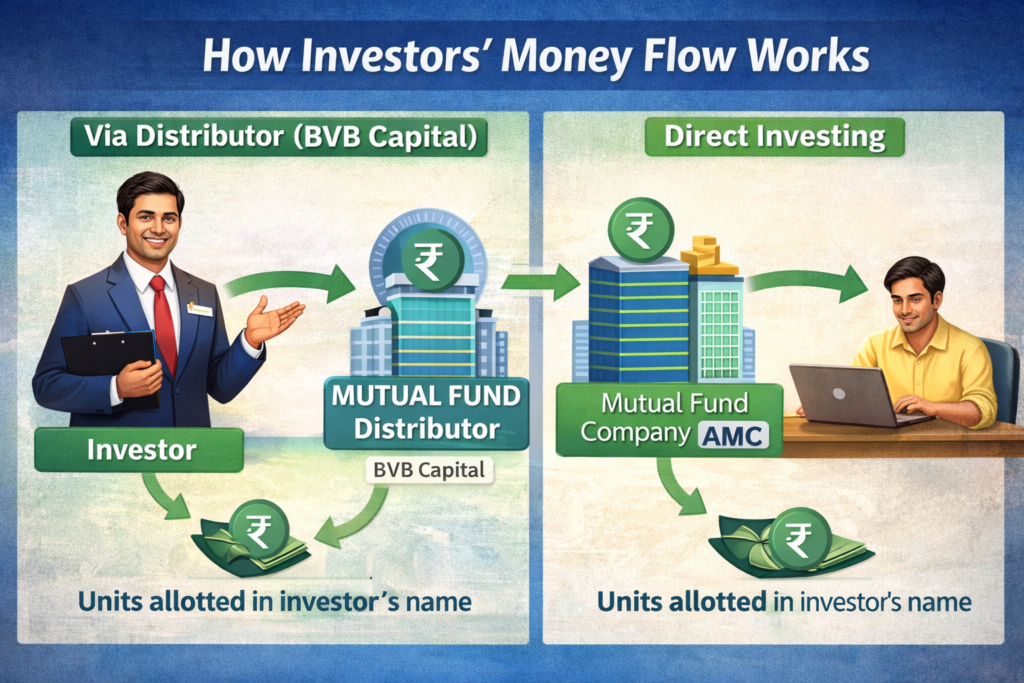

Imagine you want to travel to a new city. You can go alone using Google Maps, or you can take the help of a guide who knows the best routes, risks, and shortcuts. Investing in mutual funds is very similar.

A Mutual Fund Distributor (MFD) is like your trusted guide in the investment journey. At BVB Capital Private Limited, we help individuals invest in a simple, safe, and goal-based manner without confusion or stress.

This article will clearly explain:

How a mutual fund distributor functions

What services BVB Capital provides

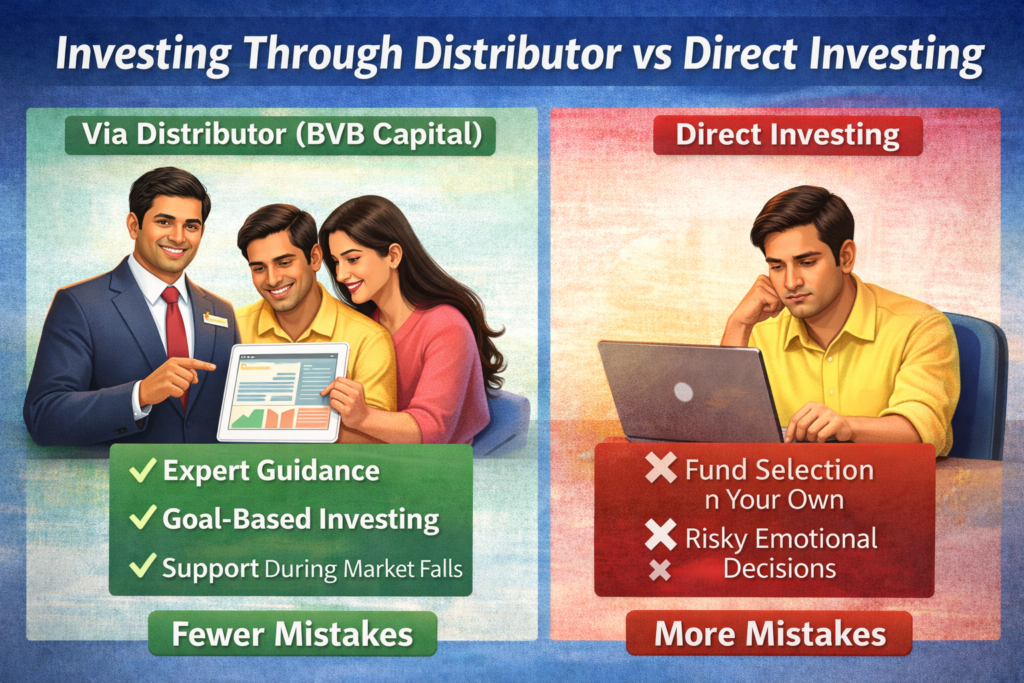

Why investing through a distributor is better than direct investing

The truth about money safety and transparency

What Does a Mutual Fund Distributor Actually Do?

A mutual fund distributor does not create mutual funds. Mutual funds are managed by big regulated companies called Asset Management Companies (AMCs) such as SBI Mutual Fund, HDFC Mutual Fund, ICICI Prudential, etc.

നമ്മുടെ ജീവിതത്തിലെ ഏറ്റവും സമാധാനപരമായ കാലഘട്ടമാകണം റിട്ടയർമെന്റ് കാലം. ഓടിത്തളർന്ന ജോലിത്തിരക്കുകളിൽ നിന്ന് മാറി, കുടുംബത്തോടൊപ്പം സമയം ചിലവഴിക്കാൻ ആഗ്രഹിക്കുന്ന സമയം. എന്നാൽ പലരെയും ഈ ഘട്ടത്തിൽ അലട്ടുന്ന പ്രധാന പ്രശ്നം മറ്റൊന്നാണ്: “മാസം തോറും കയ്യിൽ വന്നിരുന്ന ശമ്പളം ഇനി എങ്ങനെ ലഭിക്കും?”

ജോലിയിൽ നിന്നൊക്കെ വിരമിച്ചു കഴിയുമ്പോൾ… ആലോചിക്കുമ്പോൾ തന്നെ ഒരു ആധി വരും. മാസം മാസം വന്നിരുന്ന ശമ്പളം നിൽക്കും, എന്നാൽ ചെലവുകൾ നിൽക്കുമോ? ഓണത്തിന് പുതിയ മുണ്ടും സാരിയും എടുക്കണം, കൊച്ചുമക്കൾക്ക് വിഷുക്കൈനീട്ടം കൊടുക്കണം, അസുഖങ്ങൾ വന്നാൽ ആശുപത്രിയിൽ പോകണം.

ഇതിനൊക്കെ മക്കളുടെ മുന്നിൽ കൈനീട്ടാതെ, നമ്മൾ കഷ്ടപ്പെട്ട് സമ്പാദിച്ച പണം തന്നെ നമുക്ക് ഒരു ‘മാസശമ്പളം’ പോലെ തന്നാലോ? അതിനെക്കുറിച്ചാണ് ഇന്ന് ഞാൻ പറയാൻ പോകുന്നത്. സംഗതിയുടെ പേര് ‘SWP’ എന്നാണ്. പേര് കേട്ട് പേടിക്കണ്ട, നമുക്ക് ഇത് ലളിതമായി ഒന്ന് നോക്കാം.

ജോലി ഉള്ളപ്പോൾ മാസം ഒന്നാം തീയതി മൊബൈലിൽ വരുന്ന ആ ‘സാലറി മെസ്സേജ്‘ ഉണ്ടല്ലോ, അത് നൽകുന്ന ഒരു സമാധാനം ഒന്ന് വേറെ തന്നെയാണ്. റിട്ടയർമെന്റിന് ശേഷം ആ സമാധാനം നമുക്ക് നഷ്ടപ്പെടുമോ എന്ന് നിങ്ങൾ ചിന്തിച്ചിട്ടുണ്ടോ? ബാങ്കിൽ പണം ഇട്ടാൽ പലിശ കിട്ടും, ശരിയാണ്. പക്ഷേ വിലക്കയറ്റം കൂടുന്ന ഈ കാലത്ത് ആ പലിശ മാത്രം മതിയോ? ഇവിടെയാണ് SWP (Systematic Withdrawal Plan) എന്ന സൂത്രപ്പണി നമുക്ക് തുണയാകുന്നത്.

എന്താണ് ഈ ‘സിസ്റ്റമാറ്റിക് വിത്ത്ഡ്രോവൽ പ്ലാൻ’ (SWP)?

നമ്മൾ മ്യൂച്വൽ ഫണ്ടിൽ പണം നിക്ഷേപിക്കുന്ന ‘SIP’ (എസ്.ഐ.പി)യെ കുറിച്ച് കേട്ടിട്ടുണ്ടാകുമല്ലോ. ഓരോ മാസവും നമ്മുടെ അക്കൗണ്ടിൽ നിന്ന് പണം ഫണ്ടിലേക്ക് പോകുന്ന രീതിയാണത്. ഇതിന്റെ നേരെ വിപരീതമാണ് SWP.

അതായത്, നമ്മുടെ കയ്യിലുള്ള ഒരു വലിയ തുക (ഉദാഹരണത്തിന് റിട്ടയർമെന്റ് ആനുകൂല്യങ്ങൾ) മ്യൂച്വൽ ഫണ്ടിൽ നിക്ഷേപിക്കുന്നു. എന്നിട്ട് നമ്മൾ പറയുന്നു, “എനിക്ക് എല്ലാ മാസവും ഇതിൽ നിന്ന് ഇത്ര രൂപ വീതം തിരിച്ചു തരണം”. ബാക്കി പണം അവിടെ കിടന്ന് വളരുകയും ചെയ്യും, നമുക്ക് ആവശ്യത്തിന് പണം മാസം മാസം അക്കൗണ്ടിൽ വരികയും ചെയ്യും.

നമ്മുടെ വീട്ടിലെ വാട്ടർ ടാങ്ക് പോലെ ഒന്ന് സങ്കൽപ്പിച്ചു നോക്കൂ. ടാങ്ക് നിറയെ വെള്ളമുണ്ട് (നിങ്ങളുടെ നിക്ഷേപം). അതിൽ നിന്ന് ഒരു ചെറിയ ടാപ്പ് തുറന്ന് നമുക്ക് ആവശ്യമുള്ള വെള്ളം മാത്രം എടുക്കുന്നു. പെയ്യുന്ന മഴയത്ത് ടാങ്ക് വീണ്ടും നിറയുന്നു (മാർക്കറ്റിലെ ലാഭം). ഇതാണ് ലളിതമായി പറഞ്ഞാൽ SWP.

ഇത് മനസ്സിലാക്കാൻ താഴെ പറയുന്ന ടേബിൾ ഒന്ന് നോക്കൂ:

പ്രത്യേകതകൾ

SIP (എസ്.ഐ.പി)

SWP (എസ്.ഡബ്ല്യു.പി)

പ്രധാന ലക്ഷ്യം

പണം സമ്പാദിക്കുക (Wealth Creation)

വരുമാനം കണ്ടെത്തുക (Regular Income)

പണത്തിന്റെ ഒഴുക്ക്

ബാങ്കിൽ നിന്ന് ഫണ്ടിലേക്ക്

ഫണ്ടിൽ നിന്ന് ബാങ്കിലേക്ക്

ആർക്ക് ഗുണകരം

ജോലി ഉള്ളവർക്കും യുവാക്കൾക്കും

വിരമിച്ചവർക്കും സ്ഥിരവരുമാനം വേണ്ടവർക്കും

സൗകര്യം

ഓരോ മാസവും ചെറിയ തുക നിക്ഷേപിക്കാം

ഓരോ മാസവും നിശ്ചിത തുക പിൻവലിക്കാം

റിട്ടയർമെന്റ് കാലത്ത് SWP തിരഞ്ഞെടുക്കാൻ 5 പ്രധാന കാരണങ്ങൾ

എന്തിനാണ് ബാങ്ക് ഡിപ്പോസിറ്റിന് പകരം നമ്മൾ ഇത് നോക്കുന്നത് എന്ന് നിങ്ങൾ ചോദിച്ചേക്കാം. അതിന് പ്രധാനമായും അഞ്ച് കാരണങ്ങളാണുള്ളത്:

വിലക്കയറ്റത്തെ തോൽപ്പിക്കാം: പണ്ട് പത്ത് രൂപയ്ക്ക് കിട്ടിയിരുന്ന സാധനങ്ങൾ ഇന്ന് വാങ്ങാൻ നൂറ് രൂപ വേണം. ഇതിനെയാണ് ഇൻഫ്ലേഷൻ (Inflation) എന്ന് പറയുന്നത്. സാധാരണ സേവിങ്സ് സ്കീമുകളെക്കാൾ മികച്ച ലാഭം തരാൻ മ്യൂച്വൽ ഫണ്ടുകൾക്ക് സാധിക്കാറുണ്ട്. ഇതുമായി ബന്ധപ്പെട്ട് നിക്ഷേപങ്ങൾ എങ്ങനെ വളർത്താം എന്നതിനെക്കുറിച്ച് കൂടുതൽ വായിക്കാവുന്നതാണ്.

നികുതി ലാഭം (Tax Efficiency): ഇതാണ് ഏറ്റവും വലിയ പ്രത്യേകത! ബാങ്ക് പലിശയ്ക്ക് നമ്മൾ വലിയൊരു തുക ടാക്സ് കൊടുക്കേണ്ടി വരും. എന്നാൽ SWP-യിൽ നമ്മൾ പിൻവലിക്കുന്ന തുകയുടെ ലാഭത്തിന് മാത്രമാണ് ചെറിയൊരു ടാക്സ് വരുന്നത്.

പണം നമ്മുടെ കയ്യിൽ: നിങ്ങൾക്ക് ഈ മാസം 10,000 രൂപ മതി, അടുത്ത മാസം ഒരു യാത്ര പോകാൻ 15,000 രൂപ വേണം എന്ന് വിചാരിക്കുക. നിങ്ങൾക്ക് വളരെ എളുപ്പത്തിൽ പിൻവലിക്കുന്ന തുകയിൽ മാറ്റം വരുത്താം. നിക്ഷേപം പൂർണ്ണമായും നിർത്തണമെന്നുണ്ടെങ്കിൽ അതിനും തടസ്സമില്ല.

മുതൽ നശിക്കാതെ സംരക്ഷിക്കാം: നമ്മൾ പിൻവലിക്കുന്നത് ലാഭത്തേക്കാൾ കുറഞ്ഞ തുകയാണെങ്കിൽ, കാലക്രമേണ നമ്മുടെ നിക്ഷേപിച്ച തുക (Principal) കൂടി വരുന്നത് കാണാം.

ഓരോ മാസവും കൃത്യമായ വരുമാനം: കൃത്യം ഒന്നാം തീയതി പണം അക്കൗണ്ടിലെത്തും.

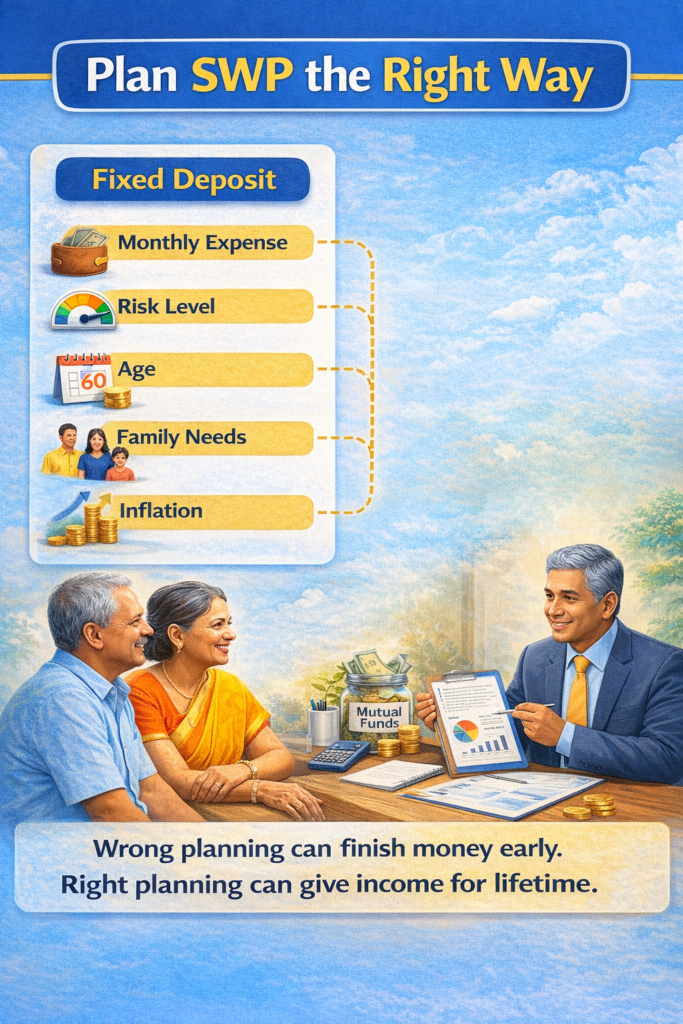

ഒരു ശരിയായ SWP പ്ലാൻ എങ്ങനെ തയ്യാറാക്കാം? (5 ലളിതമായ ഘട്ടങ്ങൾ)

നിങ്ങൾ ഇത് തുടങ്ങാൻ ആഗ്രഹിക്കുന്നുവെങ്കിൽ ഈ രീതി പിന്തുടരാം:

ശരിയായ ഫണ്ട് തിരഞ്ഞെടുക്കുക: റിട്ടയർമെന്റ് കാലമായതുകൊണ്ട് അമിത റിസ്ക് എടുക്കാതിരിക്കുക. ഇക്വിറ്റിയും ഡെറ്റും കലർന്ന ‘ഹൈബ്രിഡ് ഫണ്ടുകൾ’ ഇതിനായി തിരഞ്ഞെടുക്കാം.

പിൻവലിക്കേണ്ട തുക നിശ്ചയിക്കുക: സാധാരണയായി നിങ്ങളുടെ മൊത്തം നിക്ഷേപത്തിന്റെ 6% മുതൽ 8% വരെ മാത്രം വർഷത്തിൽ പിൻവലിക്കുന്നതാണ് ബുദ്ധി. ഉദാഹരണത്തിന്, 10 ലക്ഷം രൂപ ഇട്ടാൽ മാസം 5,000 – 6,000 രൂപ പിൻവലിക്കാം.

ദിവസം തിരഞ്ഞെടുക്കുക: എല്ലാ മാസവും ഏത് തീയതിയിലാണ് പണം വേണ്ടതെന്ന് നിങ്ങൾക്ക് തീരുമാനിക്കാം. അന്ന് പണം കൃത്യമായി നിങ്ങളുടെ ബാങ്ക് അക്കൗണ്ടിലേക്ക് വരും.

ഒരു എമർജൻസി ഫണ്ട് കരുതുക: എല്ലാ പണവും എടുത്ത് മ്യൂച്വൽ ഫണ്ടിൽ ഇടരുത്. പെട്ടെന്ന് ഒരു ആവശ്യം വന്നാൽ എടുക്കാൻ കുറച്ചു പണം സേവിങ്സ് അക്കൗണ്ടിലോ കയ്യിലോ വെക്കുക.

ക്ഷമ വേണം: ഷെയർ മാർക്കറ്റിൽ ചെറിയ മാറ്റങ്ങൾ വരുമ്പോൾ പേടിച്ച് നിക്ഷേപം പിൻവലിക്കരുത്. ഇതൊരു ദീർഘകാല പദ്ധതിയാണെന്ന് എപ്പോഴും ഓർക്കുക.

ഉദാഹരണത്തിന്:

നിങ്ങളുടെ കൈവശം 50 ലക്ഷം രൂപ ഉണ്ടെന്ന് കരുതുക.

നിക്ഷേപം

വാർഷിക പിൻവലിക്കൽ (%)

മാസ വരുമാനം

₹ 50,00,000

6%

₹ 25,000

₹ 50,00,000

8%

₹ 33,333

ഇതുപോലെ പിൻവലിച്ചാൽ ബാക്കി തുക ഫണ്ടിൽ കിടന്ന് വളരാൻ അവസരം ലഭിക്കും.

ബാങ്ക് എഫ്ഡിയും (FD) എസ്ഡബ്ല്യുപി (SWP)-യും തമ്മിലുള്ള വ്യത്യാസം

പലരും റിട്ടയർമെന്റ് തുക എഫ്ഡിയിൽ ഇടാനാണ് ആഗ്രഹിക്കുന്നത്. എന്നാൽ എഫ്ഡിയിൽ നിന്നുള്ള പലിശ മുഴുവനായും നിങ്ങളുടെ ടാക്സ് സ്ലാബ് അനുസരിച്ച് നികുതിക്ക് വിധേയമാണ്. എന്നാൽ SWP-യിൽ നികുതി ലാഭത്തോടൊപ്പം നിക്ഷേപിച്ച തുക (Principal) വളരാനുള്ള സാധ്യതയും കൂടുതലാണ്.

ആർക്കൊക്കെ ഇത് അനുയോജ്യമാണ്?

റിട്ടയർമെന്റ് ജീവിതം ആസ്വദിക്കാൻ ആഗ്രഹിക്കുന്നവർ.

സ്ഥിരമായ മാസവരുമാനം ആഗ്രഹിക്കുന്ന വീട്ടമ്മമാർ.

കയ്യിലുള്ള വലിയൊരു തുക സുരക്ഷിതമായി നിക്ഷേപിച്ച് അതിൽ നിന്ന് ലാഭം എടുക്കാൻ ആഗ്രഹിക്കുന്നവർ.

18 വയസ്സിന് മുകളിലുള്ളവർ ഇത് വായിക്കുന്നത് എന്തിന്?

നിങ്ങൾ ഇപ്പോൾ കൗമാരപ്രായത്തിലാണെങ്കിൽ, റിട്ടയർമെന്റിനെ കുറിച്ച് ചിന്തിക്കാൻ സമയമായില്ല എന്ന് തോന്നാം. എന്നാൽ ‘കോമ്പൗണ്ടിംഗ്’ എന്ന അത്ഭുതം പ്രവർത്തിക്കാൻ സമയം ആവശ്യമാണ്. ചെറുപ്പത്തിലേ ചെറിയ തുകകൾ SIP വഴി നിക്ഷേപിച്ചു തുടങ്ങിയാൽ, റിട്ടയർമെന്റ് കാലത്ത് കോടികളുടെ ഒരു നിക്ഷേപം (Corpus) ഉണ്ടാക്കാൻ നിങ്ങൾക്ക് സാധിക്കും. ആ തുക ഉപയോഗിച്ച് പിന്നീട് മാസം തോറും ലക്ഷങ്ങൾ SWP വഴി സ്വന്തമാക്കാം.

എങ്ങനെ തുടങ്ങാം?

ഒരു മികച്ച റിട്ടയർമെന്റ് പ്ലാൻ തയ്യാറാക്കാൻ കൃത്യമായ ലക്ഷ്യബോധം വേണം. നിങ്ങളുടെ നിക്ഷേപ ലക്ഷ്യങ്ങൾക്കും റിസ്ക് എടുക്കാനുള്ള ശേഷിക്കും അനുസരിച്ചുള്ള ഫണ്ടുകൾ തിരഞ്ഞെടുക്കാൻ ബിവിബി ക്യാപിറ്റലിലെ (BVB Capital) വിദഗ്ധർ നിങ്ങളെ സഹായിക്കും.

ഉപസംഹാരം

പ്രിയപ്പെട്ടവരേ, റിട്ടയർമെന്റ് എന്നത് ജീവിതം അവസാനിക്കുന്ന ഇടമല്ല, മറിച്ച് പുതിയൊരു തുടക്കമാണ്. കയ്യിലുള്ള സമ്പാദ്യം വെറുതെ ബാങ്കിൽ ഇട്ട് അതിന്റെ മൂല്യം കുറയാൻ അനുവദിക്കരുത്. ബുദ്ധിപരമായി പ്ലാൻ ചെയ്താൽ സമാധാനത്തോടെ, അന്തസ്സോടെ നമുക്ക് നമ്മുടെ ശിഷ്ടകാലം ആസ്വദിക്കാം. SWP എന്നത് വെറുമൊരു നിക്ഷേപമല്ല, അതൊരു സുരക്ഷിതബോധമാണ്.

നിങ്ങൾക്കും ഇത്തരമൊരു പ്ലാൻ തുടങ്ങണമെന്നുണ്ടെങ്കിൽ ഒരു നല്ല ഫിനാൻഷ്യൽ അഡ്വൈസറെ കണ്ട് സംസാരിക്കുക. ഈ ലേഖനം നിങ്ങൾക്ക് ഉപകാരപ്പെട്ടെങ്കിൽ നിങ്ങളുടെ സുഹൃത്തുക്കൾക്കും കൂടി ഷെയർ ചെയ്യൂ. സംശയങ്ങൾ ഉണ്ടെങ്കിൽ താഴെ കമന്റ് ബോക്സിൽ ചോദിക്കാൻ മടിക്കണ്ട കേട്ടോ!

സമാധാനപരമായ ഒരു ഭാവിക്ക് വേണ്ടി ഇന്നുതന്നെ പ്ലാൻ ചെയ്യൂ!

പതിവായി ചോദിക്കുന്ന ചോദ്യങ്ങൾ (FAQ)

1. SWP തുടങ്ങാൻ വലിയ തുക വേണോ?

അങ്ങനെയൊന്നുമില്ല. മ്യൂച്വൽ ഫണ്ട് കമ്പനികൾ അനുവദിക്കുന്ന കുറഞ്ഞ തുക ഉണ്ടെങ്കിൽ നിങ്ങൾക്ക് ഇത് തുടങ്ങാം. എങ്കിലും ഒരു മാസവരുമാനം പ്രതീക്ഷിക്കുമ്പോൾ അത്യാവശ്യം നല്ലൊരു തുക നിക്ഷേപിക്കുന്നത് നന്നായിരിക്കും.

2. ഇത് സുരക്ഷിതമാണോ? പണം നഷ്ടപ്പെടുമോ?

മ്യൂച്വൽ ഫണ്ട് നിക്ഷേപങ്ങൾ വിപണിയിലെ കയറ്റിറക്കങ്ങൾക്ക് വിധേയമാണ്. അതുകൊണ്ട് തന്നെ ബാങ്ക് എഫ്.ഡി പോലെ നൂറ് ശതമാനം ഗ്യാരണ്ടി പറയാൻ കഴിയില്ല. പക്ഷേ, നല്ല ഫണ്ടുകൾ തിരഞ്ഞെടുക്കുകയും ദീർഘകാലത്തേക്ക് നിക്ഷേപിക്കുകയും ചെയ്താൽ വലിയ പേടി വേണ്ട.

3. എത്ര രൂപ മാസം പിൻവലിക്കാൻ സാധിക്കും?

നിങ്ങളുടെ ആവശ്യാനുസരണം എത്ര തുക വേണമെങ്കിലും പിൻവലിക്കാം. എങ്കിലും നിക്ഷേപിച്ച തുക തീർന്നുപോകാതിരിക്കാൻ ലാഭത്തിന്റെ ഒരു നിശ്ചിത ശതമാനം മാത്രം പിൻവലിക്കുന്നതാണ് വിദഗ്ദ്ധർ നൽകുന്ന ഉപദേശം.

4. ടാക്സ് എങ്ങനെയാണ് ഈടാക്കുന്നത്?

നിങ്ങൾ പിൻവലിക്കുന്ന ഓരോ തുകയും ‘യൂണിറ്റുകൾ’ വിൽക്കുന്നതിന് തുല്യമാണ്. അതിൽ വരുന്ന ലാഭത്തിന് (Capital Gains Tax) മാത്രമേ നിങ്ങൾ നികുതി നൽകേണ്ടി വരികയുള്ളൂ. ഇത് പലപ്പോഴും ബാങ്ക് പലിശയെക്കാൾ വളരെ കുറവായിരിക്കും.

5. എപ്പോഴാണ് ഇത് തുടങ്ങാൻ പറ്റിയ സമയം?

ജോലിയിൽ നിന്ന് വിരമിക്കുന്നതിന് തൊട്ടുമുൻപോ അല്ലെങ്കിൽ കയ്യിൽ ഒരു വലിയ തുക വരികയും അതിൽ നിന്ന് മാസം തോറും വരുമാനം വേണമെന്ന് ആഗ്രഹിക്കുമ്പോഴോ ഇത് തുടങ്ങാം.

കൂടുതൽ വിവരങ്ങൾക്കും നിങ്ങളുടെ റിട്ടയർമെന്റ് പ്ലാൻ തയ്യാറാക്കുന്നതിനും BVB Capital-ലെ വിദഗ്ധരുമായി ബന്ധപ്പെടാവുന്നതാണ്.

AMFI മാർഗ്ഗനിർദ്ദേശപ്രകാരമുള്ള അറിയിപ്പ്:മ്യൂച്വൽ ഫണ്ട് നിക്ഷേപങ്ങൾ വിപണിയിലെ അപകടസാധ്യതകൾക്ക് വിധേയമാണ്. നിക്ഷേപിക്കുന്നതിന് മുൻപ് സ്കീമുമായി ബന്ധപ്പെട്ട എല്ലാ രേഖകളും ശ്രദ്ധാപൂർവ്വം വായിക്കുക. കഴിഞ്ഞകാല പ്രകടനം ഭാവിയിൽ ആവർത്തിക്കണമെന്നില്ല.

Retirement is not just about stopping work. It is about starting a new phase of life with peace of mind. The biggest question most people face after retirement is:

“How will I get a regular monthly income?”

Earlier, people depended only on bank interest or rental income. But today interest rates are falling, and fixed deposits alone may not be enough to meet monthly expenses. This is where SWP – Systematic Withdrawal Plan from mutual funds becomes a powerful solution.

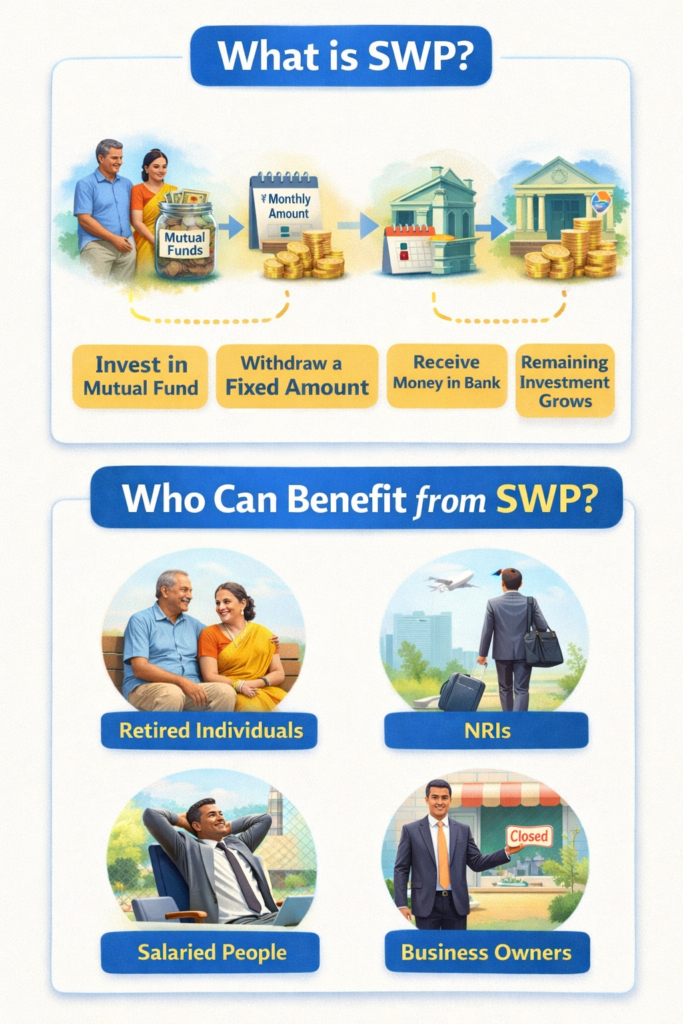

What is SWP?

SWP is a facility in mutual funds that allows you to withdraw a fixed amount every month from your investment.

It works like this:

You invest a lump sum in a mutual fund

You decide how much money you want every month

The amount is credited to your bank account regularly

The remaining money stays invested and continues to grow

So, SWP is like creating your own salary after retirement.

Who Can Benefit from SWP?

1. Retired Individuals

After retirement, regular expenses continue – medical bills, household needs, travel, and lifestyle expenses. Instead of keeping all money in low-interest deposits, SWP can provide:

Better returns than traditional savings

Regular monthly cash flow

Tax-efficient income

Flexibility to change withdrawal amount

2. NRIs Planning to Return to India

Many NRIs save money abroad and plan to settle in India later. They worry about:

How to manage income after returning

Where to park their hard-earned savings

How to get monthly income in Indian bank accounts

SWP is an excellent option because:

Money stays invested in India

Monthly income can be received just like salary

No need to depend on children or relatives

Easy to manage from anywhere in the world

3. Salaried People Preparing for Early Retirement

If you are in your 40s or 50s and dreaming of early retirement, SWP can help you plan in advance.

Let us help you convert your lifetime savings into a peaceful monthly income.

Frequently Asked Questions About SWP

1. What is SWP in mutual funds? SWP (Systematic Withdrawal Plan) is a facility that allows investors to withdraw a fixed amount from their mutual fund investment at regular intervals like monthly, quarterly, or yearly. It works like a salary after retirement.

2. Is SWP suitable for retired people? Yes. SWP is one of the best options for retired individuals who need regular monthly income while keeping their savings invested for growth.

3. Can NRIs use SWP in India? Absolutely. NRIs can invest in mutual funds in India and set up SWP to receive monthly income directly into their NRE/NRO bank accounts.

4. How is SWP better than Fixed Deposit? Unlike fixed deposits, SWP allows the remaining amount to stay invested and grow. It is also more tax-efficient and flexible compared to bank interest.

5. Will my money finish if I start SWP? Not necessarily. If withdrawals are planned properly and the fund earns reasonable returns, your capital can last for many years and may even grow.

6. Can I change the SWP amount later? Yes. You can increase, decrease, pause, or stop SWP anytime as per your financial needs.

7. Is SWP safe? SWP is linked to mutual funds, so returns depend on market performance. Choosing the right funds and proper planning makes it a safe and effective income strategy.

8. How much should I withdraw every month? The withdrawal amount should be decided based on your expenses, age, inflation, and investment value. A financial advisor can help plan this correctly.

9. What is the tax on SWP withdrawals? Tax depends on the type of mutual fund and holding period. Generally, SWP is more tax-efficient than FD interest.

10. How can BVB Capital help in SWP planning? BVB Capital Private Limited helps you choose suitable funds, decide the right withdrawal amount, and manage SWP so that you enjoy stress-free monthly income.

Plan Your Retirement Income with Experts

For personalized SWP planning for retirees, NRIs, salaried professionals, and business owners, contact:

Future Potential of the Indian Stock Market – Explained in Simple Words

Have you ever visited a vegetable market?

People go there to buy and sell vegetables. Some sell potatoes, some buy tomatoes, and some just watch the prices. The stock market works in a very similar way — but instead of vegetables, people buy and sell shares of companies.

Let’s understand this in an easy way.

What is a Stock Market?

A stock market is a place where people buy and sell shares of companies.

A share means a tiny piece of ownership in a company.

For example, if you buy one share of a big company like Reliance Industries, you become a very small owner of that company. If the company grows and earns profit, your share value may increase. If the company performs poorly, the share price can fall.

So in very simple words:

Stock Market = A place where people buy and sell small ownership pieces of companies.

A Simple Story to Understand

Imagine three friends — Arun, Meera, and Rahul — who want to start a juice shop.

They need ₹1,00,000 but only have ₹50,000. So they ask friends and relatives to invest the remaining money. In return, they promise to give them a small ownership in the shop.

Now:

Arun owns 50%

Meera owns 25%

Rahul owns 25%

If the juice shop becomes popular and earns profit, everyone benefits. If the shop fails, everyone shares the loss.

This is exactly how companies raise money in the stock market — by selling shares to the public.

Why Do People Invest in the Stock Market?

People invest because they want their money to grow faster than keeping it in a normal savings account.

Some common reasons are:

Long-term wealth creation

Retirement planning

Education goals

Buying a house or car

Owning part of big companies

But remember — stock markets always have ups and downs. Prices change daily. This is normal and part of investing.

How Does the Indian Stock Market Work?

In India, most buying and selling of shares happens through two big exchanges:

These exchanges act like large digital marketplaces where companies list their shares and investors trade safely with proper rules.

Future Potential of the Indian Stock Market

Many experts believe India has strong long-term growth potential. Here’s why:

1. Young Population

India has a large number of young people entering jobs and businesses. More income means more investments.

2. Digital Growth

Online apps, UPI payments, and mobile banking have made investing easier even from small towns and villages.

3. Growing Industries

Technology, renewable energy, healthcare, and manufacturing sectors are expanding rapidly.

4. Infrastructure Development

New roads, railways, airports, and smart cities help businesses grow.

5. Financial Awareness

More people are learning about money, savings, and investing from a young age.

Another Small Story About Growth

Think of a small village that slowly becomes a town and then a city. New schools open, shops increase, roads improve, and jobs grow. Property values rise and businesses expand.

The Indian stock market is similar. As the country develops, many good companies grow along with it. When companies grow, their share values can also grow over time — especially for patient investors.

Important Lesson for Beginners

If you are young or just starting to learn:

Learn first, invest later

Start small

Think long term

Avoid “get rich quick” schemes

Be patient and disciplined

Stock market investing is not gambling when done with knowledge and planning. It is a way of participating in the country’s growth journey.

How Mutual Funds Help You Enter the Stock Market

Not everyone needs to buy shares directly. A very simple and safer way to enter the stock market is through Mutual Funds.

Two popular methods are:

Lumpsum Investment – Investing a bigger amount one time.

Mutual funds collect money from many investors and invest in different companies. This provides diversification, meaning your money is spread across many stocks instead of depending on just one company. This can reduce risk compared to investing in a single share.

So even if you are a beginner, mutual funds allow you to participate in the Indian stock market in a structured and guided way.

Why Guidance Matters

Just like you would ask a teacher to learn mathematics or a coach to learn sports, it is always wise to take guidance while investing money.

For mutual fund investing, approaching a trusted and knowledgeable distributor can make a big difference. They help you:

Understand your financial goals

Choose suitable funds

Invest regularly with discipline

Avoid emotional decisions

Plan for long-term wealth

For those looking for professional support, approaching a mutual fund distributor like BVB Capital Private Limited can be a smart step. Proper guidance can help beginners enter the stock market confidently through SIP or lumpsum investments.

Conclusion

The stock market may look complicated at first, just like a crowded marketplace. But once you understand the basics, it becomes a powerful tool for building wealth over time.

You don’t always need to pick individual shares. Investing through mutual funds using SIP or lumpsum is a simple gateway into the Indian stock market. With the right guidance and patience, even small regular investments today can grow into meaningful financial strength tomorrow.

Start early, stay informed, and take expert guidance — the future opportunities in the Indian stock market are bright for those who prepare wisely.

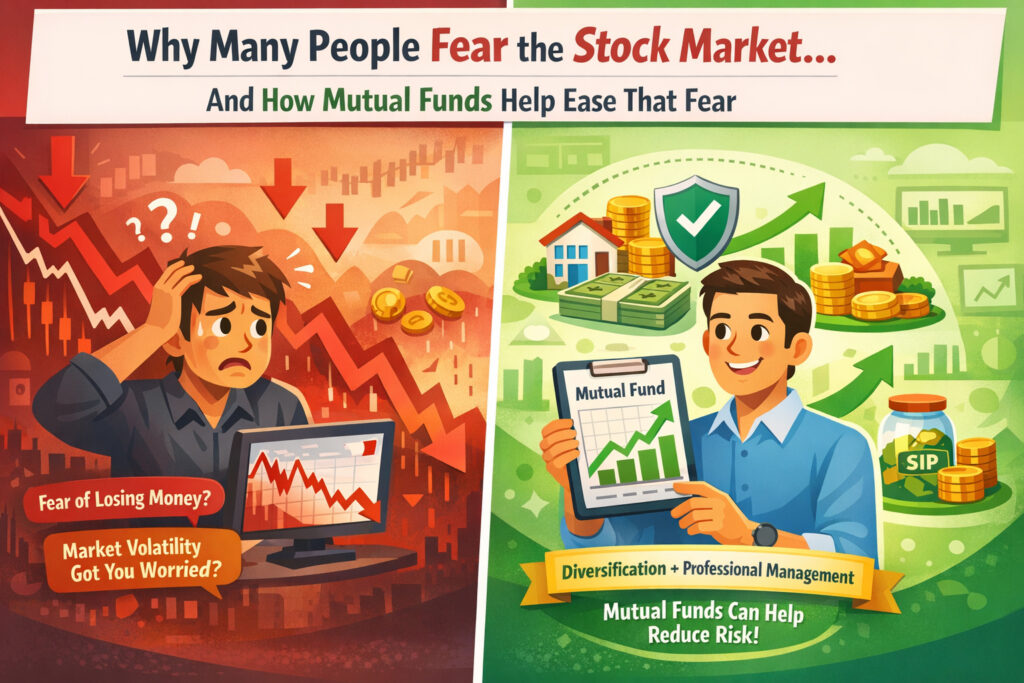

ഷെയർ മാർക്കറ്റ് എന്ന് കേൾക്കുമ്പോൾ തന്നെ നമ്മുടെ ഉള്ളിൽ ഒരു ചെറിയ മിന്നൽ അടിക്കാറുണ്ടോ? “അയ്യോ, അതൊക്കെ വലിയ റിസ്കല്ലേ?”, “പൈസ മുഴുവൻ പോയാലോ?” എന്നൊക്കെ ചിന്തിച്ച് മാറി നിൽക്കുന്നവരാണ് നമ്മളിൽ പലരും. രാവിലെ ഒരു കട്ടൻ ചായയും കുടിച്ച് പത്രം വായിക്കുമ്പോൾ ഷെയർ മാർക്കറ്റ് ഇടിഞ്ഞു എന്ന വാർത്ത കാണുമ്പോൾ, “നമ്മുടെ ഉള്ള കാശ് ഇങ്ങനെ കളയാനില്ല” എന്ന് പറഞ്ഞ് ആ പേജ് മറിച്ചു കളയുന്ന മലയാളിയുടെ ശീലം നമുക്ക് മാറ്റിയെടുക്കാം.

സത്യത്തിൽ, ഈ പേടി വെറുതെയല്ല. പക്ഷേ, ഈ പേടിയെ മാറ്റി നിർത്തി എങ്ങനെ നമ്മുടെ സമ്പാദ്യം വളർത്താം? അവിടെയാണ് ‘മ്യൂച്വൽ ഫണ്ടുകൾ‘ (Mutual Funds) ഒരു ഹീറോയെപ്പോലെ വരുന്നത്. നമുക്ക് ഈ വിഷയത്തെക്കുറിച്ച് വളരെ ലളിതമായി, ഒരു അയൽവാസിയോട് സംസാരിക്കുന്നതുപോലെ ഒന്ന് ചർച്ച ചെയ്താലോ?

പണം സുരക്ഷിതമായി വളർത്താൻ മ്യൂച്വൽ ഫണ്ടുകൾ നിങ്ങളെ എങ്ങനെ സഹായിക്കും എന്ന് വായിക്കാം!

നമുക്ക് കുറച്ച് സീരിയസ്സായ, എന്നാൽ എല്ലാവർക്കും ഉപകാരപ്പെടുന്ന ഒരു കാര്യം സംസാരിക്കാം. നമ്മൾ മലയാളികൾക്ക് പൊതുവെ രണ്ട് തരം നിക്ഷേപങ്ങളോടാണ് പ്രിയം—ഒന്ന് സ്വർണം, രണ്ട് ബാങ്കിലെ ഫിക്സഡ് ഡെപ്പോസിറ്റ് (FD). എന്നാൽ കാലം മാറുകയാണ്. പണപ്പെരുപ്പം (Inflation) കൂടുന്നതനുസരിച്ച് നമ്മുടെ സമ്പാദ്യവും വളരേണ്ടതുണ്ട്. ഷെയർ മാർക്കറ്റ് എന്ന് കേൾക്കുമ്പോൾ പേടി തോന്നുന്നവർക്കായി, ആ പേടി മാറ്റി എങ്ങനെ ബുദ്ധിപരമായി നിക്ഷേപം തുടങ്ങാം എന്നാണ് ഇന്ന് നമ്മൾ നോക്കുന്നത്.

എന്തിനാണ് നമുക്ക് ഷെയർ മാർക്കറ്റിനെ ഇത്ര പേടി?

നമ്മുടെ വീട്ടിലെ കുട്ടികളുടെ സ്കൂൾ ബാഗ് ശ്രദ്ധിച്ചിട്ടുണ്ടോ? അതിൽ ഒരുപാട് പുസ്തകങ്ങൾ ഉണ്ടാകും. അത് ഒറ്റയ്ക്ക് തൂക്കി നോക്കിയാൽ നല്ല ഭാരമാണ്. അതുപോലെയാണ് ഷെയർ മാർക്കറ്റും. നേരിട്ട് ഇറങ്ങിത്തിരിച്ചാൽ കാര്യങ്ങൾ പഠിക്കാനും റിസ്ക് എടുക്കാനും വലിയ ഭാരമായി തോന്നും. പ്രധാനമായും മൂന്ന് കാരണങ്ങൾ കൊണ്ടാണ് നമ്മൾ പേടിക്കുന്നത്:

പണം നഷ്ടപ്പെടുമോ എന്ന പേടി (Volatility): ലാഭം കിട്ടുന്ന ഷെയർ നാളെ ഇടിയുമോ എന്ന ടെൻഷൻ. ഒരു ഓണം ഷോപ്പിംഗിന് പോകുമ്പോൾ ഉള്ള തിരക്കുപോലെയാണ് മാർക്കറ്റ്; എപ്പോൾ എങ്ങോട്ട് തിരിയുമെന്ന് പറയാനാവില്ല.

വിവരമില്ലായ്മ (Lack of Knowledge): ഏത് കമ്പനിയുടെ ഷെയർ വാങ്ങണം? എപ്പോൾ വിൽക്കണം? ബാലൻസ് ഷീറ്റ് എങ്ങനെ വായിക്കും? ഇതൊന്നും സാധാരണക്കാരായ നമുക്ക് അറിയില്ലായിരിക്കും.

പഴയ കഥകൾ: പണ്ട് ആരോ ഷെയർ മാർക്കറ്റിൽ ഇട്ട് പണം കളഞ്ഞ കഥയോ അല്ലെങ്കിൽ വലിയ തട്ടിപ്പുകളെക്കുറിച്ചുള്ള വാർത്തകളോ കേട്ടാൽ പിന്നെ നമ്മൾ അങ്ങോട്ട് നോക്കില്ല.

ഈ പേടികളെല്ലാം മാറ്റാൻ സഹായിക്കുന്ന ഒന്നാണ് മ്യൂച്വൽ ഫണ്ടുകൾ.

മ്യൂച്വൽ ഫണ്ടുകൾ എങ്ങനെയാണ് ഈ പേടി മാറ്റുന്നത്?

മ്യൂച്വൽ ഫണ്ട് എന്ന് പറയുന്നത് ഒരു ടൂറിസ്റ്റ് ബസ് പോലെയാണ്. നമ്മൾ ഒരു സ്ഥലത്തേക്ക് കാറോടിച്ചു പോകുമ്പോൾ ഉള്ള ടെൻഷൻ ആലോചിച്ചു നോക്കൂ—വഴി അറിയണം, ട്രാഫിക് നോക്കണം, വണ്ടി കേടായാൽ നന്നാക്കണം. എന്നാൽ ബസ്സിൽ ആണെങ്കിലോ? ഒരു മിടുക്കനായ ഡ്രൈവർ ഉണ്ടാകും. നമ്മൾ ടിക്കറ്റ് എടുത്ത് ഇരുന്നാൽ മതി, ഡ്രൈവർ നമ്മളെ ലക്ഷ്യസ്ഥാനത്ത് എത്തിക്കും.

മ്യൂച്വൽ ഫണ്ടിലും ഇതുതന്നെയാണ് സംഭവിക്കുന്നത്.

വിദഗ്ധരുടെ സേവനം (Professional Management): നമുക്ക് മാർക്കറ്റിനെക്കുറിച്ച് അറിയില്ലെങ്കിലും സാരമില്ല. സാമ്പത്തിക കാര്യങ്ങളിൽ വലിയ അറിവുള്ള ‘ഫണ്ട് മാനേജർമാർ’ ആണ് നമ്മുടെ പണം എവിടെ നിക്ഷേപിക്കണം എന്ന് തീരുമാനിക്കുന്നത്.

റിസ്ക് കുറയ്ക്കുന്നു (Diversification): “എല്ലാ മുട്ടകളും ഒരു കൊട്ടയിൽ വെക്കരുത്” എന്ന് പറയാറില്ലേ? മ്യൂച്വൽ ഫണ്ടുകൾ നമ്മുടെ പണം ഒരു കമ്പനിയിലല്ല, മറിച്ച് പല പല കമ്പനികളിലായി നിക്ഷേപിക്കുന്നു. ഒരു കമ്പനി നഷ്ടത്തിലായാലും മറ്റുള്ളവ ലാഭത്തിലാകുന്നത് വഴി നമ്മുടെ പണം സുരക്ഷിതമായിരിക്കും.

ചെറിയ തുക കൊണ്ട് തുടങ്ങാം (SIP): ആയിരങ്ങളും ലക്ഷങ്ങളും വേണമെന്നില്ല. വെറും 500 രൂപ കൊണ്ട് നിങ്ങൾക്ക് നിക്ഷേപം തുടങ്ങാം. ഇതിനെയാണ് SIP (Systematic Investment Plan) എന്ന് വിളിക്കുന്നത്. കുട്ടികൾ കുടുക്കയിൽ പണം ഇട്ടു വെക്കുന്നതുപോലെ മാസമാസം നമുക്ക് നിക്ഷേപിക്കാം.

നേരിട്ടുള്ള ഓഹരി നിക്ഷേപവും മ്യൂച്വൽ ഫണ്ടും തമ്മിലുള്ള വ്യത്യാസം

നിങ്ങൾക്ക് കാര്യങ്ങൾ എളുപ്പത്തിൽ മനസ്സിലാക്കാൻ താഴെ പറയുന്ന പട്ടിക ഒന്ന് നോക്കൂ:

സവിശേഷത

നേരിട്ടുള്ള ഷെയർ നിക്ഷേപം

മ്യൂച്വൽ ഫണ്ട്

അറിവ്

നല്ല അറിവും സമയവും വേണം

പ്രത്യേക അറിവ് നിർബന്ധമില്ല

റിസ്ക്

വളരെ കൂടുതൽ

കുറവായിരിക്കും (താരതമ്യേന)

സമയ ലാഭം

എന്നും മാർക്കറ്റ് ശ്രദ്ധിക്കണം

ഫണ്ട് മാനേജർ നോക്കിക്കൊള്ളും

നിക്ഷേപ തുക

നല്ലൊരു തുക തുടക്കത്തിൽ വേണം

500 രൂപ മുതൽ തുടങ്ങാം

നിക്ഷേപം തുടങ്ങാൻ 4 ലളിതമായ ഘട്ടങ്ങൾ

മ്യൂച്വൽ ഫണ്ടിലേക്ക് ആദ്യമായി ചുവടുവെക്കുന്നവർക്ക് ഈ വഴി പിന്തുടരാം:

നിങ്ങളുടെ ലക്ഷ്യം തീരുമാനിക്കുക: മകളുടെ കല്യാണത്തിനാണോ, വീട് പണിക്കാണോ, അതോ വിരമിച്ച ശേഷമുള്ള ജീവിതത്തിനാണോ നിങ്ങൾ പണം മാറ്റിവെക്കുന്നത് എന്ന് ആദ്യം ചിന്തിക്കുക.

ശരിയായ ഫണ്ട് തിരഞ്ഞെടുക്കുക: റിസ്ക് എടുക്കാൻ മടിയുള്ളവർക്ക് ഡെബ്റ്റ് ഫണ്ടുകളും (Debt Funds), കൂടുതൽ ലാഭം ആഗ്രഹിക്കുന്നവർക്ക് ഇക്വിറ്റി ഫണ്ടുകളും (Equity Funds) തിരഞ്ഞെടുക്കാം.

കെ.വൈ.സി (KYC) പൂർത്തിയാക്കുക: ആധാർ കാർഡും പാൻ കാർഡും ഉപയോഗിച്ച് എളുപ്പത്തിൽ ഇത് ചെയ്യാം.

SIP തുടങ്ങുക: എല്ലാ മാസവും കൃത്യമായ ഒരു തുക നിക്ഷേപിക്കാൻ ബാങ്കിൽ നിന്ന് ഓട്ടോമാറ്റിക് ആയി മാറുന്ന രീതി ക്രമീകരിക്കാം.

ഇതുമായി ബന്ധപ്പെട്ട് ചില കാര്യങ്ങൾ കൂടി…

നമ്മൾ ഒരു തൈ നടുന്നത് പോലെയാണ് നിക്ഷേപം. ഇന്ന് നട്ടാൽ നാളെ തന്നെ ഫലം കിട്ടില്ല. അതിന് വെള്ളമൊഴിച്ച്, വളമിട്ട് കാത്തിരിക്കണം. അതുപോലെ മാർക്കറ്റിൽ ചെറിയ ഇടിവുകൾ ഉണ്ടാകുമ്പോൾ പേടിച്ച് പണം പിൻവലിക്കരുത്. ദീർഘകാലത്തേക്ക് (Long term) നിക്ഷേപിച്ചാൽ മാത്രമേ പണം നല്ല രീതിയിൽ വളരുകയുള്ളൂ.

ഉപസംഹാരം

ഷെയർ മാർക്കറ്റ് എന്നത് ഭാഗ്യപരീക്ഷണമല്ല, മറിച്ച് കൃത്യമായ പ്ലാനിംഗിലൂടെ പണം വളർത്താനുള്ള ഒരു വഴിയാണ്. പേടി കൊണ്ട് മാത്രം ആ വഴി ഉപേക്ഷിക്കരുത്. മ്യൂച്വൽ ഫണ്ടുകൾ നിങ്ങളുടെ പേടി മാറ്റാനും പണം സുരക്ഷിതമായി വളർത്താനും സഹായിക്കും. ഓർക്കുക, ഇന്ന് നിങ്ങൾ മാറ്റിവെക്കുന്ന ഓരോ രൂപയും നിങ്ങളുടെ ഭാവി സുരക്ഷിതമാക്കാൻ സഹായിക്കും. അപ്പോൾ ഇന്ന് തന്നെ ഒരു SIP തുടങ്ങിയാലോ?

പതിവായി ചോദിക്കുന്ന ചോദ്യങ്ങൾ (FAQ)

1. മ്യൂച്വൽ ഫണ്ടിൽ പണം നഷ്ടപ്പെടാൻ സാധ്യതയുണ്ടോ?

മ്യൂച്വൽ ഫണ്ടുകൾ മാർക്കറ്റ് റിസ്കുകൾക്ക് വിധേയമാണ്. എന്നാൽ ദീർഘകാലത്തേക്ക് നിക്ഷേപിക്കുമ്പോൾ ഈ റിസ്ക് വളരെ കുറയുകയും നല്ല ലാഭം ലഭിക്കാനുള്ള സാധ്യത കൂടുകയും ചെയ്യുന്നു.

2. എത്ര രൂപ മുതൽ എനിക്ക് നിക്ഷേപം തുടങ്ങാം?

മിക്ക മ്യൂച്വൽ ഫണ്ടുകളിലും വെറും 500 രൂപ മുതൽ SIP ആയി നിക്ഷേപം തുടങ്ങാവുന്നതാണ്.

3. പണം എപ്പോൾ വേണമെങ്കിലും പിൻവലിക്കാമോ?

അതെ, മിക്ക സ്കീമുകളിലും നിങ്ങൾക്ക് എപ്പോൾ വേണമെങ്കിലും പണം പിൻവലിക്കാം (ലിക്വിഡ് ഫണ്ടുകൾ ഇതിന് മികച്ചതാണ്). എന്നാൽ ചില ടാക്സ് സേവിംഗ് ഫണ്ടുകൾക്ക് (ELSS) മൂന്ന് വർഷത്തെ ലോക്കിൻ പിരിയഡ് ഉണ്ടാകും.

4. മ്യൂച്വൽ ഫണ്ടുകൾ സുരക്ഷിതമാണോ?

ഇന്ത്യയിലെ മ്യൂച്വൽ ഫണ്ടുകളെല്ലാം സെബി (SEBI – Securities and Exchange Board of India) എന്ന സർക്കാർ ഏജൻസിയുടെ കർശനമായ നിയന്ത്രണത്തിലാണ്. അതുകൊണ്ട് നിങ്ങളുടെ പണം തട്ടിക്കൊണ്ടുപോകാൻ ആർക്കും എളുപ്പമല്ല.

5. എനിക്ക് ബാങ്ക് അക്കൗണ്ട് വേണോ?

അതെ, മ്യൂച്വൽ ഫണ്ടിൽ നിക്ഷേപിക്കാനും തിരികെ പണം വാങ്ങാനും ഒരു ബാങ്ക് അക്കൗണ്ട് നിർബന്ധമാണ്.

ഈ പോസ്റ്റ് നിങ്ങൾക്ക് ഉപകാരപ്പെട്ടോ? നിങ്ങളുടെ സംശയങ്ങൾ താഴെ കമന്റ് ചെയ്യൂ. നിങ്ങളുടെ കൂട്ടുകാർക്കും ഇത് ഷെയർ ചെയ്യാൻ മറക്കരുത്!

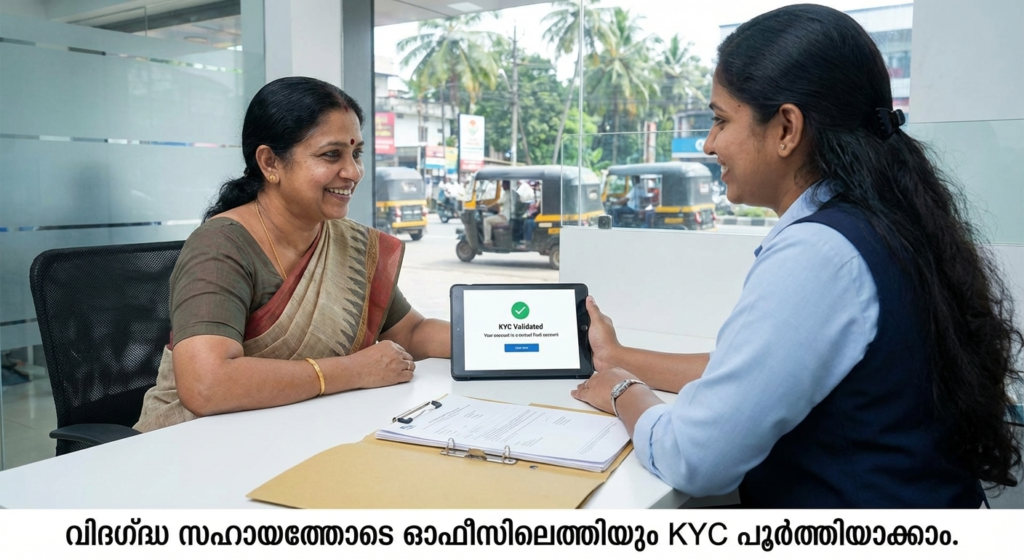

സന്ധ്യക്ക് ഒരു ചായയും കുടിച്ച് സിറ്റൗട്ടിൽ ഇരിക്കുമ്പോഴാണ് പലപ്പോഴും നമ്മൾ നിക്ഷേപങ്ങളെ കുറിച്ചും ഭാവിയിലെ സമ്പാദ്യത്തെ കുറിച്ചുമൊക്കെ ചിന്തിക്കാറുള്ളത്, അല്ലേ? പ്രത്യേകിച്ച് ഈ ഓണം ബോണസ് കിട്ടുമ്പോഴോ അല്ലെങ്കിൽ മക്കളുടെ സ്കൂൾ ബാഗും കുടയുമൊക്കെ വാങ്ങാൻ പണം തികയാതെ വരുമ്പോഴോ ഒക്കെയാകും “ഒരു നിക്ഷേപം തുടങ്ങാമായിരുന്നു” എന്ന് നമ്മൾ ആലോചിക്കുക.

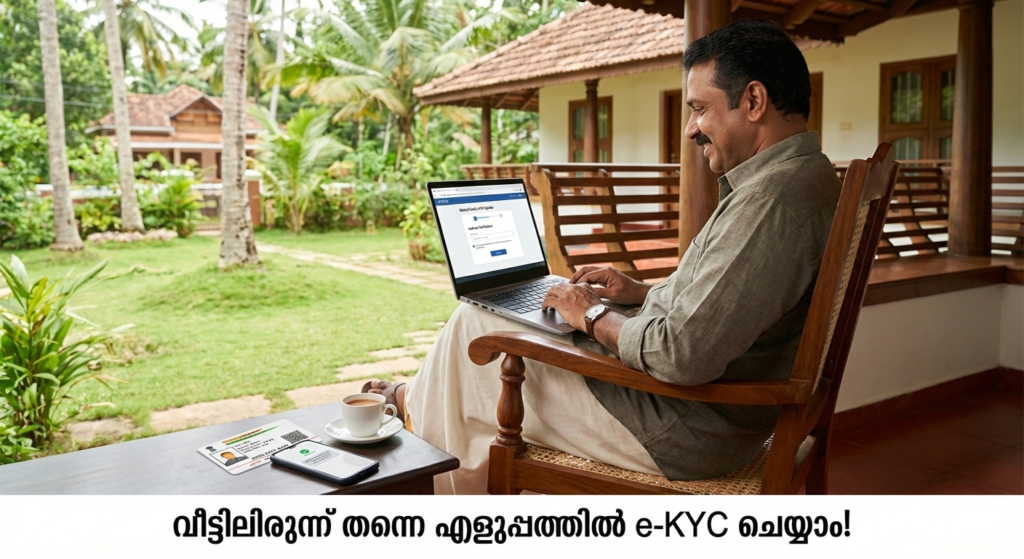

അങ്ങനെ കഷ്ടപ്പെട്ട് കുറച്ച് പണം മ്യൂച്വൽ ഫണ്ടിൽ നിക്ഷേപിക്കാൻ തീരുമാനിച്ചു എന്ന് വിചാരിക്കുക. പക്ഷേ, പെട്ടെന്ന് ഒരാൾ വന്ന് ചോദിക്കുന്നു, “നിങ്ങളുടെ കെ.വൈ.സി (KYC) ഓക്കെയാണോ?” എന്ന്. അപ്പോൾ നമ്മൾ ഒന്ന് അമ്പരക്കും. ഇതെന്ത് സാധനമാണെന്ന് പലരും ചോദിക്കാറുണ്ട്. പേടിക്കേണ്ട, നമ്മുടെ നാട്ടിലെ ബാങ്കിൽ അക്കൗണ്ട് തുടങ്ങുന്നതുപോലെ ലളിതമായ ഒരു കാര്യമാണിത്. ഇന്ന് നമ്മൾ സംസാരിക്കാൻ പോകുന്നത് മ്യൂച്വൽ ഫണ്ട് നിക്ഷേപകർ അറിഞ്ഞിരിക്കേണ്ട കെ.വൈ.സി വിശേഷങ്ങളെ കുറിച്ചാണ്.

നമ്മൾ മലയാളികൾക്ക് എന്നും സമ്പാദ്യശീലം കുറച്ച് കൂടുതലാണ്. ചിട്ടിയും സ്വർണ്ണവും ഒക്കെ കഴിഞ്ഞാൽ ഇപ്പോൾ നമ്മുടെ ഇടയിൽ ട്രെൻഡ് ആയിക്കൊണ്ടിരിക്കുന്നത് മ്യൂച്വൽ ഫണ്ടുകളാണ്. എന്നാൽ നിക്ഷേപം തുടങ്ങുന്നതിന് മുൻപോ അല്ലെങ്കിൽ നിലവിലുള്ള നിക്ഷേപം സുഗമമായി മുന്നോട്ട് കൊണ്ടുപോകാനോ ഈ ‘കെ.വൈ.സി’ കൃത്യമായിരിക്കണം. ഇതിനെക്കുറിച്ച് ലളിതമായി താഴെ വിവരിക്കാം.

എന്താണ് ഈ കെ.വൈ.സി (KYC)?

ലളിതമായി പറഞ്ഞാൽ ‘നിങ്ങളുടെ ഇടപാടുകാരനെ അറിയുക’ (Know Your Customer) എന്നാണ് ഇതിന്റെ അർത്ഥം. നമ്മൾ സ്കൂളിൽ ചേരുമ്പോൾ ജനന സർട്ടിഫിക്കറ്റും ഫോട്ടോയും ഒക്കെ കൊടുക്കാറില്ലേ? അതുപോലെ തന്നെയാണ് ഇതും. നിങ്ങൾ ആരാണെന്നും എവിടെയാണ് താമസമെന്നും നിക്ഷേപിക്കുന്ന പണം നിയമപരമാണെന്നും ഉറപ്പുവരുത്താൻ സർക്കാർ ഏർപ്പെടുത്തിയ ഒരു സംവിധാനമാണിത്. കള്ളപ്പണം വെളുപ്പിക്കുന്നത് തടയാനും നിങ്ങളുടെ പണം സുരക്ഷിതമാണെന്ന് ഉറപ്പാക്കാനും ഇത് സഹായിക്കുന്നു.

കെ.വൈ.സി സ്റ്റാറ്റസുകൾ: നിങ്ങൾ എവിടെ നിൽക്കുന്നു?

നിങ്ങൾ ഇതിനോടകം നിക്ഷേപം തുടങ്ങിയ ആളാണെങ്കിൽ നിങ്ങളുടെ കെ.വൈ.സി സ്റ്റാറ്റസ് ഒന്ന് പരിശോധിക്കുന്നത് നല്ലതാണ്. സാധാരണയായി മൂന്ന് തരം സ്റ്റാറ്റസുകളാണ് ഉള്ളത്. അത് താഴെ പറയുന്നവയാണ്:

സ്റ്റാറ്റസ് (Status)

ഇതിന്റെ അർത്ഥം എന്താണ്?

നിങ്ങൾ എന്ത് ചെയ്യണം?

KYC Validated

എല്ലാം പെർഫെക്റ്റാണ്! ആധാർ കാർഡും പാൻ കാർഡും കൃത്യമായി ലിങ്ക് ചെയ്തിട്ടുണ്ട്.

നിങ്ങൾക്ക് പുതിയ നിക്ഷേപങ്ങൾ തുടങ്ങാം, പണം പിൻവലിക്കാം. പേടിക്കേണ്ടതില്ല.

KYC Registered

നിങ്ങളുടെ വിവരങ്ങൾ ഉണ്ട്, പക്ഷേ ആധാർ വഴി വീണ്ടും ഒന്ന് ഉറപ്പിക്കേണ്ടതുണ്ട്.

പഴയ നിക്ഷേപം തുടരാം, പക്ഷേ പുതിയ ഫണ്ടുകളിൽ നിക്ഷേപിക്കണമെങ്കിൽ വീണ്ടും വാലിഡേഷൻ വേണം.

KYC On-Hold

എന്തോ ഒരു പ്രശ്നമുണ്ട്. ഒന്നുകിൽ ഫോൺ നമ്പർ തെറ്റാണ് അല്ലെങ്കിൽ രേഖകൾ അപൂർണ്ണമാണ്.

ഉടനെ തന്നെ രേഖകൾ പുതുക്കണം. അല്ലെങ്കിൽ നിങ്ങളുടെ നിക്ഷേപം തടസ്സപ്പെടും.

നിക്ഷേപം തുടങ്ങാൻ എന്തൊക്കെ വേണം? (Checklist)

നമ്മൾ ഒരു യാത്ര പോകുമ്പോൾ ബാഗിൽ എടുക്കേണ്ട കാര്യങ്ങൾ മറക്കാറില്ലല്ലോ? അതുപോലെ മ്യൂച്വൽ ഫണ്ട് കെ.വൈ.സി ചെയ്യാൻ താഴെ പറയുന്ന കാര്യങ്ങൾ കയ്യിൽ കരുതുക:

പാൻ കാർഡ് (PAN Card): നിക്ഷേപങ്ങളുടെ കാര്യത്തിൽ ഇതാണ് നമ്മുടെ പ്രധാന തിരിച്ചറിയൽ രേഖ.

ആധാർ കാർഡ് (Aadhaar Card): വിലാസം തെളിയിക്കാനായി ഇത് അത്യാവശ്യമാണ്.

ഫോട്ടോ: നിങ്ങളുടെ ഒരു പാസ്പോർട്ട് സൈസ് ഫോട്ടോ.

ഫോൺ നമ്പറും ഇമെയിലും: ആധാറുമായി ലിങ്ക് ചെയ്ത ഫോൺ നമ്പർ തന്നെ നൽകാൻ ശ്രദ്ധിക്കുക.

ഡിജിറ്റൽ സിഗ്നേച്ചർ: ഓൺലൈനായി ചെയ്യുമ്പോൾ വെളുത്ത പേപ്പറിൽ ഒപ്പിട്ട് അത് സ്കാൻ ചെയ്ത് നൽകേണ്ടി വരും.

കെ.വൈ.സി അപ്ഡേറ്റ് ചെയ്യാനുള്ള എളുപ്പവഴികൾ

ഇതൊക്കെ ചെയ്യാൻ ഇനി ഓഫീസുകൾ കയറി ഇറങ്ങേണ്ട കാലം കഴിഞ്ഞു. വീട്ടിലിരുന്ന് ചായ കുടിച്ചു കൊണ്ട് തന്നെ നമുക്ക് ഇത് ചെയ്യാം.

ഓൺലൈൻ വഴി (e-KYC): ഏതെങ്കിലും മ്യൂച്വൽ ഫണ്ട് ഹൗസിന്റെ വെബ്സൈറ്റിലോ കെ.ആർ.എ (KRA – KYC Registration Agency) വെബ്സൈറ്റിലോ കയറി ആധാർ ഉപയോഗിച്ച് ഒടിപി (OTP) വഴി കെ.വൈ.സി പൂർത്തിയാക്കാം. നമ്മുടെ ഫോണിൽ മെസ്സേജ് വരുന്നത് നോക്കി ടൈപ്പ് ചെയ്താൽ മതി, സംഗതി സിമ്പിൾ!

ഓഫ്ലൈൻ വഴി: നിങ്ങൾക്ക് നേരിട്ട് പോകാനാണ് താൽപ്പര്യമെങ്കിൽ അപേക്ഷാ ഫോം പൂരിപ്പിച്ച് രേഖകളുടെ കോപ്പികൾ സഹിതം ഏതെങ്കിലും ഇൻവെസ്റ്റ്മെന്റ് സെന്ററിലോ മ്യൂച്വൽ ഫണ്ട് ഓഫീസിലോ നൽകാം.

എന്തുകൊണ്ട് ഇത് ഇപ്പോൾ ചെയ്യണം?

“പിന്നെ ചെയ്യാം” എന്ന് കരുതി മാറ്റി വെക്കുന്ന ശീലം നമുക്ക് പൊതുവെ ഉണ്ടല്ലോ. എന്നാൽ കെ.വൈ.സി കാര്യത്തിൽ അത് വലിയ പണിയാകും.

SIP മുടങ്ങും: നിങ്ങൾ മാസം തോറും ചെറിയ തുക നിക്ഷേപിക്കുന്ന ആളാണെങ്കിൽ (SIP), കെ.വൈ.സി പ്രശ്നമാണെങ്കിൽ ബാങ്കിൽ നിന്ന് പണം പോകുന്നത് നിൽക്കും.

പണം പിൻവലിക്കാൻ കഴിയില്ല: അത്യാവശ്യ ഘട്ടത്തിൽ മ്യൂച്വൽ ഫണ്ടിൽ നിന്ന് പണം എടുക്കാൻ നോക്കുമ്പോൾ കെ.വൈ.സി തടസ്സമായാൽ അത് വലിയ ബുദ്ധിമുട്ടാകും.

പുതിയ നിക്ഷേപം നടക്കില്ല: നല്ലൊരു അവസരം വരുമ്പോൾ പുതിയ ഫണ്ടുകളിൽ പണം ഇടാൻ നിങ്ങൾക്ക് കഴിയില്ല.

നമ്മുടെ സമ്പാദ്യം സുരക്ഷിതമായിരിക്കാൻ നിയമപരമായ ഇത്തരം കാര്യങ്ങൾ കൃത്യമായി പാലിക്കേണ്ടതുണ്ട്. സ്കൂൾ ബാഗ് അടുക്കി വെക്കുന്നതുപോലെ തന്നെ പ്രധാനമാണ് നമ്മുടെ നിക്ഷേപ രേഖകളും വൃത്തിയായി സൂക്ഷിക്കുന്നത്. കെ.വൈ.സി സ്റ്റാറ്റസ് ‘Validated’ ആണെന്ന് ഉറപ്പുവരുത്തിയാൽ നിങ്ങൾക്ക് സമാധാനമായി ഉറങ്ങാം.

ഇതുമായി ബന്ധപ്പെട്ട് നിങ്ങൾക്ക് എന്തെങ്കിലും സംശയങ്ങൾ ഉണ്ടെങ്കിൽ കമന്റ് ചെയ്യുകയോ അല്ലെങ്കിൽ നിങ്ങളുടെ സാമ്പത്തിക ഉപദേശകനോട് ചോദിക്കുകയോ ചെയ്യാം. നിക്ഷേപം തുടങ്ങാൻ ഇനിയും വൈകിക്കരുത്!

പതിവായി ചോദിക്കുന്ന ചോദ്യങ്ങൾ (FAQ)

1. ആധാർ ഇല്ലാതെ കെ.വൈ.സി ചെയ്യാൻ പറ്റുമോ?

പറ്റും, വോട്ടർ ഐഡിയോ പാസ്പോർട്ടോ ഒക്കെ ഉപയോഗിക്കാം. പക്ഷേ, ഇപ്പോൾ എല്ലാം ഡിജിറ്റൽ ആയതുകൊണ്ട് ആധാർ ഉപയോഗിക്കുന്നതാണ് ഏറ്റവും എളുപ്പവും വേഗമേറിയതും.

2. കെ.വൈ.സി ചെയ്യാൻ പണം നൽകണോ?

ഒരിക്കലുമില്ല! മ്യൂച്വൽ ഫണ്ട് കെ.വൈ.സി തികച്ചും സൗജന്യമാണ്. ഇതിനായി ആരെങ്കിലും പണം ചോദിച്ചാൽ കൊടുക്കരുത്.

3. പാൻ കാർഡും ആധാറും ലിങ്ക് ചെയ്യേണ്ടത് നിർബന്ധമാണോ?

അതെ, തീർച്ചയായും! ഇവ രണ്ടും ലിങ്ക് ചെയ്തിട്ടില്ലെങ്കിൽ നിങ്ങളുടെ പാൻ കാർഡ് അസാധുവാകാൻ സാധ്യതയുണ്ട്. അത് നിങ്ങളുടെ നിക്ഷേപത്തെ ബാധിക്കും.

4. എത്ര ദിവസം കൊണ്ട് കെ.വൈ.സി പൂർത്തിയാകും?

ഓൺലൈൻ വഴിയാണെങ്കിൽ സാധാരണ 3 മുതൽ 5 പ്രവൃത്തി ദിവസങ്ങൾക്കുള്ളിൽ സ്റ്റാറ്റസ് അപ്ഡേറ്റ് ആകും. ചിലപ്പോൾ അതിലും വേഗത്തിൽ നടന്നേക്കാം.

5. ഞാൻ നേരത്തെ കെ.വൈ.സി ചെയ്തതാണ്, ഇനി വീണ്ടും ചെയ്യണോ?

നിങ്ങളുടെ സ്റ്റാറ്റസ് ‘Validated’ ആണെങ്കിൽ വീണ്ടും ചെയ്യേണ്ടതില്ല. എന്നാൽ വിലാസമോ ഫോൺ നമ്പറോ മാറിയിട്ടുണ്ടെങ്കിൽ അത് അപ്ഡേറ്റ് ചെയ്യുന്നത് നല്ലതാണ്.

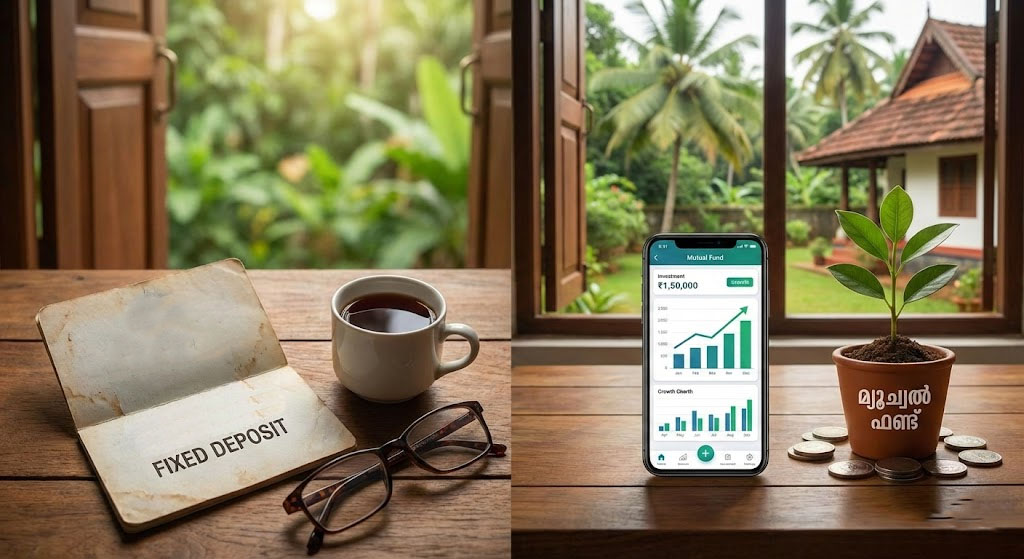

രാവിലെ ഒരു ചായയും കുടിച്ച് പത്രം വായിച്ചിരിക്കുമ്പോഴാണ് അടുത്ത വീട്ടിലെ ദാസേട്ടൻ വരുന്നത്. കയ്യിൽ ഒരു ചെറിയ തുകയുണ്ട്, അത് എവിടെയെങ്കിലും നിക്ഷേപിക്കണം. “മോനേ, ഇത് ബാങ്കിൽ എഫ്ഡി (FD) ഇട്ടാൽ മതിയോ അതോ ഈ പരസ്യത്തിൽ കാണുന്ന മ്യൂച്വൽ ഫണ്ടിൽ ഇടണോ?” എന്നായിരുന്നു പുള്ളിക്കാരന്റെ സംശയം. ഇത് ദാസേട്ടന്റെ മാത്രം സംശയമല്ല, നമ്മളിൽ പലരും എപ്പോഴും ആലോചിക്കുന്ന കാര്യമാണ്.

നമ്മൾ കഷ്ടപ്പെട്ട് ഉണ്ടാക്കിയ പണം വെറുതെ അലമാരയിൽ വെച്ചാൽ അത് വളരില്ലല്ലോ. അതുകൊണ്ട്, ശരിയായ വഴി തിരഞ്ഞെടുക്കാൻ നിങ്ങളെ സഹായിക്കുന്ന ഒരു കൊച്ചു ബ്ലോഗാണിത്. നമുക്ക് വളരെ ലളിതമായി, ഒരു ചായ കുടിക്കുന്ന നേരത്തിനുള്ളിൽ ഇത് മനസ്സിലാക്കാം.

കഷ്ടപ്പെട്ട് ഉണ്ടാക്കിയ പണം എവിടെ സൂക്ഷിക്കണം? ബാങ്ക് എഫ്ഡിയാണോ മ്യൂച്വൽ ഫണ്ടാണോ നിങ്ങൾക്ക് നല്ലത്? ദാ ഒരു സിമ്പിൾ മറുപടി!

നിങ്ങൾ എപ്പോഴെങ്കിലും ചിന്തിച്ചിട്ടുണ്ടോ, പത്ത് വർഷം മുമ്പ് ഒരു സ്കൂൾ ബാഗ് വാങ്ങാൻ എത്ര രൂപയായിരുന്നു എന്ന്? ഒരുപക്ഷേ 200 രൂപ. ഇന്ന് അതേ ബാഗിന് 800 രൂപയെങ്കിലും കൊടുക്കണം. ഇതിനെയാണ് നമ്മൾ ‘വിലക്കയറ്റം’ (Inflation) എന്ന് വിളിക്കുന്നത്. നമ്മുടെ പണം വളരുന്നത് ഈ വിലക്കയറ്റത്തേക്കാൾ വേഗത്തിലല്ലെങ്കിൽ, സത്യത്തിൽ നമ്മൾ ദരിദ്രരാവുകയാണ് ചെയ്യുന്നത്. ഇവിടെയാണ് എഫ്ഡിയും മ്യൂച്വൽ ഫണ്ടും തമ്മിലുള്ള യുദ്ധം തുടങ്ങുന്നത്!

എന്താണ് ഈ ബാങ്ക് എഫ്ഡി (Fixed Deposit)?

ബാങ്ക് എഫ്ഡി എന്ന് പറയുന്നത് നമ്മുടെ പഴയ കാലത്തെ പത്തായം പോലെയാണ്. സുരക്ഷിതമാണ്. ഒരു നിശ്ചിത തുക നമ്മൾ ഒരു നിശ്ചിത കാലത്തേക്ക് ബാങ്കിൽ ഏൽപ്പിക്കുന്നു. പകരം ബാങ്ക് നമുക്ക് ഒരു നിശ്ചിത ശതമാനം പലിശ തരുന്നു.

ഗുണങ്ങൾ:

പേടി വേണ്ട: ബാങ്ക് പൊളിഞ്ഞു പോകില്ല എന്ന വിശ്വാസമുള്ളതുകൊണ്ട് നമുക്ക് സമാധാനമായി ഉറങ്ങാം.

ഉറപ്പുള്ള ലാഭം: നിക്ഷേപിക്കുമ്പോൾ തന്നെ എത്ര രൂപ തിരിച്ചു കിട്ടും എന്ന് നമുക്കറിയാം.

ദോഷങ്ങൾ:

കുറഞ്ഞ ലാഭം: പലിശ നിരക്ക് പലപ്പോഴും കുറവായിരിക്കും. വിലക്കയറ്റത്തെ തോൽപ്പിക്കാൻ ഈ ലാഭം മിക്കപ്പോഴും തികയില്ല.

ടാക്സ്: കിട്ടുന്ന പലിശയ്ക്ക് നമ്മൾ നികുതി കൊടുക്കേണ്ടി വരും.

അപ്പോൾ എന്താണ് ഈ മ്യൂച്വൽ ഫണ്ട് (Mutual Fund)?

മ്യൂച്വൽ ഫണ്ട് എന്നത് ഒരു ഗ്രൂപ്പ് നിക്ഷേപം പോലെയാണ്. പലരിൽ നിന്നായി പണം ശേഖരിച്ച് ഒരു വിദഗ്ധൻ (Fund Manager) അത് ഓഹരി വിപണിയിലോ മറ്റ് മേഖലകളിലോ നിക്ഷേപിക്കുന്നു. ഇത് നമ്മുടെ പറമ്പിൽ ഒരു തെങ്ങ് നടുന്നത് പോലെയാണ്. നനച്ചു വളർത്തിയാൽ ഭാവിയിൽ നല്ല ആദായം കിട്ടും.

ഗുണങ്ങൾ:

കൂടുതൽ ലാഭം: ദീർഘകാലത്തേക്ക് നോക്കിയാൽ എഫ്ഡിയേക്കാൾ മികച്ച ലാഭം തരാൻ മ്യൂച്വൽ ഫണ്ടുകൾക്ക് സാധിക്കും.

ചെറിയ തുകയിൽ തുടങ്ങാം: ഓണം ഷോപ്പിംഗിന് മാറ്റിവെക്കുന്ന പണത്തിന്റെ ഒരു ഭാഗം, അതായത് 500 രൂപ ഉണ്ടെങ്കിൽ പോലും നിങ്ങൾക്ക് നിക്ഷേപം തുടങ്ങാം (ഇതിനെ SIP എന്ന് വിളിക്കുന്നു).

വിദഗ്ധരുടെ സേവനം: പണം എവിടെ നിക്ഷേപിക്കണം എന്ന് തല പുകയ്ക്കേണ്ടതില്ല, അത് നോക്കാൻ പ്രൊഫഷണലുകൾ ഉണ്ട്.

ദോഷങ്ങൾ:

റിസ്ക് ഉണ്ട്: വിപണിയിൽ മാറ്റങ്ങൾ വരുമ്പോൾ ലാഭത്തിലും ചെറിയ മാറ്റങ്ങൾ വരാം. പക്ഷേ ദീർഘകാലം കാത്തിരുന്നാൽ ഈ റിസ്ക് കുറയും.

എഫ്ഡിയും മ്യൂച്വൽ ഫണ്ടും: ഒരു ചെറിയ താരതമ്യം

നമുക്ക് ഇതൊരു പട്ടിക രൂപത്തിൽ നോക്കിയാലോ? കാര്യങ്ങൾ പെട്ടെന്ന് മനസ്സിലാകും.

കാര്യങ്ങൾ

ബാങ്ക് എഫ്ഡി (FD)

മ്യൂച്വൽ ഫണ്ട് (MF)

ലാഭം (Returns)

നിശ്ചിതം (സ്ഥിരമായ പലിശ)

വിപണിക്കനുസരിച്ച് മാറ്റം വരാം (സാധാരണ കൂടുതൽ ലാഭം)

റിസ്ക്

വളരെ കുറവ്

ഇടത്തരം മുതൽ കൂടുതൽ വരെ (സ്കീം അനുസരിച്ച്)

പണം പിൻവലിക്കൽ

കാലാവധിക്ക് മുമ്പ് പിൻവലിച്ചാൽ പിഴയുണ്ട്

എപ്പോൾ വേണമെങ്കിലും പിൻവലിക്കാം (ചിലതിന് ലോക്ക്-ഇൻ പിരീഡ് ഉണ്ട്)

നികുതി (Tax)

പലിശ വരുമാനത്തിന് ടാക്സ് ഉണ്ട്

ദീർഘകാല നിക്ഷേപങ്ങൾക്ക് നികുതി ഇളവുകൾ ലഭ്യമാണ്

പണപ്പെരുപ്പം

വിലക്കയറ്റത്തെ തോൽപ്പിക്കാൻ ബുദ്ധിമുട്ടാണ്

വിലക്കയറ്റത്തെ തോൽപ്പിക്കാൻ മികച്ചത്

ഏതാണ് നിങ്ങൾ തിരഞ്ഞെടുക്കേണ്ടത്?

ഇതൊരു മില്യൺ ഡോളർ ചോദ്യമാണ്! ഇത് നിങ്ങളുടെ ആവശ്യങ്ങളെ ആശ്രയിച്ചിരിക്കും. നമുക്ക് ചില ഉദാഹരണങ്ങൾ നോക്കാം:

അടുത്ത വർഷത്തെ സ്കൂൾ ഫീസ്: നിങ്ങൾക്ക് അടുത്ത വർഷം തന്നെ പണം ആവശ്യമുണ്ടെങ്കിൽ റിസ്ക് എടുക്കാതെ എഫ്ഡി തിരഞ്ഞെടുക്കുന്നതാണ് നല്ലത്.

മകളുടെ വിവാഹം അല്ലെങ്കിൽ മകന്റെ ഉപരിപഠനം: പത്ത് പന്ത്രണ്ട് വർഷം കഴിഞ്ഞ് വലിയൊരു തുക ആവശ്യമുണ്ടെങ്കിൽ കണ്ണും പൂട്ടി മ്യൂച്വൽ ഫണ്ട് തിരഞ്ഞെടുക്കാം.

അത്യാവശ്യ ഫണ്ട് (Emergency Fund): വീട്ടിൽ ആർക്കെങ്കിലും പെട്ടെന്ന് അസുഖം വന്നാലോ മറ്റോ എടുക്കാൻ കുറച്ചു പണം എപ്പോഴും ബാങ്കിൽ (FD/Savings) വേണം.

നിങ്ങൾ ശ്രദ്ധിക്കേണ്ട 3 കാര്യങ്ങൾ:

ലക്ഷ്യം നിശ്ചയിക്കുക: എന്തിനു വേണ്ടിയാണ് നിങ്ങൾ പണം ലാഭിക്കുന്നത്? വീട് വെക്കാനാണോ അതോ ഒരു കാർ വാങ്ങാനാണോ?

സമയം: എത്ര കാലം പണം നിക്ഷേപിച്ചു വെക്കാൻ നിങ്ങൾക്ക് കഴിയും? സമയം കൂടുന്തോറും മ്യൂച്വൽ ഫണ്ടിലെ ലാഭവും കൂടും.

എല്ലാ മുട്ടയും ഒരു കുട്ടയിൽ ഇടരുത്: കുറച്ചു പണം എഫ്ഡിയിലും കുറച്ചു പണം മ്യൂച്വൽ ഫണ്ടിലും നിക്ഷേപിക്കുന്നതാണ് ഏറ്റവും ബുദ്ധിപരമായ നീക്കം.

സുഹൃത്തുക്കളെ, എഫ്ഡിയും മ്യൂച്വൽ ഫണ്ടും അവരവരുടെ രീതിയിൽ നല്ലതാണ്. സേഫ്റ്റി വേണമെന്നുണ്ടെങ്കിൽ എഫ്ഡി നോക്കാം, പണം വളരണമെന്നുണ്ടെങ്കിൽ മ്യൂച്വൽ ഫണ്ട് തിരഞ്ഞെടുക്കാം. നിങ്ങളുടെ പോക്കറ്റിനും സ്വഭാവത്തിനും ഇണങ്ങുന്നത് ഏതാണെന്ന് ചിന്തിച്ച് മാത്രം തീരുമാനമെടുക്കുക.

നിങ്ങൾ ഇപ്പോൾ എവിടെയാണ് പണം നിക്ഷേപിക്കുന്നത്? അതോ നിക്ഷേപം തുടങ്ങാൻ പ്ലാൻ ചെയ്യുന്നതേയുള്ളൂ? നിങ്ങളുടെ അഭിപ്രായങ്ങളും സംശയങ്ങളും താഴെ കമന്റായി അറിയിക്കുമല്ലോ. നമുക്ക് അവിടെ സംസാരിക്കാം!

പതിവ് സംശയങ്ങൾ (FAQs)

1. മ്യൂച്വൽ ഫണ്ടിൽ പണം നഷ്ടപ്പെടുമോ?

ഓഹരി വിപണിയുമായി ബന്ധപ്പെട്ടതായതുകൊണ്ട് ചെറിയ റിസ്ക് ഉണ്ട്. പക്ഷേ 5-10 വർഷത്തേക്ക് നിക്ഷേപിക്കുകയാണെങ്കിൽ നഷ്ടം വരാനുള്ള സാധ്യത വളരെ കുറവാണ്. നല്ലൊരു ഫണ്ട് തിരഞ്ഞെടുക്കുക എന്നതാണ് പ്രധാനം.

2. എത്ര രൂപ മുതൽ മ്യൂച്വൽ ഫണ്ടിൽ നിക്ഷേപിക്കാം?

പല ഫണ്ടുകളിലും മാസം 500 രൂപ മുതൽ നിക്ഷേപം തുടങ്ങാം. ഇതിനെ SIP (Systematic Investment Plan) എന്നാണ് പറയുന്നത്. നമ്മുടെ ചെറിയ സമ്പാദ്യങ്ങൾ വലിയൊരു തുകയായി മാറാൻ ഇത് സഹായിക്കും.

3. പ്രായമായവർക്ക് ഏതാണ് നല്ലത്?

പ്രായമായവർക്ക് സ്ഥിരമായ വരുമാനം ആവശ്യമായതുകൊണ്ട് എഫ്ഡി അല്ലെങ്കിൽ സീനിയർ സിറ്റിസൺ സേവിങ്സ് സ്കീമുകൾ കൂടുതൽ അനുയോജ്യമാണ്. എങ്കിലും പണത്തിന്റെ ഒരു ചെറിയ ഭാഗം മ്യൂച്വൽ ഫണ്ടിൽ ഇടുന്നത് വിലക്കയറ്റത്തെ നേരിടാൻ സഹായിക്കും.

4. എഫ്ഡിയിൽ നിന്ന് പണം എപ്പോൾ വേണമെങ്കിലും എടുക്കാമോ?

എടുക്കാം, പക്ഷേ ബാങ്ക് ചെറിയൊരു തുക പിഴയായി ഈടാക്കും. പലിശ നിരക്കിലും കുറവ് വരും. മ്യൂച്വൽ ഫണ്ടാണെങ്കിൽ (ലിക്വിഡ് ഫണ്ടുകൾ പോലുള്ളവ) പെട്ടെന്ന് പണം പിൻവലിക്കാൻ എളുപ്പമാണ്.

5. ഏതാണ് കൂടുതൽ ലാഭകരം?

ചരിത്രം പരിശോധിച്ചാൽ ദീർഘകാല നിക്ഷേപങ്ങൾക്ക് (5 വർഷത്തിന് മുകളിൽ) മ്യൂച്വൽ ഫണ്ടുകളാണ് എപ്പോഴും എഫ്ഡിയേക്കാൾ കൂടുതൽ ലാഭം നൽകിയിട്ടുള്ളത്.

ഇതുമായി ബന്ധപ്പെട്ട് കൂടുതൽ അറിയാൻ ഞങ്ങളുടെ മറ്റ് ലേഖനങ്ങളും വായിക്കാവുന്നതാണ്. കൃത്യമായ പ്ലാനിംഗിലൂടെ നമുക്കും സാമ്പത്തിക ഭദ്രത നേടാം!

Which Is Better for You? (Complete Guide for Indian Investors)

The Real-World Dilemma of Indian Investors

Meet Ramesh, a 32-year-old working in Kochi. Like many Indians today, he wants to grow his savings beyond a bank FD and has heard a lot about SIPs and mutual funds. He downloads a few “zero commission” investment apps, compares star ratings of funds, starts a SIP, and feels proud.

But soon… he is confused.

Should he invest more in equity?

Why did his fund fall last month?

Which ELSS fund should he use for tax saving?

Should he stop SIPs when markets dip?

How should he plan for his child’s education?

Meanwhile his colleague Amrita invests through a mutual fund distributor. She doesn’t worry about research, rebalancing, or risk. Her advisor reviews her portfolio quarterly, suggests SIP top-ups, evaluates goals, explains market dips, and helps with tax planning.

Both invest in the same mutual fund category. But while Ramesh keeps switching funds and stopping SIPs during volatile months, Amrita follows a disciplined strategy created for her goals — and ends up earning higher long-term returns with less stress.

So the big question arises for investors today:

“Is it worth paying for a distributor’s help, or should you go direct?”

This debate of direct vs distributor mutual funds has grown in the last few years due to fintech apps and DIY investing culture.

Reality check: While direct mutual funds may look cheaper due to slightly lower expense ratios, the real cost comes from wrong choices, poor asset allocation, and emotional mistakes — especially during crashes.

On the other hand, a skilled mutual fund distributor or mutual fund investment advisor brings structured financial planning, goal-based investing, risk management, and behavioral guidance — which most investors desperately need.

Throughout India — especially in small cities and towns — people rely on distributors because they want handholding, not just a transaction platform.

Based in Kerala, BVB Capital is a AMFI-registered, client-first, technology-enabled mutual fund distributor helping families build wealth without confusion, panic, or guesswork.

🟢 Thesis: For most investors (80–90% of Indians), the benefits of a good distributor easily outweigh the small cost difference of direct plans — and BVB Capital excels because of its experienced management team, advisory-led model, and long-term client focus.

Understanding Mutual Fund Investment Options

Before deciding which route to take, it’s important to understand how mutual funds can be purchased in India.

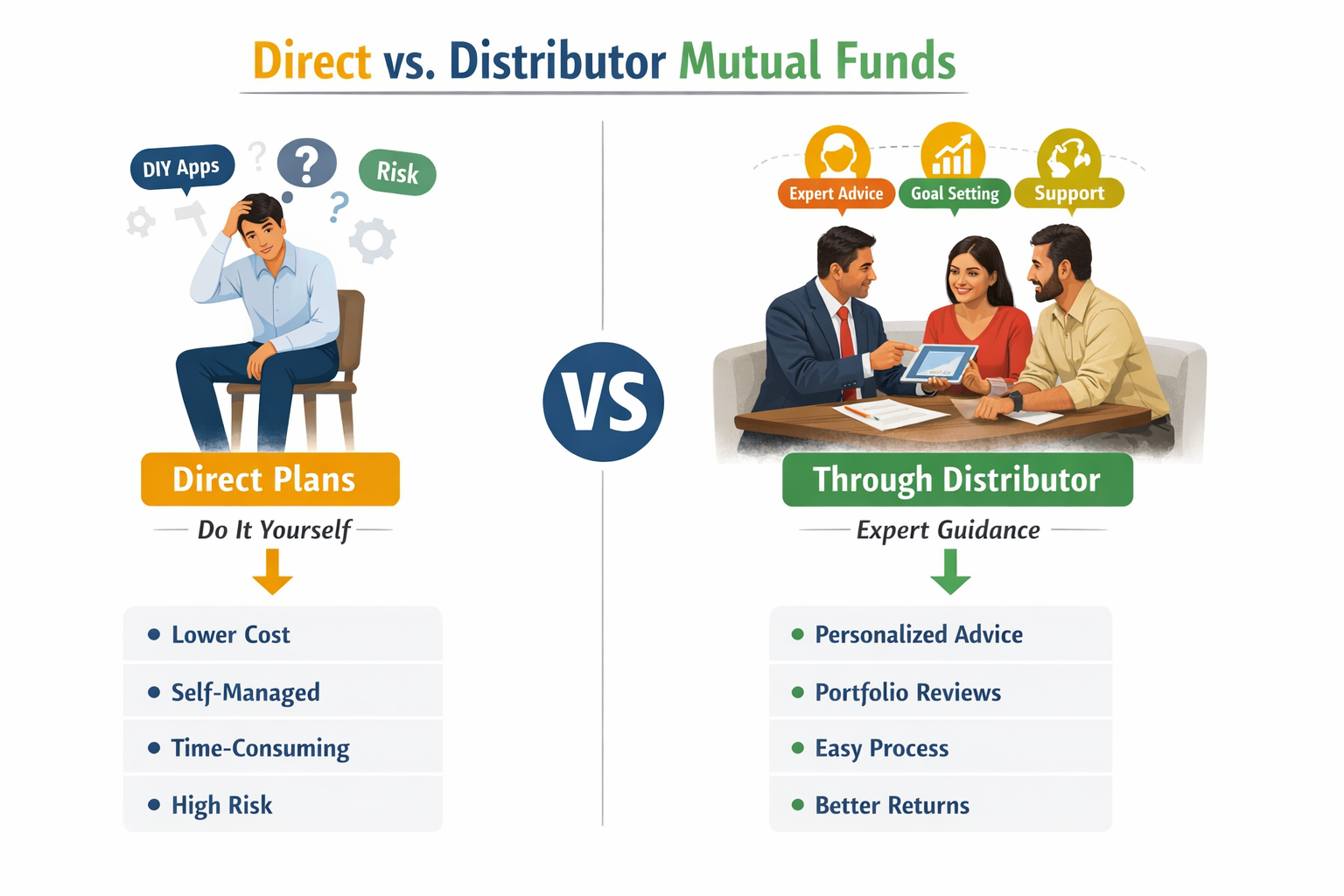

What are Direct Plans?

Direct plans allow you to invest directly with the AMC (fund house) through:

AMC websites

AMC apps

RTA portals (CAMS, Kfintech)

Some online DIY platforms

Key features of direct plans:

Lower expense ratio (no distributor commission)

Full control — investor chooses funds, tracks performance, manages risk

Suitable mainly for DIY financial experts

But there’s a catch: Investors must handle asset allocation, taxation, fund selection, rebalancing, market behavior, and documentation on their own.

What are Regular Plans via Distributors?

Regular plans are purchased through a mutual fund distributor or advisor who assists with:

Goal setting

Fund selection

Documentation & KYC

Ongoing review

Rebalancing

Market guidance

Regular plans have a slightly higher expense ratio because distributors are paid by AMCs for providing services.

For 90% of Indian investors, a trusted distributor is more beneficial because investing is not just selecting funds — it’s about managing entire financial life cycles.

Top Benefits of Using a Mutual Fund Distributor

Here are the major mutual fund distributor benefits that most investors underestimate:

1. Personalized Investment Advice

Distributors analyze:

Age

Income & cash flow

Risk profile

Time horizon

Life goals (retirement, education, home, tax)

They design goal-based portfolios tailored to investors.

Example:

25-year-old professional → equity-heavy SIPs for long-term growth

60-year-old retiree → debt & hybrid for stability & income

2. Access to 1000+ Funds Across AMCs

Instead of relying on popular brand names, distributors help you choose across:

Equity

Debt

Hybrid

Solution-oriented funds

Index funds

ELSS for tax planning

This ensures proper diversification, not random selection.

3. Ongoing Portfolio Review & Rebalancing

Markets change, life changes — portfolios must too.

Distributors provide:

Quarterly reviews

Asset rebalancing

SIP top-up recommendations

Category rotation (largecap ↔ midcap, etc.)

This helps maintain the right risk-return balance.

4. Time-Saving Transactions & Support

Investors don’t want paperwork headaches such as:

KYC registration

FATCA

Consolidated statements

SIPS/STPs/SWPs

Nomination updates

Distributors handle all of this smoothly.

5. Behavioral & Emotional Discipline

One of the most underrated advantages:

Investment success is more about behaviour than returns.

During market volatility, DIY investors panic.

Example: During the 2020 COVID crash, many DIY investors sold at bottoms, while distributors advised clients to continue SIPs, leading to significant wealth creation post recovery.

6. Risk Management

Distributors help avoid:

Over-concentration in a single stock/sector

Wrong timing decisions

Misalignment of asset allocation

They also guide on debt vs equity balance, crucial for retirees.

7. Tax Optimization

They assist with:

ELSS fund selection

Capital gains tax calculations

Dividend taxation

Setting SWP for tax efficiency

8. Cost-Effectiveness in Long Term

While direct plans save 0.5–1% TER, mistakes can cost 2–5% returns annually due to:

Wrong fund choices

Lack of rebalancing

Stopping SIPs

Timing markets

Over-diversification or under-diversification

Industry reports suggest that guided investors earn 1–2% higher net returns due to discipline and asset allocation.

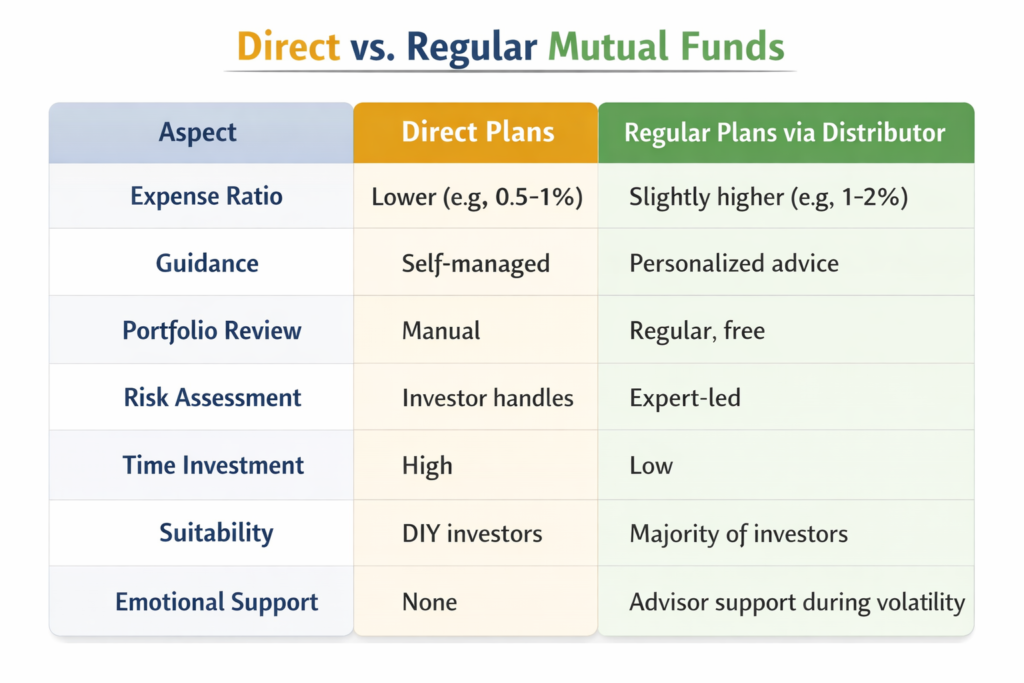

Direct vs Distributor: Head-to-Head Comparison

To make things crystal clear, here is a direct comparison:

Pros & Cons Table

Factor

Direct Plans Pros/Cons

Distributor Pros/Cons

Cost

✔ Lower TER ✖ Hidden errors cost more

✔ Saves via expertise ✖ Commission in expense ratio

Expertise

✖ Investor must self-educate

✔ Custom strategies & guidance

Convenience

✔ 24/7 apps ✖ Zero handholding

✔ Full service ✖ Appointment-based

Suitability

Experts only

Beginners, families, HNIs

Behavioral Control

✖ High panic risk

✔ Emotional discipline

Portfolio Returns

Variable due to errors

Optimized (1–3% possible edge)

Verdict

Data from multiple consumer surveys show that:

80%+ of Indian investors prefer distributors

Only 10–15% have the knowledge for direct investing

Errors hurt long-term compounding more than commissions

So, while direct plans look attractive on paper, distributors win in real life — especially for:

Beginners

Busy professionals

Retirees

Business owners

Families planning life goals

Why BVB Capital Private Limited Is the Best Choice for Investors

1. Who We Are

BVB Capital Private Limited is a Kerala-based, AMFI-registered mutual fund distributor dedicated to simplifying investments for Indians.

Our mission:

To make wealth-building simple, transparent, and stress-free for every investor.

We are built for people who want:

Guidance, not confusion

Discipline, not panic

Knowledge, not tips

Long-term wealth, not short-term gambling

2. What Makes Us Different

While many providers just offer “platforms,” BVB Capital offers a complete advisory ecosystem:

This team-based model ensures investors get research-backed advice, not generic recommendations.

5. Our Advisory Philosophy

At BVB Capital, we believe:

Investing is personal

Risk matters as much as return

Markets reward patience

SIPs are powerful wealth builders

Advice must be unbiased & transparent

We educate clients because informed investors stay disciplined.

6. Comparison With Others

Category

Generic Distributor

BVB Capital

Advisory Quality

Transaction-focused

Advisory-driven

Client Interaction

One-time

Continuous relationship

Goal Planning

Minimal

Structured & documented

Review Frequency

Annual/None

Quarterly reviews

Tools & Reporting

Basic

Digital dashboards

Conclusion

Direct mutual funds are good for trained, disciplined DIY investors.

But for most Indians, the value of a skilled mutual fund distributor or mutual fund investment advisor is far greater than the small cost difference.

From personalized planning to behavioral guidance and disciplined compounding — distributors make wealth building simpler, smarter, and stress-free.

And when it comes to choosing one, BVB Capital Private Limited stands out for its expert management team, advisory-first approach, and technology-driven client service, making it among the best mutual fund distributor India for families and professionals.

👉 Ready to invest smart and grow your wealth? Book a free consultation with us at: https://bvbcap.com/

Start your SIP today and build wealth the right way — with guidance, discipline, and confidence.

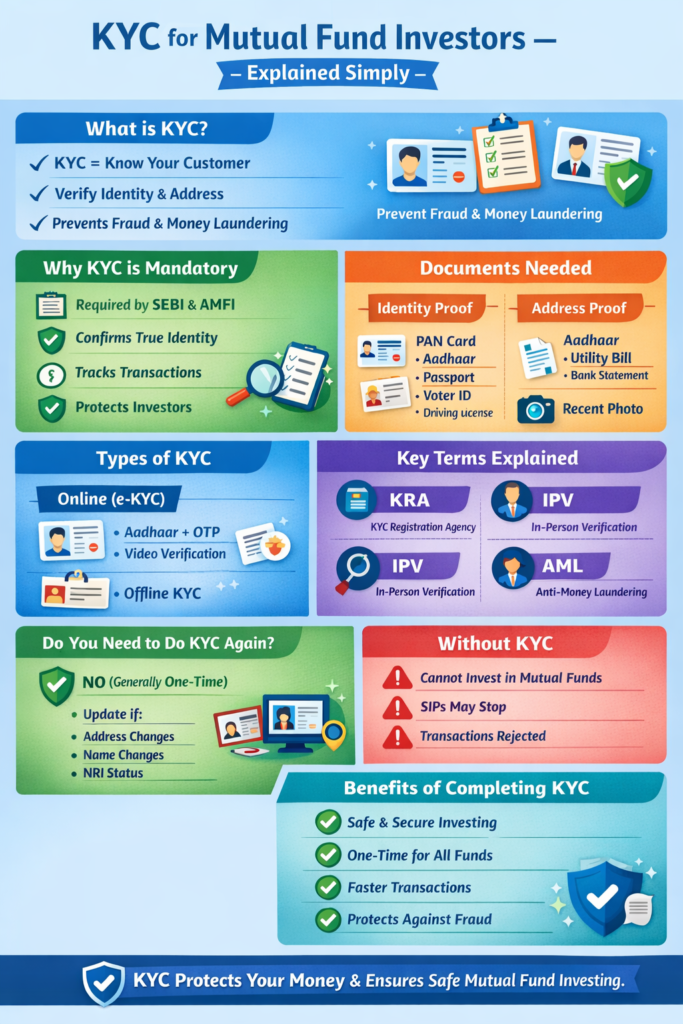

If you have ever tried to invest in a mutual fund, buy insurance, or open a bank account, you may have heard the term KYC. Many people find it confusing at first, so let’s break it down in simple English.

What is KYC?

KYC stands for Know Your Customer.

It is a process used by financial institutions (like banks, mutual fund companies, stockbrokers, etc.) to confirm the identity and address of a customer before allowing financial transactions.

In simple words:

KYC is like showing your ID card before entering a secured area. It proves that you are a real and genuine person.

Why Was KYC Created in the First Place?

Financial systems like banks and mutual funds deal with huge amounts of money. Without proper checks, criminals may misuse the system for illegal activities.

KYC helps to prevent:

✔ Money Laundering (hiding illegal money by making it look legal) ✔ Terrorist Financing (funding harmful activities) ✔ Identity Theft (someone pretending to be you) ✔ Fraud and Financial Scams

So, KYC protects both the financial institution and the investor.

Who Makes KYC Mandatory?

In India, KYC rules for mutual funds are governed by:

These authorities ensure that the Indian financial markets remain safe and transparent.

Why is KYC Mandatory for Mutual Fund Investors?

Mutual funds allow people to invest money and earn returns. Since money is involved, the system must be safe.

KYC is mandatory because it helps:

1. Verify Investor Identity

Mutual funds must know who is investing. This prevents fraud and protects honest investors.

2. Track Financial Activities

If a suspicious transaction happens, authorities can investigate easily.

3. Protect Investors’ Money

KYC creates a secure investment environment and reduces chances of misuse.

4. Follow Government Regulations

AMCs (Asset Management Companies) must obey SEBI rules. KYC ensures compliance.

What Documents Are Needed for KYC?

To complete KYC, you generally need:

Proof of Identity (POI) – example:

PAN Card

Aadhaar Card

Passport

Voter ID

Driving License

Proof of Address (POA) – example:

Aadhaar

Passport

Driving License

Electricity bill

Bank statement

Photograph

A recent passport-size photo (physical KYC)

Live photo (for online KYC)

PAN Card is Compulsory

Because PAN helps track financial transactions in India.

Types of KYC (Modes of Completion)

There are mainly two types:

1. Offline KYC

Submit physical documents

Sign forms

In-person verification may be done

2. Online KYC (e-KYC)

Aadhaar-based verification

Paperless and quick

Can submit through KRA (KYC Registration Agencies)

For mutual funds, popular KRAs include:

CVL KRA (CDSL Ventures)

NDML KRA

Karvy KRA

DOTEX KRA, etc.

Understanding Some Complicated Terms

Here are terms that often confuse investors — explained easily:

✔ KRA (KYC Registration Agency)

A KRA stores and verifies KYC records. Once you register KYC with one KRA, it works for all mutual fund companies.

✔ IPV (In-Person Verification)

A simple face-to-face verification process to confirm that the person exists in real life. In online KYC, this may happen through a video call.

✔ e-KYC

Electronic KYC using Aadhaar number and OTP. It is fast, digital, and paperless.

✔ AML (Anti-Money Laundering)

Rules made to stop criminals from using financial systems to hide illegal money.

✔ FATCA

A US law that requires financial institutions to report details of investors who are US taxpayers. (Needed only if applicable to you)

Is KYC a One-Time Process?

Yes, mostly you do KYC only once.

After successful registration:

You can invest in any mutual fund

You don’t need to repeat KYC for every AMC

Sometimes details may need updating if:

You change address

Your name changes (marriage, legal reasons)

You become a Non-Resident Indian (NRI)

What Happens If You Don’t Do KYC?

Without KYC, you cannot invest in mutual funds.

Even if you have existing SIPs, they may be stopped if your KYC becomes invalid due to mismatches or missing details.

Benefits of Completing KYC

✔ Safer and transparent investment ✔ One-time setup for all mutual funds ✔ Faster transactions and redemptions ✔ Protection from fraud and misuse ✔ Mandatory legal compliance

So doing KYC is not just a rule — it’s for your own financial safety.

Common Myths About KYC

Myth

Reality

KYC is risky

No, it protects your money

KYC shares my data publicly

No, data is protected by law

KYC takes a long time

Online KYC is quick & simple

Only big investors need KYC

Every investor needs KYC

Conclusion

KYC may feel like paperwork, but it plays a very important role in keeping mutual fund investments safe, legal, and transparent. It protects both the investor and the financial system from fraud and misuse.

Whether you are a new investor or experienced, understanding KYC helps you invest with confidence.

Final Takeaway in One Line:

KYC exists to protect your money and ensure safe investing — that’s why it is mandatory.

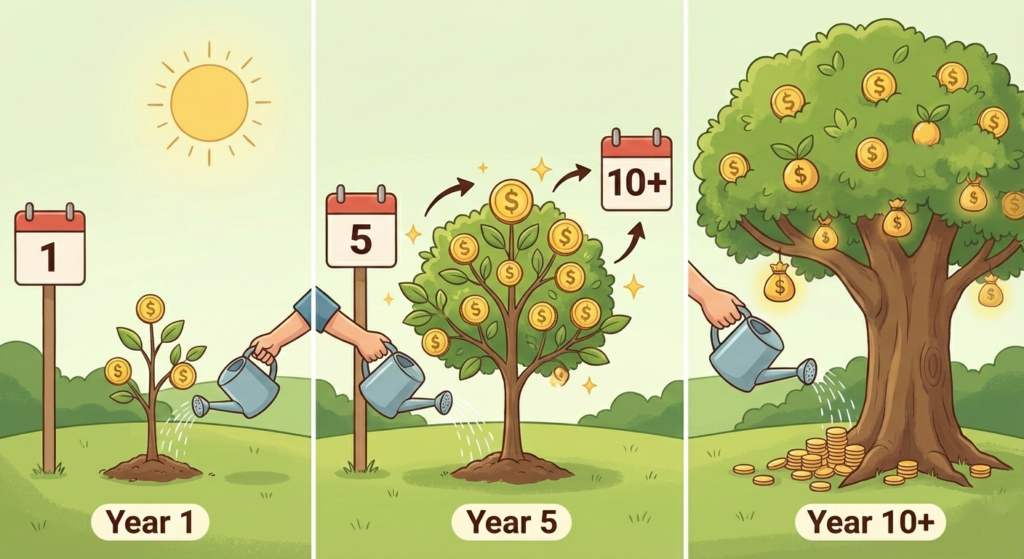

കൂട്ടുകാരെ, നമുക്കെല്ലാവർക്കും മിഠായി വാങ്ങാനും കളിപ്പാട്ടങ്ങൾ വാങ്ങാനും ഒക്കെ പൈസ വേണം, അല്ലേ? സാധാരണ നമ്മൾ എന്ത് ചെയ്യും? അച്ഛനോ അമ്മയോ തരുന്ന പൈസ ഒരു കുടുക്കയിൽ (Piggy bank) ഇട്ടു വെക്കും. കുറെ നാൾ കഴിയുമ്പോൾ ആ കുടുക്ക നിറയും.

ഇതുപോലെ വലിയവർ പണം സമ്പാദിക്കുന്ന ഒരു സൂപ്പർ വഴിയെക്കുറിച്ചാണ് ഇന്ന് നമ്മൾ പറയാൻ പോകുന്നത്. അതിന്റെ പേരാണ് SIP-യും SWP-യും. കേട്ടിട്ട് പേടി തോന്നുന്നുണ്ടോ? പേടിക്കണ്ട, സംഗതി വളരെ സിമ്പിളാണ്!

1. എന്താണ് ഈ SIP? (മരം നടുന്ന കാലം)

നമ്മൾ ഒരു മാവിൻ തൈ നടുന്നു എന്ന് വിചാരിക്കുക. നമ്മൾ ദിവസവും അതിന് വെള്ളമൊഴിക്കും, ശ്രദ്ധിക്കും. പെട്ടെന്ന് ഒരു ദിവസം കൊണ്ട് അത് വലിയ മരമാകില്ല. വർഷങ്ങൾ എടുക്കും. പക്ഷേ, നമ്മൾ മടുക്കാതെ എന്നും വെള്ളമൊഴിച്ചാൽ അത് പതുക്കെ പതുക്കെ വളർന്ന് വലിയൊരു മരമാകും.

ഇതുപോലെ, എല്ലാ മാസവും നമ്മുടെ കയ്യിലുള്ള ചെറിയൊരു തുക (അത് 500 രൂപയോ 1000 രൂപയോ എത്രയുമാകാം) സമ്പാദിക്കുന്ന രീതിയാണ് SIP (Systematic Investment Plan).

ഗുണം: ചെറിയ തുകയായതുകൊണ്ട് നമുക്ക് ബുദ്ധിമുട്ടുണ്ടാകില്ല.

മാജിക്: വർഷങ്ങൾ കഴിയുമ്പോൾ ഈ ചെറിയ തുക ഒരു വലിയ ‘പണത്തിന്റെ മരമായി’ മാറും. ഇതിനെയാണ് ‘കോമ്പൗണ്ടിംഗ്’ (Compounding) എന്ന് വിളിക്കുന്നത്. അതായത്, പണം വളർന്ന് വളർന്ന് വലുതാകുന്ന മാജിക്!

2. എന്താണ് ഈ SWP? (പഴം പറിക്കുന്ന കാലം)

നമ്മൾ നട്ട മാവ് വലുതായി എന്ന് വിചാരിക്കുക. ഇനി നമുക്ക് എന്ത് ചെയ്യാം? ആ മരം മുറിച്ചു വിൽക്കാം. പക്ഷേ, അങ്ങനെ ചെയ്താൽ പിന്നെ നമുക്ക് മാമ്പഴം കിട്ടില്ലല്ലോ?

അതിന് പകരം, മരത്തിലെ മാമ്പഴം മാത്രം ഓരോന്നായി പറിച്ചെടുത്താലോ? മരം അവിടെത്തന്നെ ഉണ്ടാകും, നമുക്ക് എല്ലാ കാലത്തും മാമ്പഴം കഴിക്കുകയും ചെയ്യാം.

ഇതാണ് SWP (Systematic Withdrawal Plan). നമ്മൾ SIP വഴി ഉണ്ടാക്കിയ വലിയൊരു തുകയിൽ നിന്ന്, എല്ലാ മാസവും കൃത്യമായ ഒരു തുക ശമ്പളം പോലെ തിരിച്ചെടുക്കുന്ന രീതിയാണിത്.

ഗുണം: ജോലിയിൽ നിന്നൊക്കെ വിരമിച്ചു കഴിയുമ്പോൾ (Retirement), കയ്യിൽ പണമില്ലാതെ വിഷമിക്കണ്ട. ഈ മരത്തിൽ നിന്ന് മാമ്പഴം പറിക്കുന്നത് പോലെ എല്ലാ മാസവും പണം കിട്ടിക്കൊണ്ടിരിക്കും. ബാക്കി പണം അവിടെയിരുന്ന് വീണ്ടും വളരുകയും ചെയ്യും!

ചുരുക്കത്തിൽ പറഞ്ഞാൽ:

SIP: ഇത് പണം നിക്ഷേപിക്കുന്ന ഘട്ടമാണ്. ഒരു വലിയ സമ്പാദ്യം ഉണ്ടാക്കിയെടുക്കാൻ ഇത് സഹായിക്കുന്നു.

SWP: ഇത് നിക്ഷേപിച്ച പണം ഉപയോഗിക്കുന്ന ഘട്ടമാണ്. എല്ലാ മാസവും ഒരു വരുമാനം ഉറപ്പാക്കാൻ ഇത് സഹായിക്കുന്നു.

നമ്മൾ എന്ത് ചെയ്യണം?

ഇപ്പോൾ നിങ്ങൾ കുട്ടികളാണെങ്കിലും, ഈ കാര്യം മനസ്സിലാക്കി വെക്കുന്നത് നല്ലതാണ്. വലുതാകുമ്പോൾ ആദ്യത്തെ ശമ്പളം കിട്ടിത്തുടങ്ങുമ്പോൾ തന്നെ ഒരു ചെറിയ SIP തുടങ്ങിയാൽ, ഭാവിയിൽ നിങ്ങൾക്ക് സാമ്പത്തികമായി ഒരു ബുദ്ധിമുട്ടും ഉണ്ടാവില്ല.

ഓർക്കുക: ഇന്ന് നാം നടുന്ന ചെറിയ തൈയാണ് നാളെ നമുക്ക് തണലും പഴങ്ങളും തരുന്നത്!

നിങ്ങളുടെ അച്ഛനോടും അമ്മയോടും ഈ കാര്യത്തെക്കുറിച്ച് ചോദിച്ചു നോക്കൂ. അവർക്കും ഇതൊരു പുതിയ അറിവായേക്കാം!