഷേപകർ അറിഞ്ഞിരിക്കേണ്ട കെ.വൈ.സി വിശേഷങ്ങളെ കുറിച്ചാണ്.

നമ്മൾ മലയാളികൾക്ക് എന്നും സമ്പാദ്യശീലം കുറച്ച് കൂടുതലാണ്. ചിട്ടിയും സ്വർണ്ണവും ഒക്കെ കഴിഞ്ഞാൽ ഇപ്പോൾ നമ്മുടെ ഇടയിൽ ട്രെൻഡ് ആയിക്കൊണ്ടിരിക്കുന്നത് മ്യൂച്വൽ ഫണ്ടുകളാണ്. എന്നാൽ നിക്ഷേപം തുടങ്ങുന്നതിന് മുൻപോ അല്ലെങ്കിൽ നിലവിലുള്ള നിക്ഷേപം സുഗമമായി മുന്നോട്ട് കൊണ്ടുപോകാനോ ഈ ‘കെ.വൈ.സി’ കൃത്യമായിരിക്കണം. ഇതിനെക്കുറിച്ച് ലളിതമായി താഴെ വിവരിക്കാം.

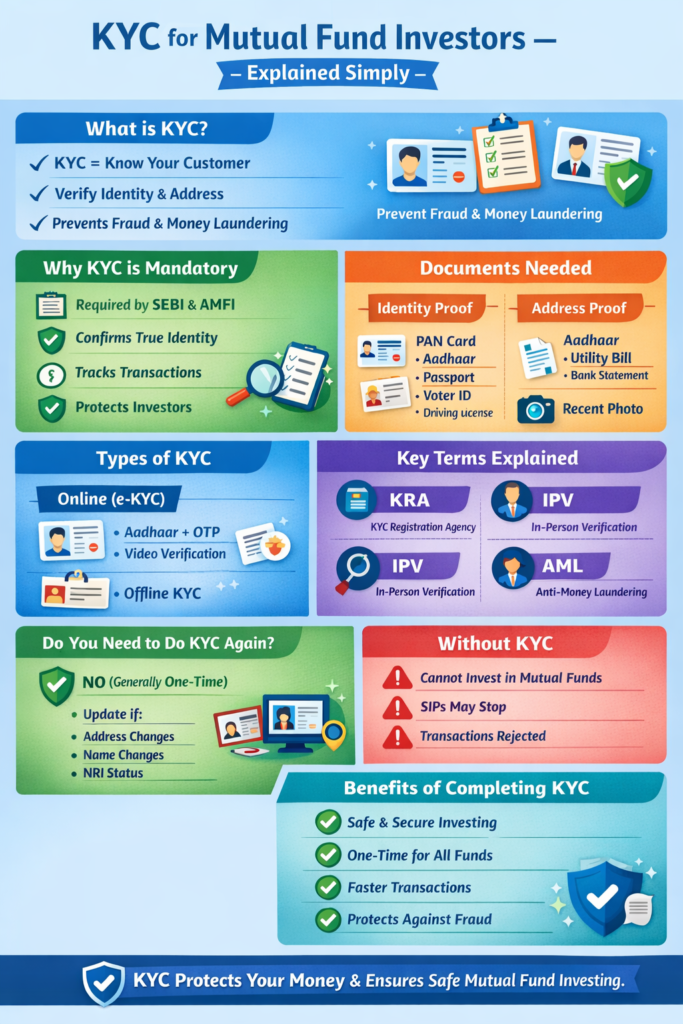

എന്താണ് ഈ കെ.വൈ.സി (KYC)?

ലളിതമായി പറഞ്ഞാൽ ‘നിങ്ങളുടെ ഇടപാടുകാരനെ അറിയുക’ (Know Your Customer) എന്നാണ് ഇതിന്റെ അർത്ഥം. നമ്മൾ സ്കൂളിൽ ചേരുമ്പോൾ ജനന സർട്ടിഫിക്കറ്റും ഫോട്ടോയും ഒക്കെ കൊടുക്കാറില്ലേ? അതുപോലെ തന്നെയാണ് ഇതും. നിങ്ങൾ ആരാണെന്നും എവിടെയാണ് താമസമെന്നും നിക്ഷേപിക്കുന്ന പണം നിയമപരമാണെന്നും ഉറപ്പുവരുത്താൻ സർക്കാർ ഏർപ്പെടുത്തിയ ഒരു സംവിധാനമാണിത്. കള്ളപ്പണം വെളുപ്പിക്കുന്നത് തടയാനും നിങ്ങളുടെ പണം സുരക്ഷിതമാണെന്ന് ഉറപ്പാക്കാനും ഇത് സഹായിക്കുന്നു.

കെ.വൈ.സി സ്റ്റാറ്റസുകൾ: നിങ്ങൾ എവിടെ നിൽക്കുന്നു?

നിങ്ങൾ ഇതിനോടകം നിക്ഷേപം തുടങ്ങിയ ആളാണെങ്കിൽ നിങ്ങളുടെ കെ.വൈ.സി സ്റ്റാറ്റസ് ഒന്ന് പരിശോധിക്കുന്നത് നല്ലതാണ്. സാധാരണയായി മൂന്ന് തരം സ്റ്റാറ്റസുകളാണ് ഉള്ളത്. അത് താഴെ പറയുന്നവയാണ്:

| സ്റ്റാറ്റസ് (Status) | ഇതിന്റെ അർത്ഥം എന്താണ്? | നിങ്ങൾ എന്ത് ചെയ്യണം? |

| KYC Validated | എല്ലാം പെർഫെക്റ്റാണ്! ആധാർ കാർഡും പാൻ കാർഡും കൃത്യമായി ലിങ്ക് ചെയ്തിട്ടുണ്ട്. | നിങ്ങൾക്ക് പുതിയ നിക്ഷേപങ്ങൾ തുടങ്ങാം, പണം പിൻവലിക്കാം. പേടിക്കേണ്ടതില്ല. |

| KYC Registered | നിങ്ങളുടെ വിവരങ്ങൾ ഉണ്ട്, പക്ഷേ ആധാർ വഴി വീണ്ടും ഒന്ന് ഉറപ്പിക്കേണ്ടതുണ്ട്. | പഴയ നിക്ഷേപം തുടരാം, പക്ഷേ പുതിയ ഫണ്ടുകളിൽ നിക്ഷേപിക്കണമെങ്കിൽ വീണ്ടും വാലിഡേഷൻ വേണം. |

| KYC On-Hold | എന്തോ ഒരു പ്രശ്നമുണ്ട്. ഒന്നുകിൽ ഫോൺ നമ്പർ തെറ്റാണ് അല്ലെങ്കിൽ രേഖകൾ അപൂർണ്ണമാണ്. | ഉടനെ തന്നെ രേഖകൾ പുതുക്കണം. അല്ലെങ്കിൽ നിങ്ങളുടെ നിക്ഷേപം തടസ്സപ്പെടും. |

നിക്ഷേപം തുടങ്ങാൻ എന്തൊക്കെ വേണം? (Checklist)

നമ്മൾ ഒരു യാത്ര പോകുമ്പോൾ ബാഗിൽ എടുക്കേണ്ട കാര്യങ്ങൾ മറക്കാറില്ലല്ലോ? അതുപോലെ മ്യൂച്വൽ ഫണ്ട് കെ.വൈ.സി ചെയ്യാൻ താഴെ പറയുന്ന കാര്യങ്ങൾ കയ്യിൽ കരുതുക:

- പാൻ കാർഡ് (PAN Card): നിക്ഷേപങ്ങളുടെ കാര്യത്തിൽ ഇതാണ് നമ്മുടെ പ്രധാന തിരിച്ചറിയൽ രേഖ.

- ആധാർ കാർഡ് (Aadhaar Card): വിലാസം തെളിയിക്കാനായി ഇത് അത്യാവശ്യമാണ്.

- ഫോട്ടോ: നിങ്ങളുടെ ഒരു പാസ്പോർട്ട് സൈസ് ഫോട്ടോ.

- ഫോൺ നമ്പറും ഇമെയിലും: ആധാറുമായി ലിങ്ക് ചെയ്ത ഫോൺ നമ്പർ തന്നെ നൽകാൻ ശ്രദ്ധിക്കുക.

- ഡിജിറ്റൽ സിഗ്നേച്ചർ: ഓൺലൈനായി ചെയ്യുമ്പോൾ വെളുത്ത പേപ്പറിൽ ഒപ്പിട്ട് അത് സ്കാൻ ചെയ്ത് നൽകേണ്ടി വരും.

കെ.വൈ.സി അപ്ഡേറ്റ് ചെയ്യാനുള്ള എളുപ്പവഴികൾ

ഇതൊക്കെ ചെയ്യാൻ ഇനി ഓഫീസുകൾ കയറി ഇറങ്ങേണ്ട കാലം കഴിഞ്ഞു. വീട്ടിലിരുന്ന് ചായ കുടിച്ചു കൊണ്ട് തന്നെ നമുക്ക് ഇത് ചെയ്യാം.

- ഓൺലൈൻ വഴി (e-KYC): ഏതെങ്കിലും മ്യൂച്വൽ ഫണ്ട് ഹൗസിന്റെ വെബ്സൈറ്റിലോ കെ.ആർ.എ (KRA – KYC Registration Agency) വെബ്സൈറ്റിലോ കയറി ആധാർ ഉപയോഗിച്ച് ഒടിപി (OTP) വഴി കെ.വൈ.സി പൂർത്തിയാക്കാം. നമ്മുടെ ഫോണിൽ മെസ്സേജ് വരുന്നത് നോക്കി ടൈപ്പ് ചെയ്താൽ മതി, സംഗതി സിമ്പിൾ!

- ഓഫ്ലൈൻ വഴി: നിങ്ങൾക്ക് നേരിട്ട് പോകാനാണ് താൽപ്പര്യമെങ്കിൽ അപേക്ഷാ ഫോം പൂരിപ്പിച്ച് രേഖകളുടെ കോപ്പികൾ സഹിതം ഏതെങ്കിലും ഇൻവെസ്റ്റ്മെന്റ് സെന്ററിലോ മ്യൂച്വൽ ഫണ്ട് ഓഫീസിലോ നൽകാം.

എന്തുകൊണ്ട് ഇത് ഇപ്പോൾ ചെയ്യണം?

“പിന്നെ ചെയ്യാം” എന്ന് കരുതി മാറ്റി വെക്കുന്ന ശീലം നമുക്ക് പൊതുവെ ഉണ്ടല്ലോ. എന്നാൽ കെ.വൈ.സി കാര്യത്തിൽ അത് വലിയ പണിയാകും.

- SIP മുടങ്ങും: നിങ്ങൾ മാസം തോറും ചെറിയ തുക നിക്ഷേപിക്കുന്ന ആളാണെങ്കിൽ (SIP), കെ.വൈ.സി പ്രശ്നമാണെങ്കിൽ ബാങ്കിൽ നിന്ന് പണം പോകുന്നത് നിൽക്കും.

- പണം പിൻവലിക്കാൻ കഴിയില്ല: അത്യാവശ്യ ഘട്ടത്തിൽ മ്യൂച്വൽ ഫണ്ടിൽ നിന്ന് പണം എടുക്കാൻ നോക്കുമ്പോൾ കെ.വൈ.സി തടസ്സമായാൽ അത് വലിയ ബുദ്ധിമുട്ടാകും.

- പുതിയ നിക്ഷേപം നടക്കില്ല: നല്ലൊരു അവസരം വരുമ്പോൾ പുതിയ ഫണ്ടുകളിൽ പണം ഇടാൻ നിങ്ങൾക്ക് കഴിയില്ല.

നമ്മുടെ സമ്പാദ്യം സുരക്ഷിതമായിരിക്കാൻ നിയമപരമായ ഇത്തരം കാര്യങ്ങൾ കൃത്യമായി പാലിക്കേണ്ടതുണ്ട്. സ്കൂൾ ബാഗ് അടുക്കി വെക്കുന്നതുപോലെ തന്നെ പ്രധാനമാണ് നമ്മുടെ നിക്ഷേപ രേഖകളും വൃത്തിയായി സൂക്ഷിക്കുന്നത്. കെ.വൈ.സി സ്റ്റാറ്റസ് ‘Validated’ ആണെന്ന് ഉറപ്പുവരുത്തിയാൽ നിങ്ങൾക്ക് സമാധാനമായി ഉറങ്ങാം.

ഇതുമായി ബന്ധപ്പെട്ട് നിങ്ങൾക്ക് എന്തെങ്കിലും സംശയങ്ങൾ ഉണ്ടെങ്കിൽ കമന്റ് ചെയ്യുകയോ അല്ലെങ്കിൽ നിങ്ങളുടെ സാമ്പത്തിക ഉപദേശകനോട് ചോദിക്കുകയോ ചെയ്യാം. നിക്ഷേപം തുടങ്ങാൻ ഇനിയും വൈകിക്കരുത്!

പതിവായി ചോദിക്കുന്ന ചോദ്യങ്ങൾ (FAQ)

1. ആധാർ ഇല്ലാതെ കെ.വൈ.സി ചെയ്യാൻ പറ്റുമോ?

പറ്റും, വോട്ടർ ഐഡിയോ പാസ്പോർട്ടോ ഒക്കെ ഉപയോഗിക്കാം. പക്ഷേ, ഇപ്പോൾ എല്ലാം ഡിജിറ്റൽ ആയതുകൊണ്ട് ആധാർ ഉപയോഗിക്കുന്നതാണ് ഏറ്റവും എളുപ്പവും വേഗമേറിയതും.

2. കെ.വൈ.സി ചെയ്യാൻ പണം നൽകണോ?

ഒരിക്കലുമില്ല! മ്യൂച്വൽ ഫണ്ട് കെ.വൈ.സി തികച്ചും സൗജന്യമാണ്. ഇതിനായി ആരെങ്കിലും പണം ചോദിച്ചാൽ കൊടുക്കരുത്.

3. പാൻ കാർഡും ആധാറും ലിങ്ക് ചെയ്യേണ്ടത് നിർബന്ധമാണോ?

അതെ, തീർച്ചയായും! ഇവ രണ്ടും ലിങ്ക് ചെയ്തിട്ടില്ലെങ്കിൽ നിങ്ങളുടെ പാൻ കാർഡ് അസാധുവാകാൻ സാധ്യതയുണ്ട്. അത് നിങ്ങളുടെ നിക്ഷേപത്തെ ബാധിക്കും.

4. എത്ര ദിവസം കൊണ്ട് കെ.വൈ.സി പൂർത്തിയാകും?

ഓൺലൈൻ വഴിയാണെങ്കിൽ സാധാരണ 3 മുതൽ 5 പ്രവൃത്തി ദിവസങ്ങൾക്കുള്ളിൽ സ്റ്റാറ്റസ് അപ്ഡേറ്റ് ആകും. ചിലപ്പോൾ അതിലും വേഗത്തിൽ നടന്നേക്കാം.

5. ഞാൻ നേരത്തെ കെ.വൈ.സി ചെയ്തതാണ്, ഇനി വീണ്ടും ചെയ്യണോ?

നിങ്ങളുടെ സ്റ്റാറ്റസ് ‘Validated’ ആണെങ്കിൽ വീണ്ടും ചെയ്യേണ്ടതില്ല. എന്നാൽ വിലാസമോ ഫോൺ നമ്പറോ മാറിയിട്ടുണ്ടെങ്കിൽ അത് അപ്ഡേറ്റ് ചെയ്യുന്നത് നല്ലതാണ്.

നിങ്ങളുടെ നിക്ഷേപ യാത്ര സന്തോഷകരമാകട്ടെ!