Over the last few years, investing has become easier than ever. With just a smartphone, anyone can start investing in mutual funds within minutes. This is a positive development. Technology has democratized investing and allowed more people to participate in wealth creation.

However, at BVB Capital Private Limited, we are observing a concerning trend.

Many people who intend to be investors are unknowingly behaving like traders.

This shift is happening silently, and modern investment apps are playing a major role in encouraging this behavior.

This article is written to create awareness so that investors can protect their financial future.

The Rise of Convenience — and the Rise of Confusion

Earlier, investing involved discussions with advisors, understanding goals, and selecting suitable investments. Today, apps provide thousands of schemes, performance rankings, star ratings, and instant transaction options.

While this convenience is powerful, it also creates a false sense of expertise.

At BVB Capital, we regularly receive calls from individuals who want to:

- Invest in the same mutual fund scheme through multiple AMCs or folios

- Enter with the intention of holding for less than 6 months

- Exit immediately if they don’t see profits

- Select schemes purely based on recent returns or ratings

- Invest without defining any financial goal

This approach is not investing.

This is trading behavior.

And mutual funds are not designed for trading.

Investing vs Trading — Understanding the Fundamental Difference

Investing is goal-based and long-term.

Trading is profit-based and short-term.

| Investing | Trading |

|---|---|

| Focus on long-term wealth creation | Focus on short-term price movements |

| Based on financial goals | Based on recent performance |

| Requires patience | Requires constant monitoring |

| Benefits from compounding | Often loses compounding advantage |

Mutual funds generate real wealth through time, discipline, and compounding—not through frequent entry and exit.

The Dangerous Illusion Created by Technology

Modern apps show:

- Top performing funds of last 1 year

- Star ratings

- Past returns

- Easy buy and sell options

But they do not show:

- Your personal financial goals

- Your risk capacity

- Your investment horizon

- Your emotional reaction during market corrections

Technology provides tools. But it does not provide wisdom.

This is where many investors make mistakes.

A Simple Analogy: Self-Medication vs Doctor’s Prescription

Imagine a patient searching Google and buying medicines without consulting a doctor.

They select medicines based on popularity, reviews, or advertisements.

They take the medicine for a few days.

If they don’t see improvement, they stop and switch to another medicine.

This behavior can worsen the health condition.

Investing without professional guidance is similar.

Mutual funds are financial instruments designed to serve specific purposes—retirement, education, wealth creation, or income.

Selecting schemes without understanding their purpose can harm financial health.

The Biggest Loss: Compounding Gets Destroyed

The real power of mutual funds is compounding.

Compounding works only with:

- Time

- Consistency

- Patience

Frequent switching interrupts compounding.

For example:

An investor who stays invested for 10 years may see significant wealth growth.

But an investor who enters and exits every 6 months may never experience the real benefits.

Short-term thinking destroys long-term wealth.

Why This Trend Is Increasing

There are three main reasons:

1. Instant Gratification Mindset

People expect quick results in everything, including investing.

2. Overconfidence Due to Easy Access

Apps create the illusion that investing is easy and requires no expertise.

3. Misunderstanding Mutual Funds

Many people think mutual funds are short-term profit tools, instead of long-term wealth creation tools.

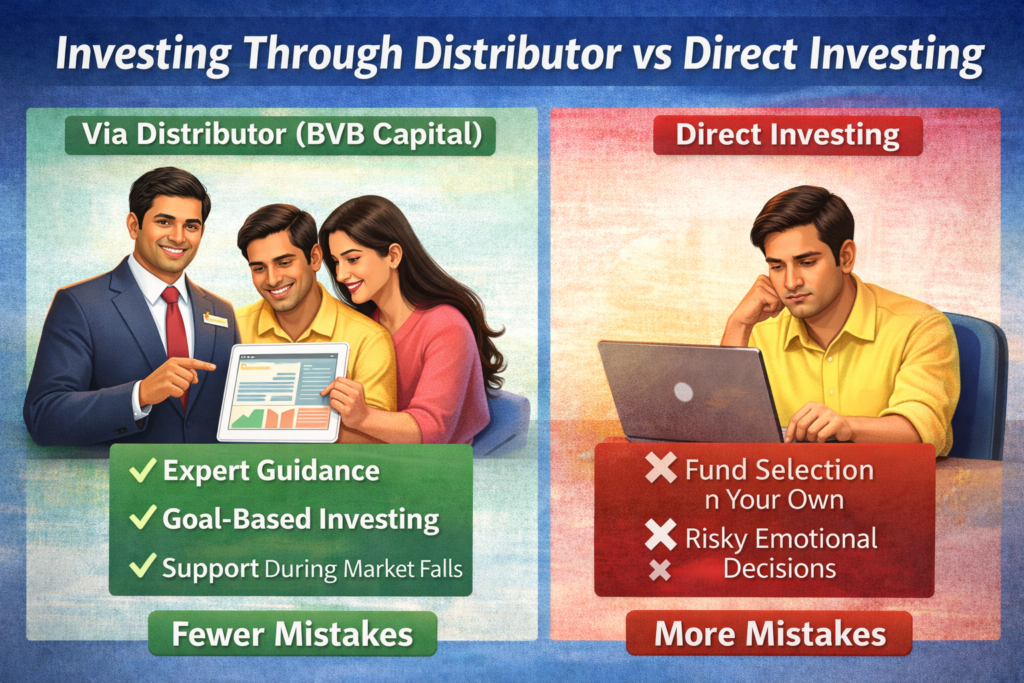

The Role of Proper Investment Planning

At BVB Capital Private Limited, our approach is different.

We believe every investment must have a purpose.

Before selecting any mutual fund, investors should clearly define:

- Why they are investing

- How long they can stay invested

- Their risk tolerance

- Their financial goals

Only then should suitable schemes be selected.

Not the other way around.

Mutual Funds Reward Discipline, Not Frequent Action

The most successful investors are not those who act frequently.

They are those who act wisely and remain disciplined.

Mutual funds are designed for:

- Long-term wealth creation

- Financial security

- Goal fulfillment

Not short-term speculation.

Technology Should Assist Investors — Not Replace Wisdom

Technology is a powerful tool.

But it should assist disciplined investing, not encourage impulsive decisions.

Apps cannot understand your life goals.

Apps cannot understand your responsibilities.

Apps cannot understand your financial future.

Only proper planning and professional guidance can do that.

The Responsible Approach to Investing

Before investing in any mutual fund, ask yourself:

- What is the purpose of this investment?

- How long can I stay invested?

- Am I investing or trading?

- Am I making decisions based on goals or emotions?

If these questions are unclear, it is better to seek guidance.

Our Message to Investors

At BVB Capital Private Limited, our mission is not just to facilitate investments.

Our mission is to help investors build sustainable, long-term wealth through disciplined and purpose-driven investing.

Mutual funds are powerful wealth creation tools—but only when used correctly.

Avoid turning investing into trading.

Avoid making decisions based on short-term results.

Avoid self-medication in investing.

Instead, follow a structured, goal-based approach.

Your financial future deserves patience, discipline, and clarity.

About BVB Capital Private Limited

BVB Capital Private Limited is committed to helping investors make informed and disciplined financial decisions. We focus on investor education, goal-based investing, and long-term wealth creation through proper planning and guidance.

Learn more at:

https://bvbcap.com